|

Getting your Trinity Audio player ready...

|

– Andrew Macken

To read the PDF version of our Q1 2026 update, please click here.

The significant geopolitical conflict in Iran dominated the March quarter. At the same time, many stocks had their valuation multiples rapidly revised down.

Investors now face two important questions: Which businesses deservedly declined because they were overvalued? And which businesses were sold off too harshly and are on sale?

The good news is that based on our analysis, there are several competitively advantaged businesses on sale today.

While the March quarter was a tough one, Montaka’s investment philosophy has not changed. We seek to exploit long-duration market inefficiencies and deliver our investors sustainable long-term excess returns.

The market routinely undervalues businesses that can grow earnings power reliably over extended time horizons. This is because many market participants simply focus on the short term, and they lack the patience – and investment structures – necessary to exploit market inefficiencies that may take many years to be realized.

We have the patience and the structures, and this is a clear point of differentiation for Montaka.

Even when others have lost faith, we can maintain our holdings in competitively advantaged companies benefiting from long-term transformations.

As we share below, during the March quarter many investors lost faith in software companies. Ignoring many exculpatory facts, they decided that substantially all software companies would be economically impaired by AI. While this may be true for some, we believe it won’t be for all.

This swift loss of faith, and the sharp stock price declines that followed, forced many investors to sell. But we maintained Montaka’s long-term perspective, and didn’t allow ourselves to be derailed by increasingly viral market narratives.

In the letter that follows, we cover the following:

- We deconstruct Montaka’s investment performance in the March quarter – both absolute and relative to the broader market.

- We outline our views on the economic and market outlook, including recent geopolitical conflict, the AI transformation, and the market’s current valuation levels.

- We take a look at Montaka’s portfolio augmentations and positioning – including the addition of four new investments during the quarter.

- And we share a case-study on one of Montaka’s newer investments, leading UK defence contractor: BAE Systems.

For newer readers, we invite you to explore our latest insights and thematic analysis at montaka.com/blogs, where you’ll also find clear information on how to invest with us. Our most popular investment vehicle is quoted on the ASX under ‘MOGL’ – which can be purchased simply through your standard brokerage account, just as you would any other ASX listing.

Deconstructing Montaka’s Recent Investment Performance

Montaka’s strategy is built around a high-conviction, long-duration portfolio. This will inevitably feature lumpy returns over time.

In the March quarter, with the exception of Albemarle, BAE Systems, and Moderna, all of Montaka’s portfolio investments experienced a decline. When weighted by their portfolio size, the biggest detractors included Microsoft, KKR, ServiceNow, MongoDB, Meta Platforms, and Salesforce.

When stock prices decline, there are two causes: (i) changes in earnings power, and (ii) changes in the valuation multiple of said earnings power. Overwhelmingly, the stock declines in Montaka’s portfolio during the March quarter were driven by the latter (valuation multiples), not the former (earnings power).

In the analysis shared here, we show that the businesses owned by Montaka continue to perform very well fundamentally. It’s just that in recent months their valuation multiples have significantly derated.

When we calculate an indicative measure of Montaka’s portfolio-weighted look-through revenues (aggregate revenue adjusted for the size of each investment) over time, we see consistent double-digit annual growth, up to and including the most recent quarter of reported results. For the portfolio’s weighted look-through earnings, the rate of growth was even higher.

Yet, of late, the valuation multiple of Montaka’s portfolio-weighted look-through earnings fell by approximately 17%.

So earnings power remains strong, but the price at which the market is valuing these earnings has declined. We view this as an opportunity.

The broader market: Software and the US underperform

It is also constructive to consider the drivers of change in broader market indices.

The software sub-sector, in general, was by far the largest negative contributor to the S&P 500 Index during the quarter (with energy the strongest sector). The substantial selloff in software stocks over the period reflects a new viral narrative that AI agents will impair the value of existing software platforms.

We elaborate on this here and conclude that, while AI agents may well hurt many existing software businesses, for a few advantaged platforms with large incumbent customer bases, their trusted distribution will likely see their value strengthened.

High exposure to the US creates short-term pain, but long-term gain

Montaka’s portfolio also suffered during the quarter from its relatively high exposure to the US.

Compared to the likes of Europe and Hong Kong, US equity markets were more negative.

