|

Getting your Trinity Audio player ready...

|

Many expect India to become a cornerstone of global growth and the next major frontier for investors in their pursuit of value. While India’s ultimate “breakout” is expected to map something similar to the Chinese economy, the timing of it is the subject of an open debate, however most agree we will likely see it take shape at some point over the next 10-15 years.

As brief context, India houses the world’s second largest population (1.4 billion people), which are part of the world’s largest democracy, however only has the world’s 15th largest economy (by GDP) and is very poor with 139th position on the wealth table (by GDP per capita). What excites observers most however, is perhaps the Indian population demographics with over 50% of the population under the age of 25 and more than 65% below the age of 35. In fact, by 2020 the average age of an Indian will be 29 years, compared to 37 for China and 48 for Japan (Australia and the U.S. will be 40). This alone provides the country with an enormous structural tailwind and opportunity for growth, as the working population explodes along with consumption. However there are numerous impediments that stand in the way of India’s development, including corruption, bureaucracy, lack of infrastructure, extreme pollution, poverty, etc. which will need to be addressed to varying degrees in order for it to fully emerge.

Within this amazing Indian construct, we will likely see many industries “breakout” and Indian companies assume globally significant positions from a valuation perspective, much like China has done over the last 10+ years. One of the most exciting areas that we have observed at Montaka Global is in the field of media, specifically the video streaming market (aka Over-The-Top / OTT).

A recent paper by the Boston Consulting Group (BCG) estimates that India’s media consumption grew at ~9% CAGR over the last 6 years, which is 2x the rate of China and 9x that of the United States. BCG contend that the future is even brighter for India’s OTT market which will increase tenfold to $5 billion in the next 5 years. Given the penetration of video streaming in India was only 16% of total media consumption versus 25% in China and 39% in the U.S. the addressable market could be enormous. In another recent piece of work, this time by Ernst & Young (EY), it is estimated that 500 million people in India will watch digital content online by 2020, a doubling from the 250 million that watched in 2017 (indicating that penetration is likely to eclipse that of China based on current trends).

