|

Getting your Trinity Audio player ready...

|

In April 2016 I wrote an article on Pitney Bowes (NYSE: PBI), a company the Montaka Global Fund was short. The premise of the article was to highlight a key component of the Montaka short framework: Thematics / Structural Declines. This article will provide an update on how our short thesis panned out, with the PBI story exemplifying the difficulties companies face when up against industry headwinds.

As a recap, PBI sells machines which automate the mail generation process. For example, a large bank has enormous mailing volumes, with potentially millions of statements being mailed to customers. PBI’s machines can print the document, fold it, insert it into an envelope, and then stamp it. The benefits of a PBI machine over a manual process are obvious. However, mail volumes are in long-term structural decline, and this has posed significant challenges for PBI, particularly as more than 90% of the company’s earnings are mail-related.

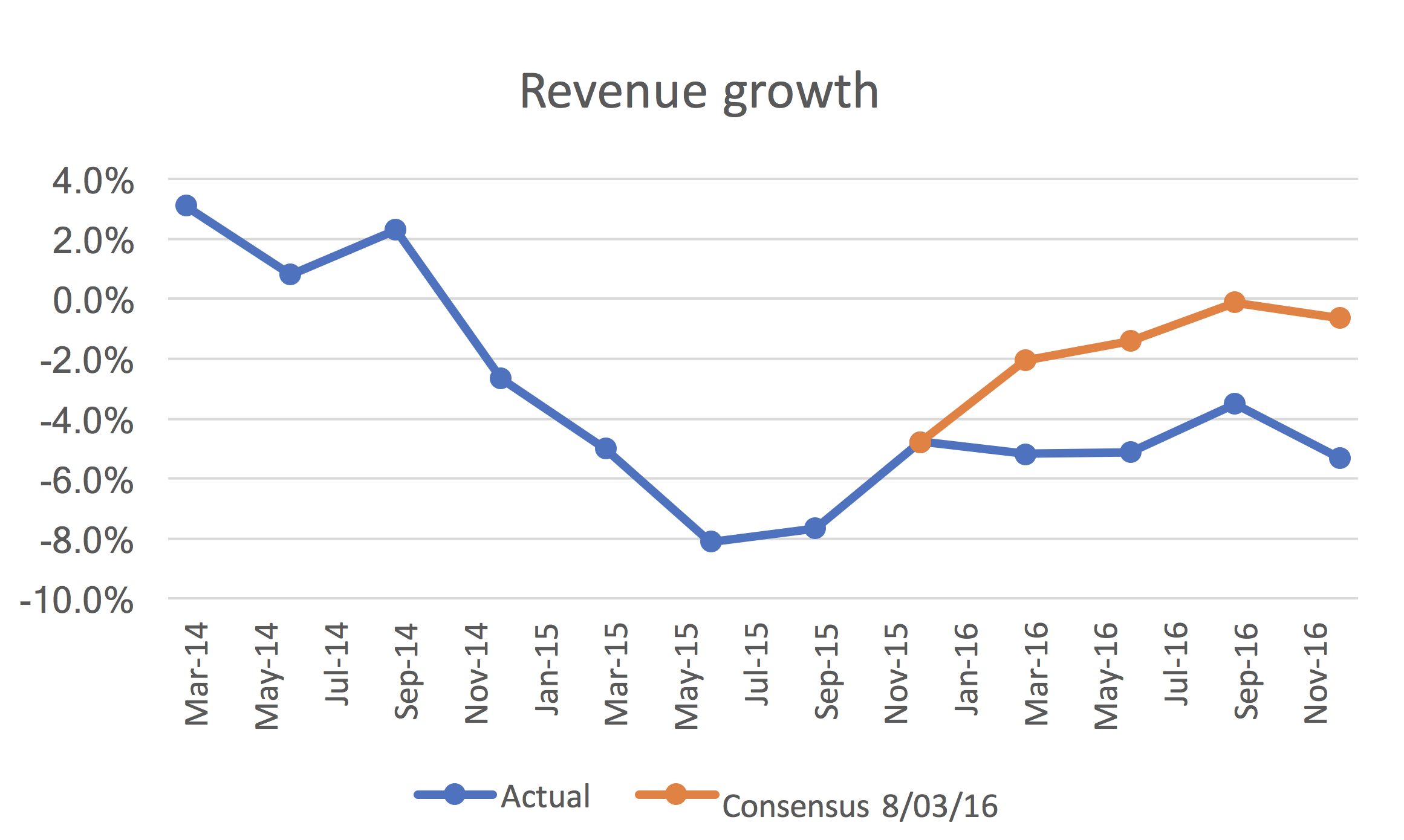

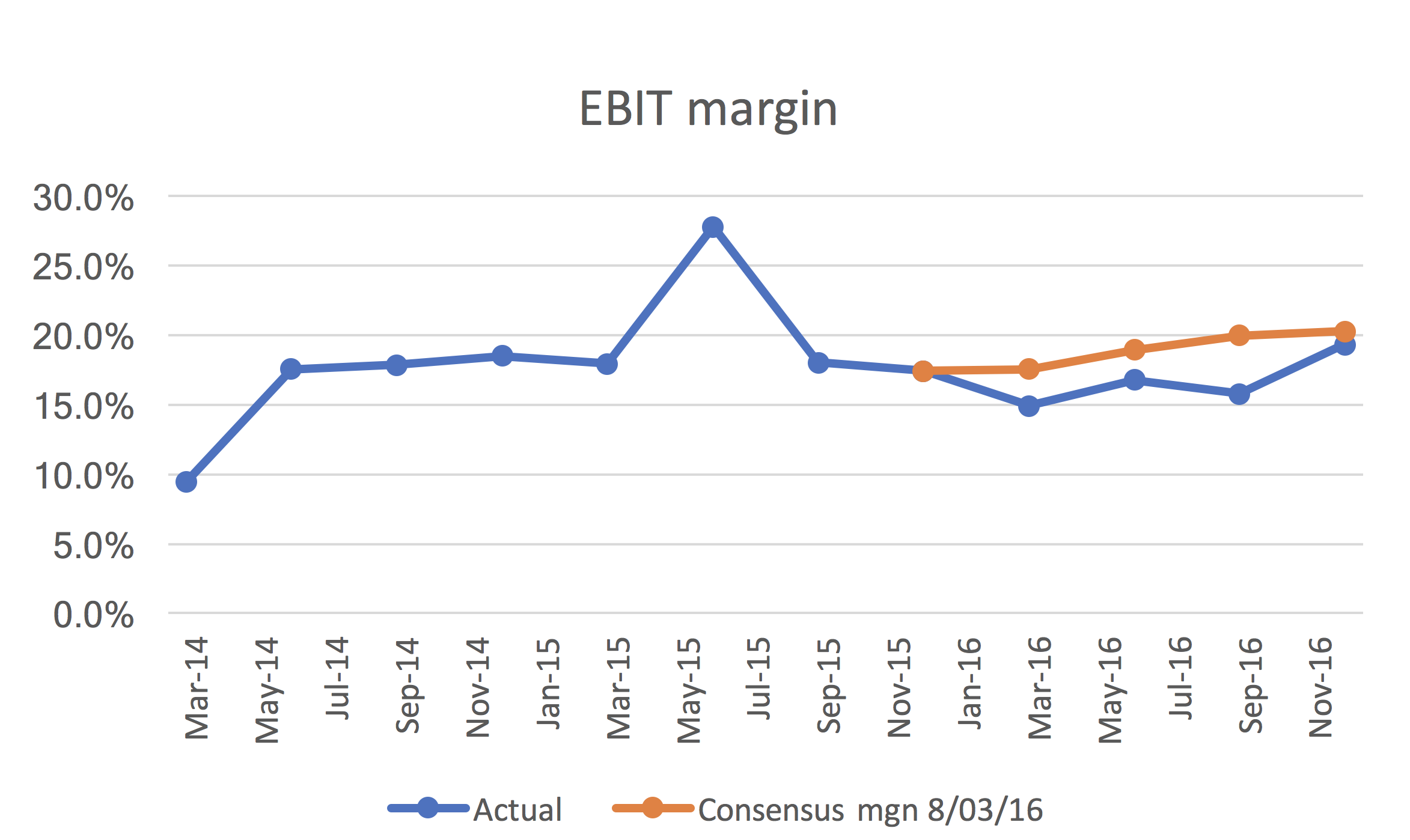

In light of this backdrop of structural headwinds impacting mail volumes, we formed the view that consensus expectations for revenue growth and margins were too optimistic. The below charts show consensus expectations in March 2016. What is clear, is that the actual revenue and EBIT margins came in below what sell-side analysts were forecasting.