This hurt Montaka’s relative returns when measured against the MSCI World Total Return Index – an index that includes significant non-US exposure.

That said, we have clear and deliberate reasons for biasing Montaka’s portfolio to US exposures relating to geopolitical, technological, and macroeconomic advantages. And we believe that, over the longer term, this positioning will prove superior.

Despite short-term returns being negative from time to time, as in the March quarter, we believe Montaka’s philosophy of owning advantaged businesses positioned well in structural transformations will ultimately deliver attractive long-term returns for investors.

Economic and Market Outlook: Examining the 3 vital themes

In today’s complex world, we see three issues as most pertinent for investors positioning for the future:

- Geopolitics

- AI

- Market valuations

We briefly share Montaka’s current thinking on each.

Geopolitics: Iran highlights the potential of chokepoints to limit aggression

The war in Iran has spotlighted that the Strait of Hormuz is a geopolitical chokepoint. Iran has demonstrated to the world how it can close this strait with relative ease, send oil prices sharply higher and limit supplies for many countries.

Interestingly, strategists suggest this approach is a template for a possible Chinese intervention in Taiwan.[1] If the economic disruption from Iran has been significant, the disruption from a major conflict in Taiwan would likely be catastrophic. Taiwan produces approximately 80% of the world’s semiconductors, and any conflict in Taiwan would likely draw a response from numerous nations such as the US, UK, Japan and Australia.[2]

Yet recent observations suggest the probability of a potential China/Taiwan conflict has arguably reduced:

- China relies on imports for approximately 60-70% of its domestic oil consumption. And 45-50% of these imports transit the Strait of Hormuz. [3] This represents a major chokepoint for much-needed Chinese supplies, particularly oil.

- The Malacca Strait (located between Indonesia and Malaysia), through which approximately 80% of China’s oil imports pass,[4] too, represents a major chokepoint for China.

- Recent detailed simulations of a potential China/Taiwan conflict by US military strategists have identified that the sustainable supply of fuel (and most importantly, oil) is what ultimately determines how long either side can sustain combat operations.[5]

Iran has shone a light on how easily it has been to close the Strait of Hormuz. There is little doubt that China too has the power to disrupt global supplies by creating chokepoints, should it so choose. But the reverse must also be true: by closing the straits of either Hormuz or Malacca, others could disrupt sustainable fuel supply to China and thwart any potential intervention against Taiwan.

We believe recent events have strengthened deterrence and, with it, reduced the probability of conflict in Taiwan.

AI: Great investment potential in the hyperscalers

Here’s how we see the contours of the AI revolution today:

- Adoption is growing rapidly and demand for compute (hardware and computational power) is growing exponentially – particularly driven by compute-intensity of new agentic use cases.

- Interestingly, growing adoption of AI is accelerating enterprises and governments’ transition of non-AI workloads, such as databases, to public clouds. This is because AI relies on the cloud for its resource-intensive workloads, and in turn, drives organisations to more rapidly migrate their existing non-AI workloads to the cloud to leverage AI’s capabilities.

- The ability to expand electric power generation in the US – needed for more data center capacity – will likely remain relatively limited for years to come.

- China, by contrast, has significant excess electric power capacity, but has limited access to the latest AI chips – though progress is being made on domestically designed and fabricated chips.

- AI safety and security remain an underappreciated issue for enterprise and government deployments of AI agents, as we explore here, and will likely increase the need for more careful deliberations on agentic rollouts.

Against this backdrop, Montaka sees great investment opportunity in the three Western cloud-computing hyperscalers: Amazon, Microsoft, and Alphabet, for several reasons:

- Growth in demand for compute, a primary service of the hyperscalers, is far outstripping growth in capacity (which is significantly hindered by physical and political bottlenecks today) – and this is handing pricing power to the hyperscalers.

- Barriers to entry in cloud computing were already high and are going higher – driven by a powerful, self-reinforcing cycle of scale and investment that is almost impossible for new players to replicate. The capital required to build and maintain competing infrastructure runs into the many tens of billions each quarter, a price that few can afford.

- Said another way, competitive advantages are strong and strengthening. And yet, all three hyperscalers became cheaper during the March quarter.