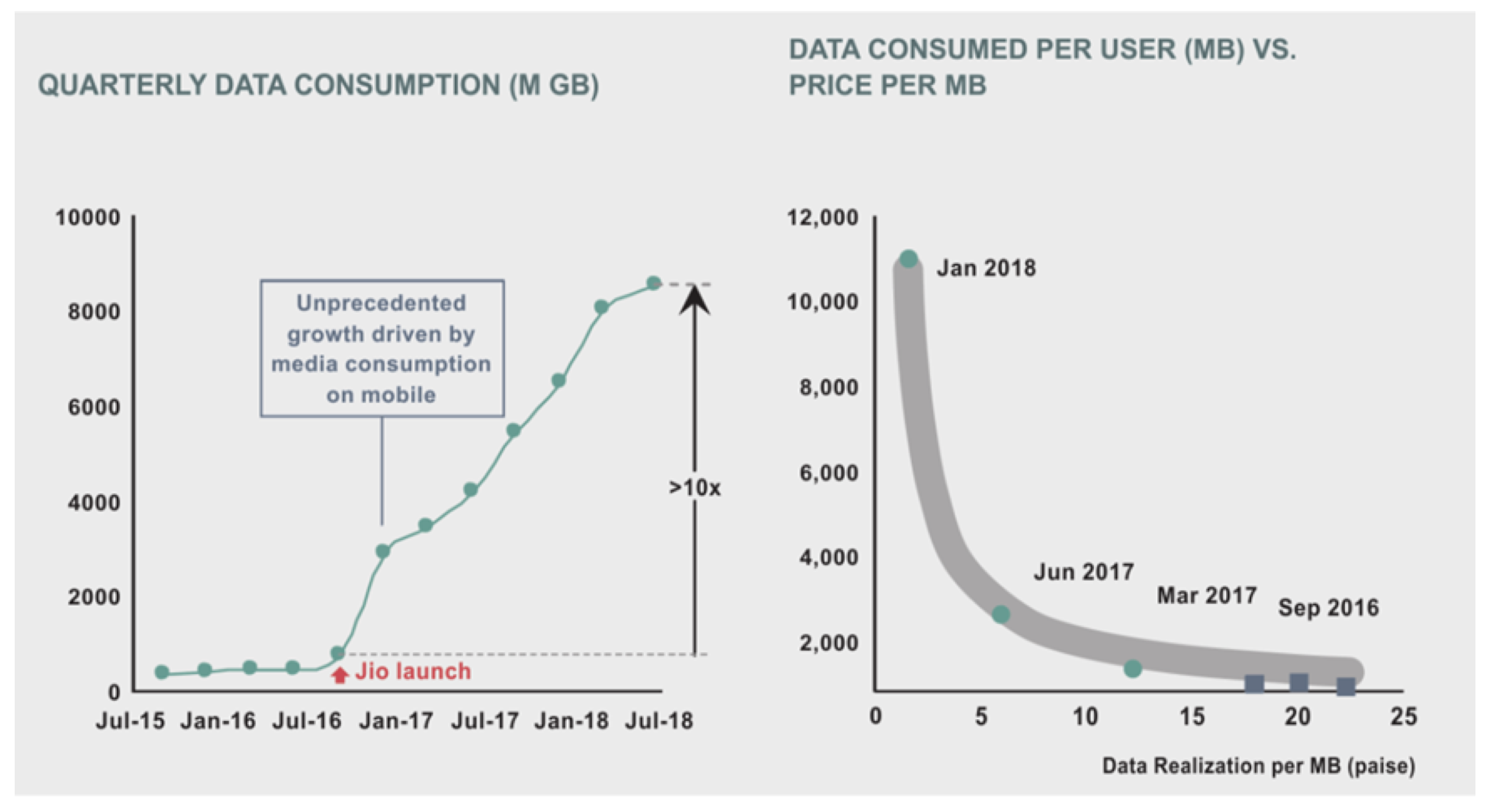

A key driver of all this streaming is increasing smartphone penetration, which was accelerated by the highly disruptive investments made by Mukesh Ambani, Asia’s richest man (#11 in the world) via his mighty Reliance conglomerate and the creation of Jio, the ultra-low cost, 4G-enabled network which has enabled millions of Indians to watch digital video content for the first time. Ericsson estimates that there will be 925 million internet-enabled phones in India by 2023 with nearly 50% of internet growth in India expected to come from rural areas. This is important given almost all rural users prefer content in their local language with EY estimating rural Indians consume regional language content 93% of the time versus English (India is a country of 1.4 billion people and 22 languages, the largest being Hindi with 420 million speakers).

