As 2019 is now well and truly underway, we thought it was timely to provide a quick summary of our near-term global economic observations. As readers will know all too well, at Montaka we pay close attention to global macro trends, despite seeing ourselves primarily as bottom-up investors. While every stock thesis – both long and short – needs to be sound on a bottom-up basis, we also seek to ensure that our portfolio in its aggregate is positioned in a way consistent with how we are seeing the world.

Here are six charts that summarize some of the key insights that we believe are relevant for global investors today and will inform how global equity portfolios should be positioned through the course of 2019.

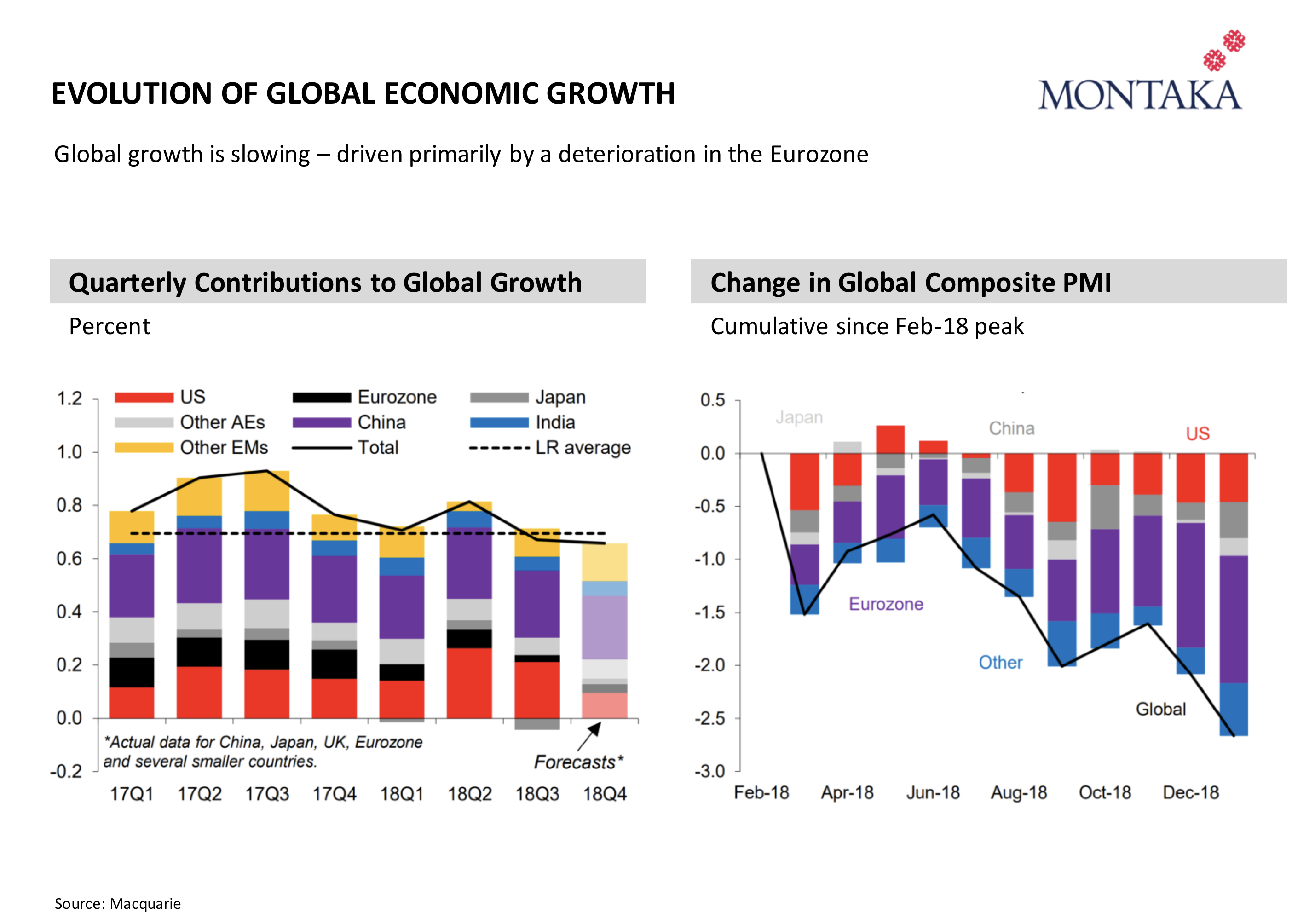

First, it is clear that global economic growth is gradually slowing. And interestingly, the major source of the deterioration is the Eurozone. Indeed, as can be observed in the chart below on the right, the Eurozone has driven around two-thirds of the total decline in the global PMI (Purchasing Managers’ Index) over the last 12 months. In large part, this has stemmed from weaker European exports to Turkey (not to China as most would assume).