Some believe that today’s hyperscalers are on a path to being disrupted by the AI foundation model companies, including OpenAI and Anthropic. Yet this appears to us to be a misdiagnosis of where the true competitive advantages lie today. And at least one foundation model company agrees with us:

“We see compute as a competitive advantage. If you do not have it, you do not have revenue. That is one thing I know for sure.”

– Sarah Friar, OpenAI CFO.[6]

Market valuations

The strength of an investment opportunity depends on the price at which you can acquire current and future earnings power. We see many instances today of strong competitive advantages being offered by the market at highly-attractive prices.

Based on Montaka’s internal assessments, here are several:

- Meta Platforms — Towards the end of March, Meta’s stock price hit US$526 per share, a level that implies an enterprise value (EV) multiple of less than 13x 2026 earnings before interest and tax (EBIT).[7] We assess this valuation multiple is far too low for a business growing revenues faster than 20% per annum and with competitive advantages as strong as Meta’s.

- KKR — KKR closed the quarter at US$92.50 per share, a level that implies an EV multiple of 17x 2026 fee-related earnings (FRE) – which itself is expected to grow by more than 20% p.a. this year.

- Salesforce — By quarter-end, Salesforce’s EV multiple was down to 4.8x 2026 gross profits (GP). To put this ratio in perspective, at the height of the 2000 ‘dot com’ bubble, Cisco’s EV was 70x GP. It was only following the stock’s 89% decline that Cisco bottomed at 5x EV/GP in October 2002.

- S&P Global — Another way Montaka routinely evaluates valuation levels is to consider what the stock is pricing in about the future. By quarter-end, we found S&P Global was pricing sustained revenue growth of (only) 3% per annum. This is for a business that has grown at more than double that rate in 13 out of the last 15 years. And S&P Global’s guided revenue growth for this year is also 6-8% per annum (excluding the effect of exchange rate changes).[8]

Overall, while the broader market is focused on war, oil prices, inflation and interest rates, we see opportunity today in select businesses with strong competitive advantages and large and growing addressable markets.

And many of these opportunities reside in Montaka’s portfolio today.

Portfolio Augmentations & Positioning: BAE, TSMC, Uber, Intercontinental Exchange

With the market throwing up opportunities in both new businesses and businesses Montaka already owns, during the March quarter we were more active in making portfolio augmentations.

-

BAE Systems – Defence exposure and countercyclical value

As mentioned above, we acquired BAE Systems. This is a large-scale, best-in-class defence contractor with significant diversification across technologies and customers globally.

BAE Systems is not only well positioned to benefit from the structural acceleration in global defence spending, but it also provides Montaka’s portfolio with some countercyclical value drivers during times of war, as we’ve experienced in recent weeks.

-

TSMC – Underappreciated pricing power

We also acquired Taiwan Semiconductor Manufacturing Co – more commonly known as TSMC – the world’s effective monopolist in AI semiconductor fabrication.

Given Montaka’s deep work in AI over many years, we’ve been following this company for some time. We had previously opted against investing in TSMC because of over geopolitical tail risk concerns, and we continue to handicap this investment for its concentrated exposure to Taiwan.

That said, the combination of accelerating demand for AI compute, combined with limited opportunities to expand US electric power generation capacity, means enhanced power efficiency will likely be a primary source of compute capacity expansion for the world’s cloud computing hyperscalers. And this gives TSMC extreme pricing power that we believe continues to be underestimated.

-

Uber – Competitive advantages and expansion potential

We acquired Uber on its recent stock price pull-back. Uber’s competitive advantages stem from its large-scale networks and flywheels – between users, drivers, merchants, and advertisers – particularly as they interface with the complex and messy real world. (Similar to the advantages of DoorDash, which we already own.)

And our analysis suggests these advantages will likely thrive in an agentic AI world. Furthermore, recent datapoints suggest the probability of potential disruption from autonomous vehicles is declining, while the probability of the mobility market expanding is increasing.

-

Intercontinental Exchange – Global market strengths

Finally, we also acquired Intercontinental Exchange, owner of the New York Stock Exchange, along with several other exchanges, clearing houses, and technology services. The company has particular strengths in global energy futures and options markets – with demand for risk management services in these markets only strengthening, in our view. And similar to BAE Systems, Intercontinental Exchange benefits from market volatility – which, of course, there is plenty of today.

To help fund these new acquisitions, Montaka exited lithium producer, Albemarle, after making a significant short-term gain, and a small position in Reliance Industries.