Indian Data Consumption Accelerated by Jio

Source: Boston Consulting Group

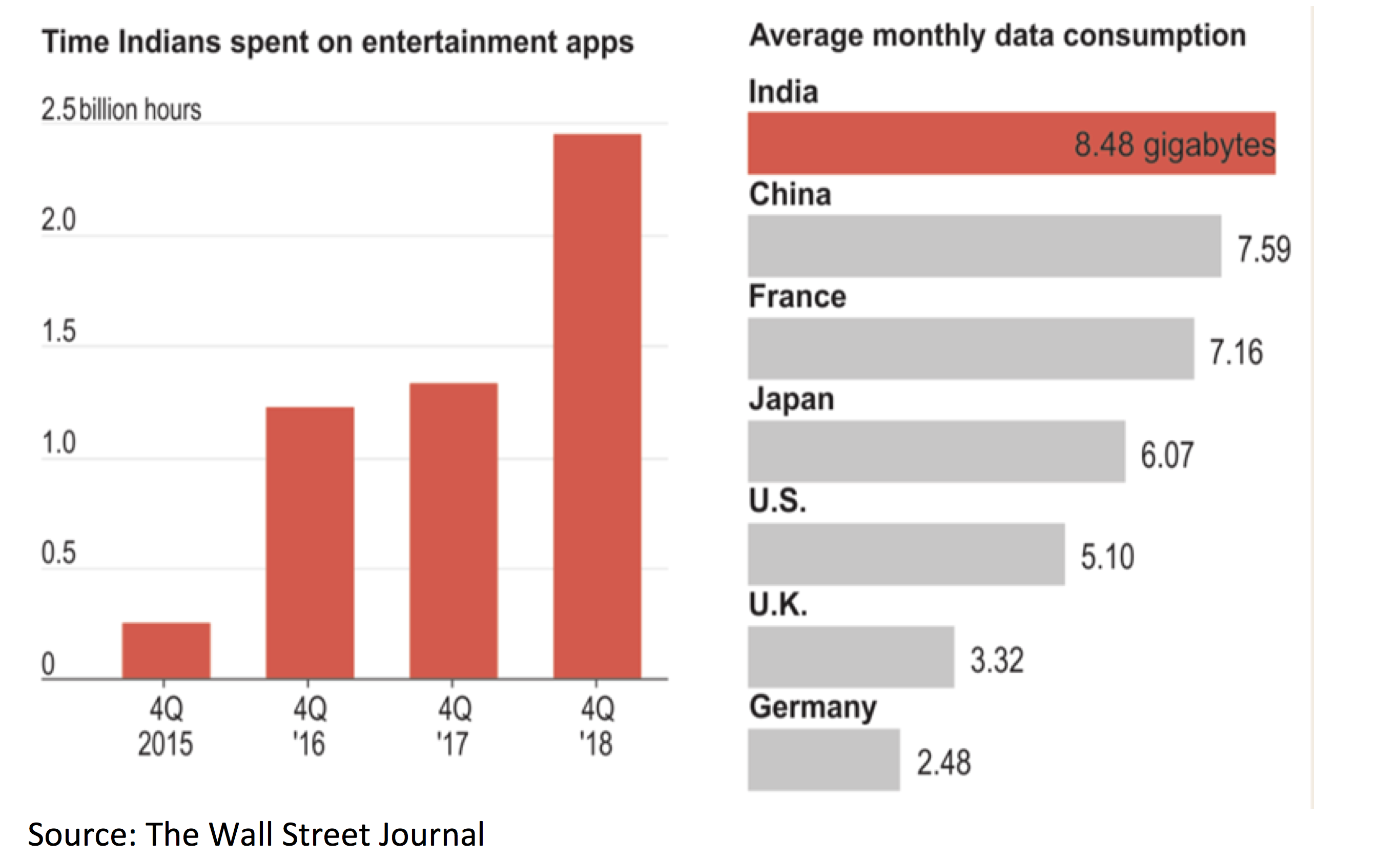

Mobile video consumption is soaring in India with streaming on handsets having risen 10x in the last 3 years alone. In fact, Indian mobile-internet users are the most data intensive in the world, consuming an average 8.5 gigabytes of data per month or the equivalent of 40 hours of video per month.

Indians Already Consume the Most Data in the World Per User

Source: The Wall Street Journal

So what does this potentially mean for investors? Well the Indian OTT market is extremely crowded currently with over 30 competitors which is likely to consolidate in order to increase profitability. Second, digital advertising is expected to increase exponentially with India’s digital advertising market only generating $2 billion in revenues per year, which is less than 2% of the >$100 billion market in the U.S. despite India having a population that is 4-5x as large. In fact, KPMG predicts that domestic digital advertising revenues in India could triple to $6 billion in the next 5 years.

This of course would bode well for our Alphabet (GOOGL) and Facebook (FB) positions which both have significant user bases in India and world leading digital advertising platforms. Both GOOGL and FB are heavily investing in growing their video businesses particularity GOOGL via its YouTube platform. In its most recent earnings (Q4 2018) GOOGL highlighted a significant increase in investment in YouTube content and has already tailored its platform for Indian consumers, enabling regional languages voice-search (via its world leading AI engine), helping overcome the English language barrier, in addition to automatically reducing video quality where network bandwidth is low.

The future is bright in Indian video streaming and the team at Montaka Global hope to capture some of that light for our investors via intelligent investments in the portfolio.

Montaka owns shares in Facebook and Alphabet

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.