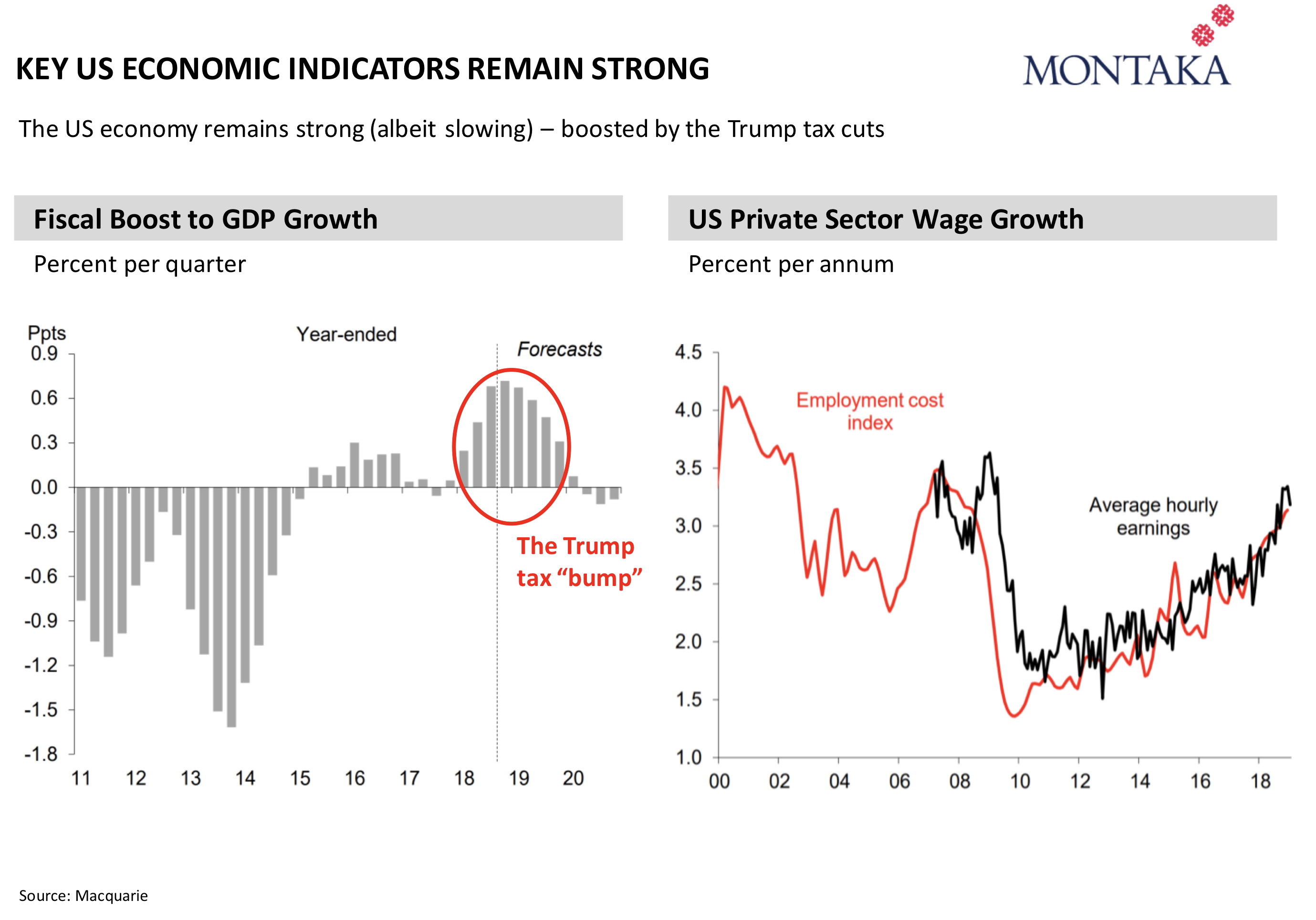

Second, the US economy remains strong. Employment is low, wages are growing, households have significantly delevered post the 2008 crisis, the banking system is very well capitalised and interest rates remain low. Many are confused by the significant amount of “commentary” about an impending US recession. Your author believes the source of confusion is around the varying definitions that exist out there for what constitutes a recession. For instance, some define a recession as two consecutive quarters of negative GDP growth. On this measure, the US is nowhere near a recession. Meanwhile, the National Bureau of Economic Research (NBER) defines a recession as a significant decline in economic activity and measures from the peak of the business cycle to its trough. On this measure, perhaps the US is already in recession – but we will only know for sure years into the future.