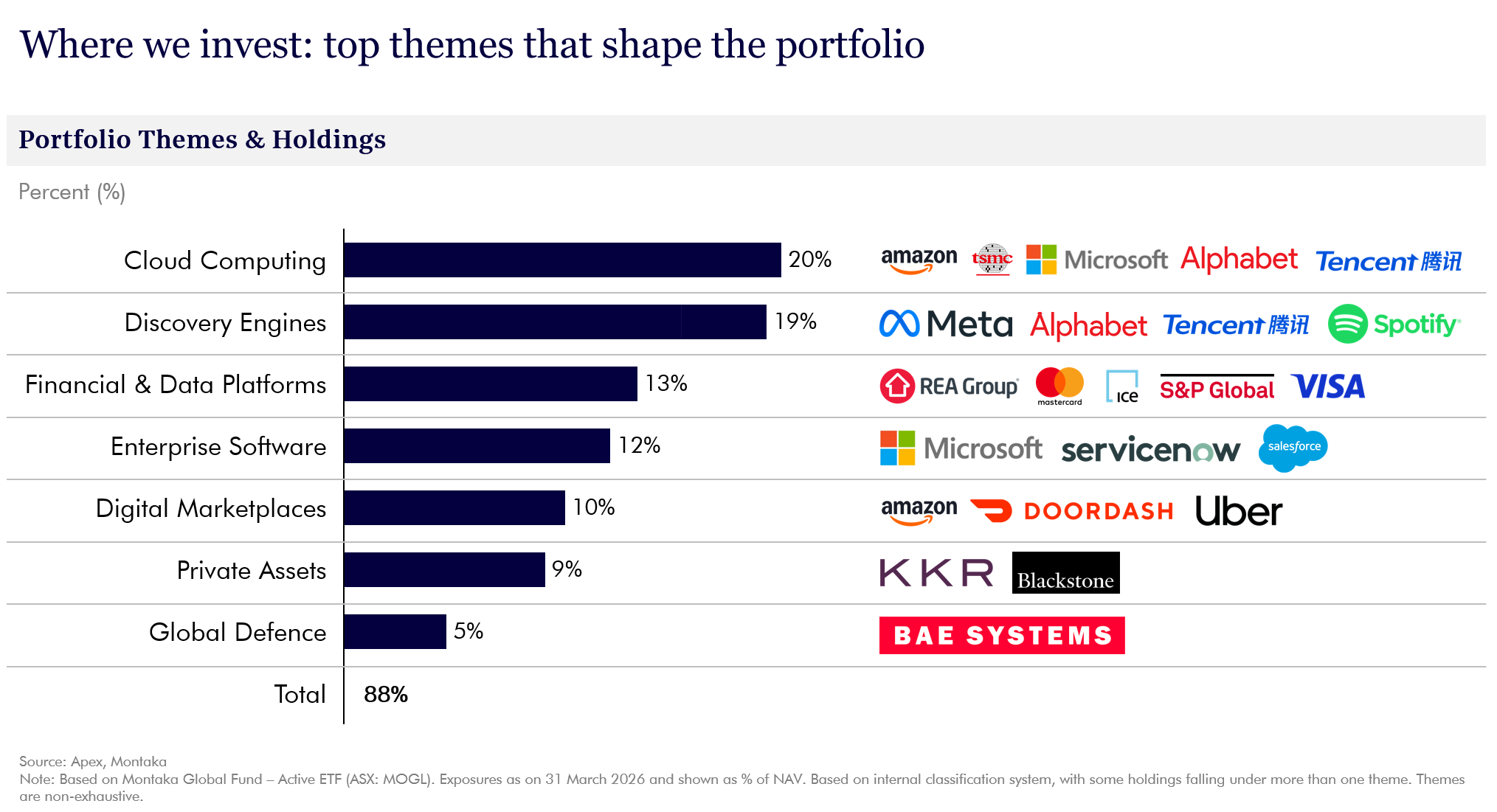

We enter April with the following key portfolio exposures. Shown on the left-hand side are the long-term themes we have invested behind, while on the right are those businesses we assess are strongly advantaged and likely to compound their earnings power over longer time horizons than the market expects.