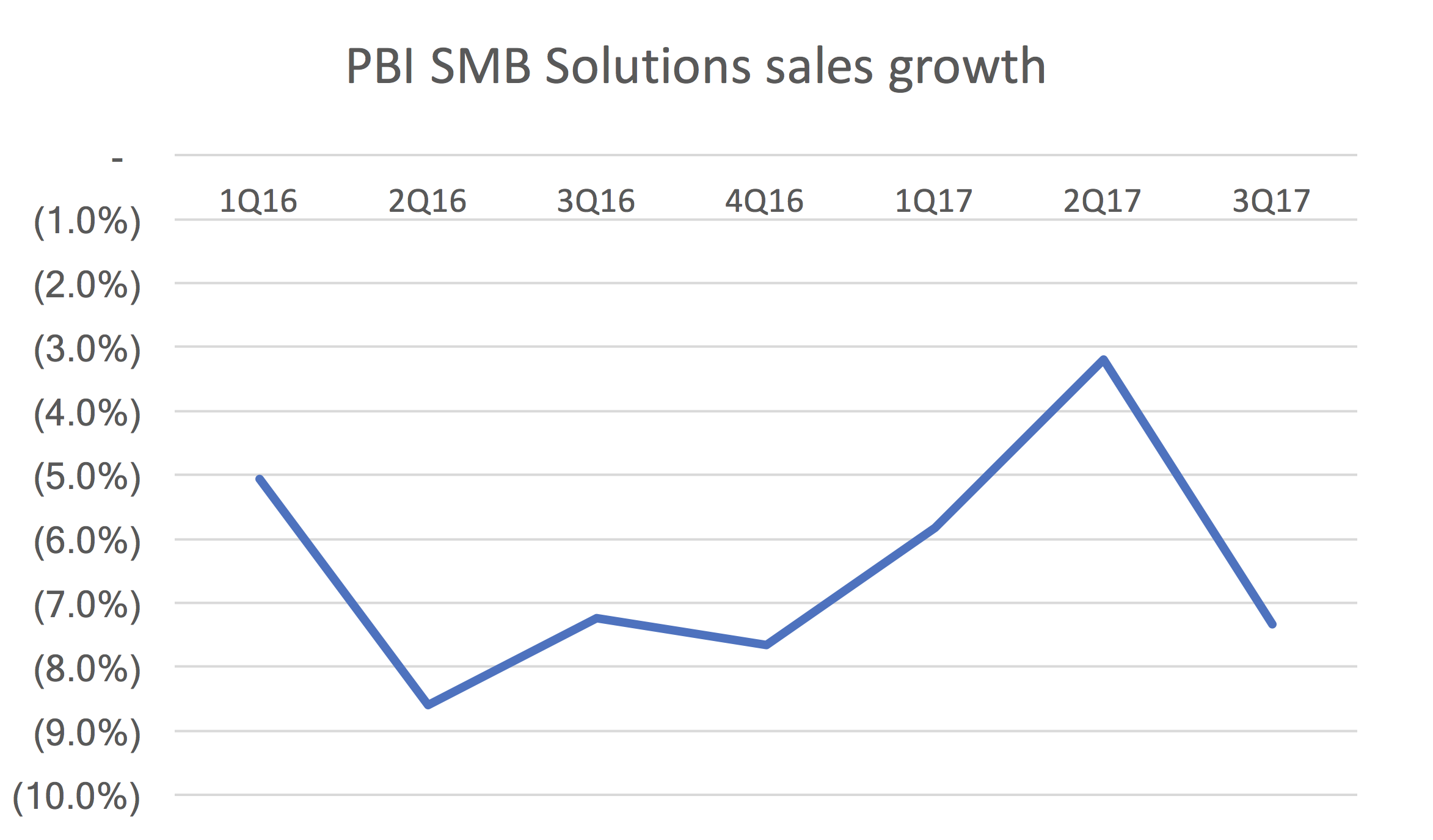

What has occurred since early 2016 has been deteriorating financial performance and repeated guidance downgrades by PBI. The company’s core mailing business, the Small and Medium Business (SMB) Solutions Group, has faced prolonged revenue declines.

In an environment where firms are shifting towards e-statements to save costs, email continues to usurp mail correspondence, and mail advertising dollars are shifting to online channels, the headwinds faced by PBI are real and significant. In light of this, the declines in PBI’s core mailing business are perhaps unsurprising. The structural decline of mail volumes has been occurring over many years and is likely to continue. There is nothing PBI can do to stop this. Instead it must try and manage this virtually inevitable decline.

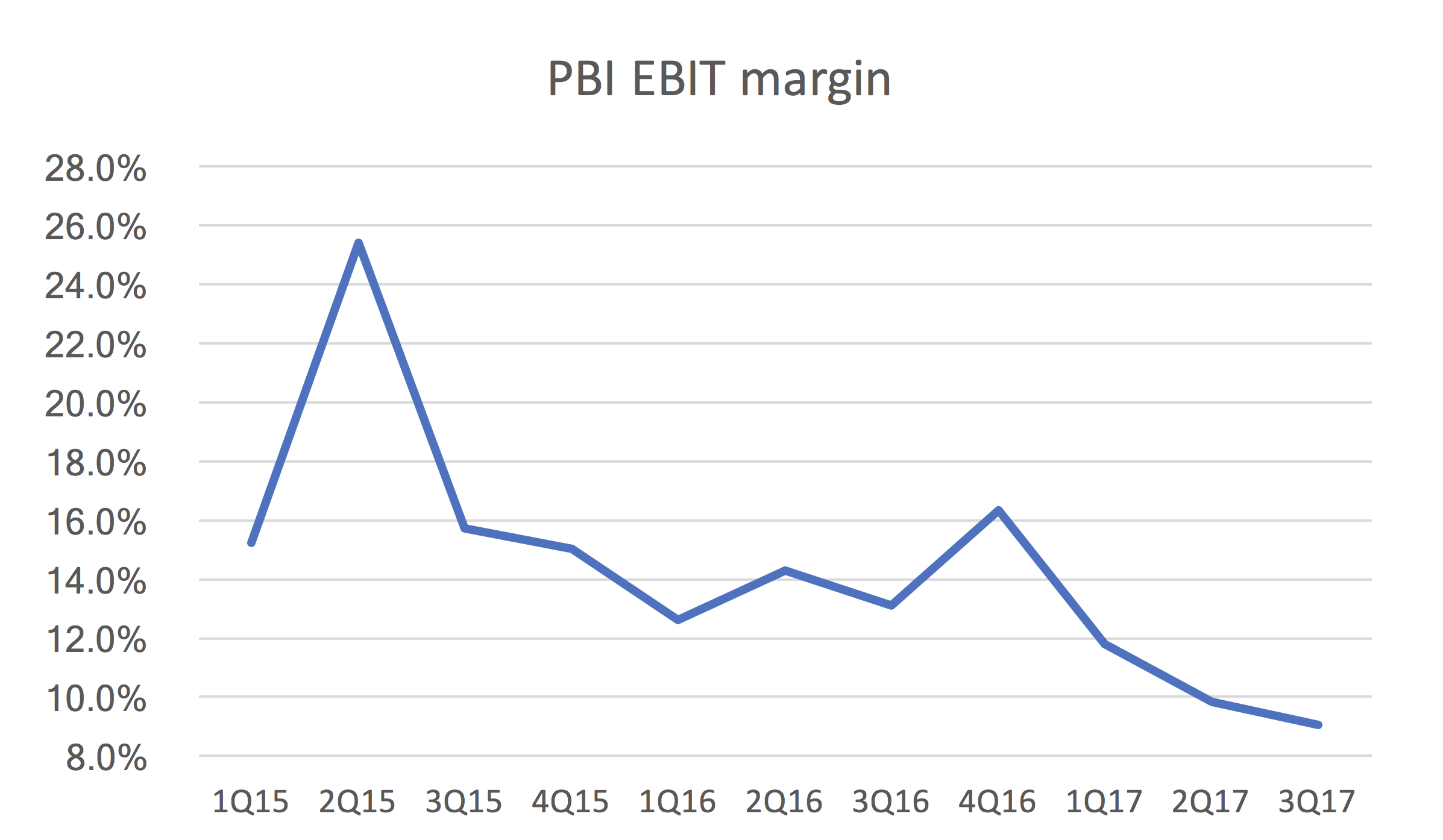

PBI’s shrinking revenues, in addition to a mix shift to lower margin revenue streams, has led to a particularly ugly margin decline, with PBI’s EBIT margin collapsing by more than 600 bps over the last two years.

The company recently reported its third quarter 2017 earnings and the stock declined 17% in the subsequent trading session. PBI yet again downgraded their FY17 EPS guidance, and the market lost patience. We decided that at these price levels the risk/reward had become less attractive, and we have since covered our PBI short position, producing a nice profit for our investors.

![]()

George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.