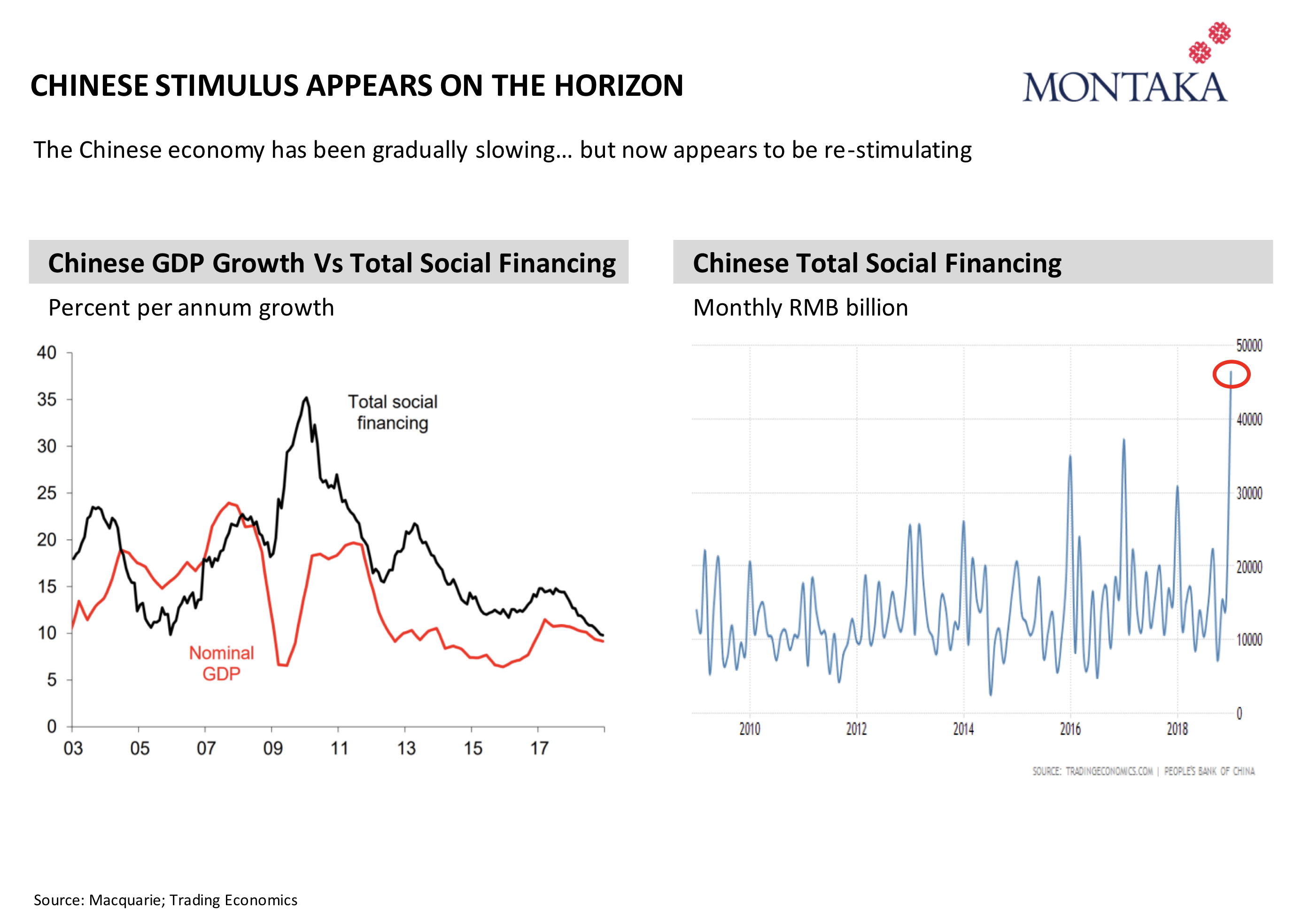

Third, the Chinese economy continues to slow gradually. This will not be new news to anyone. What is new, however, is that we now believe we have clear evidence of material stimulus. Days ago, the People’s Bank of China (PBOC) disclosed a record level of total social financing in the month of January – coming in around 50 percent higher than analyst expectations. As illustrated by the chart below on the right, the monthly injection of credit into the Chinese economy dwarfs all others. This should boost Chinese aggregate demand over the coming months.

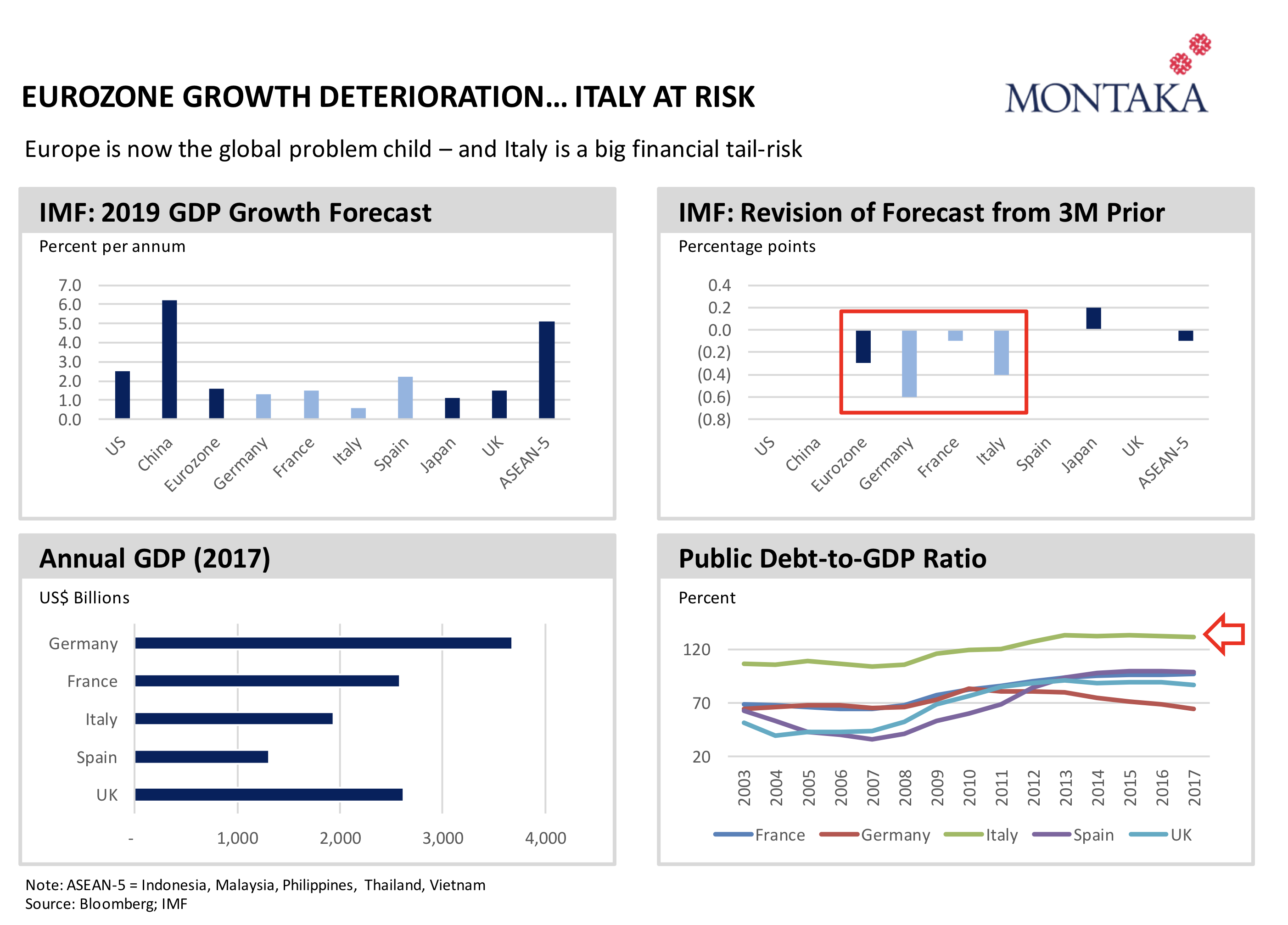

Fourth, just weeks ago, the IMF significantly downgraded its global growth forecasts – primarily as a result of downgrades to major Eurozone economies, including Germany, Italy and France. Weaker growth is particularly bad news for Italy – and not just for its labor market (youth unemployment is already at 30-35%, for example). Italy’s public balance sheet is particularly stretched with government debt-to-GDP north of 130 percent. As growth slows, so too will its primary budget surplus (that is, Italy’s annual budget surplus before interest expenses). And this means there is little conceivable way for Italy to escape its public debt trap.

And this is bad news for the entire Eurozone. Italy is the EU’s third-largest economy with an annual GDP in the order of US$2 trillion. If it is true that the Italian government finds itself in an unsustainable debt-trap, then the probability of either a write-down of Italian sovereign debt, or an exit from the European Monetary Union (EMU), or both, increases. Such a scenario would be a financial catastrophe for the EU and world – at least in the short run. As such, Montaka recently re-initiated a short position in an Italian insurer which is a major owner of Italian sovereign bonds (which incidentally are treated as “risk-free assets” by the regulatory authorities who set capital requirements).

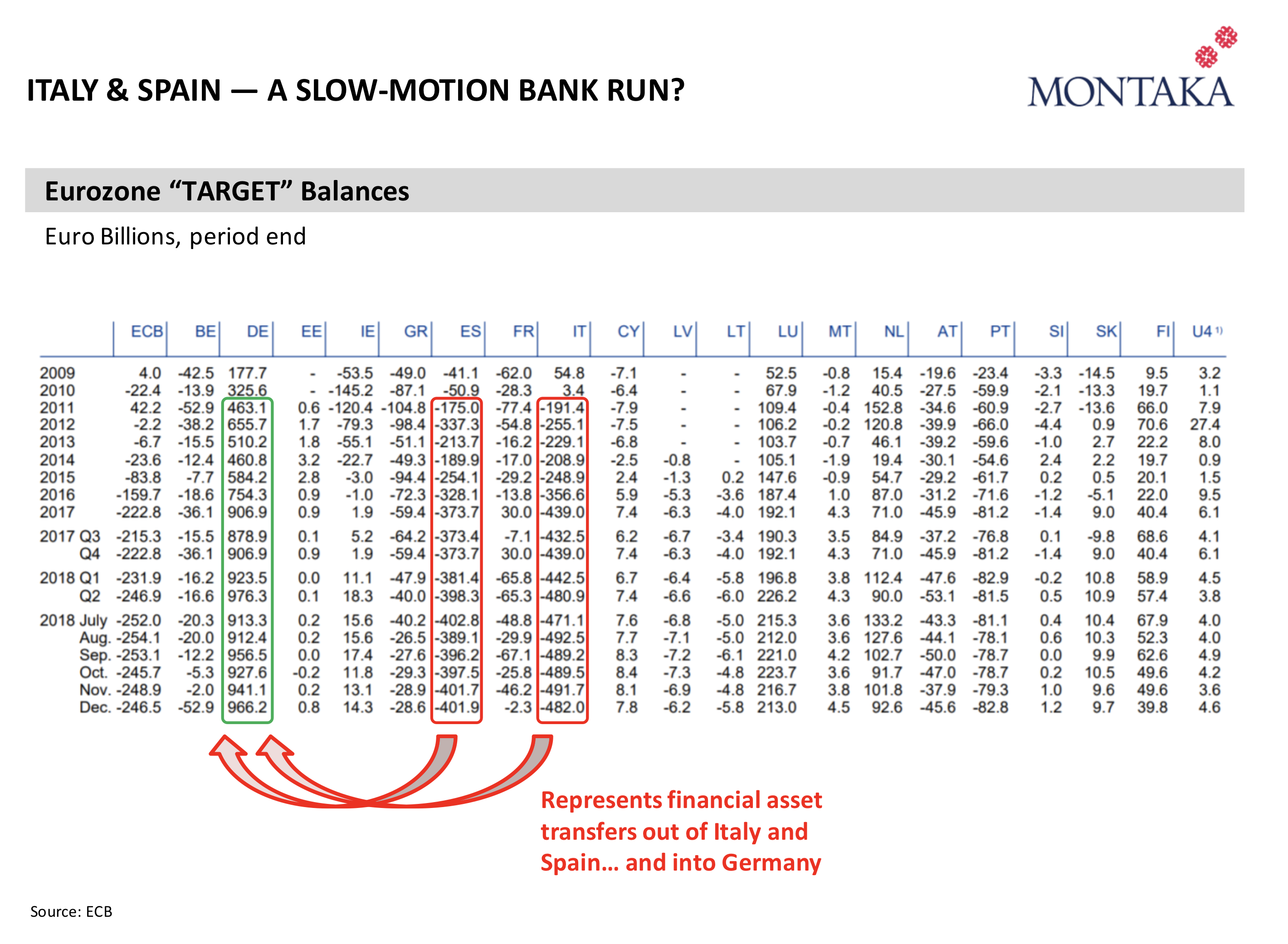

We also note a continuation of financial asset transfers by Italian and Spanish residents to Germany. We have been monitoring this trend for the last 10 years and it is showing no signs of reversing. In theory this trend is sustainable as long as the EMU remains intact. Already, however, we are hearing noises from German economists who are flagging this trillion Euro asset on the balance sheet of the Bundesbank as being at risk should politicians from countries like Italy talk about leaving the EMU.

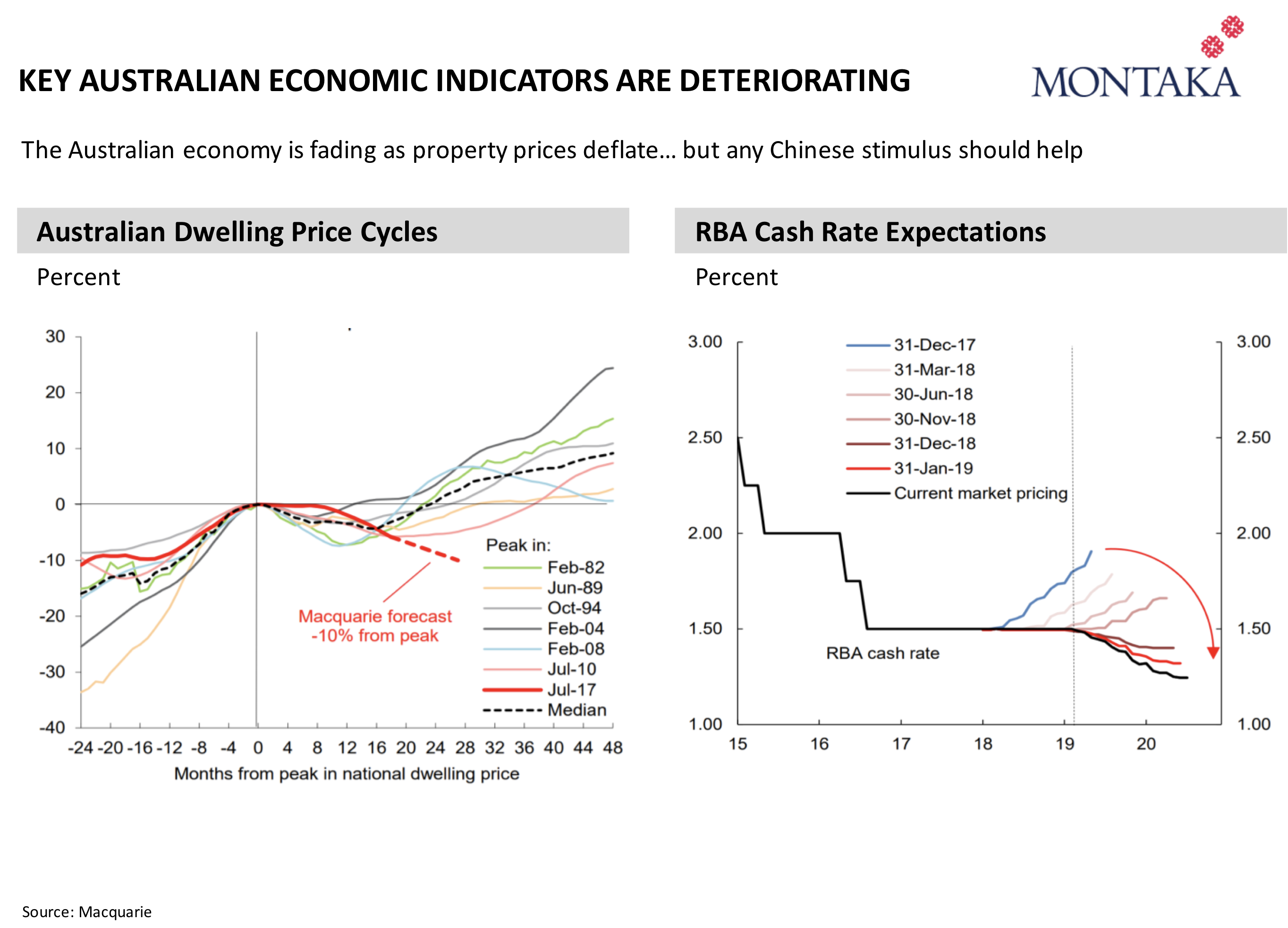

Finally, the Australian economy is clearly deteriorating. We believe this weakness is substantially the result of deflating property prices in key housing markets across the country. As prices fall, so too does the “wealth effect” go into reverse and impair consumption. The deterioration in RBA cash rate expectations paints a clear picture of an economy which is now expected to continue operating below its capacity for some time to come. That said, to the extent China is pursuing a material stimulation of its economy, this should result in an exogenous boost to Australian economic growth later in 2019.

Given the observations we have described above, we have made a number of minor changes to the exposures in Montaka’s portfolio. Specifically, we have reduced our exposures to EUR and RMB, increased our exposures to USD, JPY and AUD; and we have increased our Italian short book exposure.

Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Around the world in six charts

As 2019 is now well and truly underway, we thought it was timely to provide a quick summary of our near-term global economic observations. As readers will know all too well, at Montaka we pay close attention to global macro trends, despite seeing ourselves primarily as bottom-up investors. While every stock thesis – both long and short – needs to be sound on a bottom-up basis, we also seek to ensure that our portfolio in its aggregate is positioned in a way consistent with how we are seeing the world.

Here are six charts that summarize some of the key insights that we believe are relevant for global investors today and will inform how global equity portfolios should be positioned through the course of 2019.

First, it is clear that global economic growth is gradually slowing. And interestingly, the major source of the deterioration is the Eurozone. Indeed, as can be observed in the chart below on the right, the Eurozone has driven around two-thirds of the total decline in the global PMI (Purchasing Managers’ Index) over the last 12 months. In large part, this has stemmed from weaker European exports to Turkey (not to China as most would assume).

Second, the US economy remains strong. Employment is low, wages are growing, households have significantly delevered post the 2008 crisis, the banking system is very well capitalised and interest rates remain low. Many are confused by the significant amount of “commentary” about an impending US recession. Your author believes the source of confusion is around the varying definitions that exist out there for what constitutes a recession. For instance, some define a recession as two consecutive quarters of negative GDP growth. On this measure, the US is nowhere near a recession. Meanwhile, the National Bureau of Economic Research (NBER) defines a recession as a significant decline in economic activity and measures from the peak of the business cycle to its trough. On this measure, perhaps the US is already in recession – but we will only know for sure years into the future.

Third, the Chinese economy continues to slow gradually. This will not be new news to anyone. What is new, however, is that we now believe we have clear evidence of material stimulus. Days ago, the People’s Bank of China (PBOC) disclosed a record level of total social financing in the month of January – coming in around 50 percent higher than analyst expectations. As illustrated by the chart below on the right, the monthly injection of credit into the Chinese economy dwarfs all others. This should boost Chinese aggregate demand over the coming months.

Fourth, just weeks ago, the IMF significantly downgraded its global growth forecasts – primarily as a result of downgrades to major Eurozone economies, including Germany, Italy and France. Weaker growth is particularly bad news for Italy – and not just for its labor market (youth unemployment is already at 30-35%, for example). Italy’s public balance sheet is particularly stretched with government debt-to-GDP north of 130 percent. As growth slows, so too will its primary budget surplus (that is, Italy’s annual budget surplus before interest expenses). And this means there is little conceivable way for Italy to escape its public debt trap.

And this is bad news for the entire Eurozone. Italy is the EU’s third-largest economy with an annual GDP in the order of US$2 trillion. If it is true that the Italian government finds itself in an unsustainable debt-trap, then the probability of either a write-down of Italian sovereign debt, or an exit from the European Monetary Union (EMU), or both, increases. Such a scenario would be a financial catastrophe for the EU and world – at least in the short run. As such, Montaka recently re-initiated a short position in an Italian insurer which is a major owner of Italian sovereign bonds (which incidentally are treated as “risk-free assets” by the regulatory authorities who set capital requirements).

We also note a continuation of financial asset transfers by Italian and Spanish residents to Germany. We have been monitoring this trend for the last 10 years and it is showing no signs of reversing. In theory this trend is sustainable as long as the EMU remains intact. Already, however, we are hearing noises from German economists who are flagging this trillion Euro asset on the balance sheet of the Bundesbank as being at risk should politicians from countries like Italy talk about leaving the EMU.

Finally, the Australian economy is clearly deteriorating. We believe this weakness is substantially the result of deflating property prices in key housing markets across the country. As prices fall, so too does the “wealth effect” go into reverse and impair consumption. The deterioration in RBA cash rate expectations paints a clear picture of an economy which is now expected to continue operating below its capacity for some time to come. That said, to the extent China is pursuing a material stimulation of its economy, this should result in an exogenous boost to Australian economic growth later in 2019.

Given the observations we have described above, we have made a number of minor changes to the exposures in Montaka’s portfolio. Specifically, we have reduced our exposures to EUR and RMB, increased our exposures to USD, JPY and AUD; and we have increased our Italian short book exposure.

Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Around the world in six charts

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.