* * *

In closing, we thank you again for your ongoing trust, partnership and patience – especially against the very testing backdrop of volatile global equity markets and Montaka’s recent short-term performance.

We reiterate our philosophy of patiently investing in advantaged businesses positioned within large structural transformations and trading at acceptable (or better, as is the case in many instances today) prices.

Rest assured, the entire team continues to work diligently every day to follow our processes – and improve them whenever possible. We have, for example, recently started to deploy agentic AI tools to significantly expand Montaka’s research team coverage, without diluting focus. We will expand on these evolutions more over the coming months.

As always, we welcome any thoughts, ideas or feedback you might have.

Sincerely,

Andrew Macken

Note:

[1] FT: Shutting Hormuz is a template for China in Taiwan, April 2026

[2] TSIA: Overview on Taiwan Semiconductor Industry, 2025 Edition

[3] Columbia SIPA: Implications of the Conflict in the Middle East for China’s Energy Security, March 2026

[4] Atlas Institute for International Affairs: Navigating the ‘Malacca Dilemma’ in 2025, March 2025

[5] The Heritage Foundation: Tidalwave – Strategic Exploitation & Sustainment in a US-China Conflict, January 2026

[6] Interview: Cathie Wood (ARK CEO/CIO) and Sarah Friar (OpenAI CFO), March 31, 2026

[7] Note: This earnings level deliberately excludes the costs associated with Reality Labs (RL), we make this adjustment on the basis that, over time, RL will either break-even or its losses will be discontinued.

[8] S&P Global: 4Q25 Earnings Filing

* * *

DISCLAIMER:

This update was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

‘Montaka Global Fund – Active ETF’ investors: This document was prepared by Montaka Global Pty Ltd, (ACN 604 878 533, AFSL 516 942) (a subsidiary of MFF Capital Investments Limited (“MFF”) (A.B.N 32 121 977 884)), the investment manager of the Montaka Global Fund – Active ETF (previously known as Montaka Global Long Only Equities Fund (Managed Fund)) (ARSN: 621 941 508). Perpetual Trust Services Limited (ACN 000 142 049, AFSL 236648) is the Responsible Entity and the issuer of units of the Montaka Global Fund – Active ETF. Copies of the Product Disclosure Statement (PDS) and Target Market Determination are available on this webpage: https://montaka.com/mogl/ . Before making any decision to make or hold any investment in the Fund you should consider the PDS in full and any ASX announcements. The information provided is general information only and does not take into account your investment objectives, financial situation or particular needs. You should consider your own investment objectives, financial situation and particular needs before acting upon any information provided and consider seeking advice from a financial advisor or stockbroker. You should not base an investment decision simply on past performance. Past performance is not an indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information.

‘Montaka Global Long Only Fund’ investors: This report was prepared by Montaka Global Pty Ltd, (ACN 604 878 533, AFSL 516 942)( a subsidiary of MFF Capital Investments Limited (“MFF”) (A.B.N 32 121 977 884)), is the investment manager of the Montaka Global Long Only Fund (ARSN: 604 883 418). The responsible entity of the Fund is Fundhost Limited (ABN 69 092 517 087) (AFSL No: 233 045) (Fundhost). While the information in this document has been prepared with all reasonable care, neither Fundhost nor Montaka makes any representation or warranty as to the accuracy or completeness of any statement in this document including any forecasts. Neither Fundhost nor Montaka guarantees the performance of the Fund or the repayment of any investor’s capital. To the extent permitted by law, neither Fundhost nor Montaka, including their employees, consultants, advisers, officers or authorised representatives, are liable for any loss or damage arising as a result of reliance placed on the contents of this document. You should not base an investment decision simply on past performance. Past performance is not an indicator of future performance. Returns are not guaranteed and so the value of an investment may rise or fall. This document has been prepared for the purpose of providing general information, without taking account your particular objectives, financial circumstances or needs. You should obtain and consider a copy of the Product Disclosure Statement (PDS) relating to the Fund before making a decision to invest. The PDS and Target Market Determination are available on this webpage: https://montaka.com/mglof/

Podcast: Join the Montaka Global Investments team on Spotify as they chat about the market dynamics that shape their investing decisions in Spotlight Series Podcast. Follow along as we share real-time examples and investing tips that govern our stockpicks. Click below to listen. Alternatively, click on this link: