|

Getting your Trinity Audio player ready...

|

Envision a scenario where a firm’s auditor declines to be reappointed, and the firm subsequently struggles to find a replacement auditor. Furthermore, that same company asks the government for clarification around the powers of the secretary of state to appoint an auditor to a public company in the event that no replacements can be found. When presented with the above facts, one would presume that the situation for that company is dire at best. The stock market agreed, sending the share price of Sports Direct (LSE: SPD) down 10% on the day the news was announced.

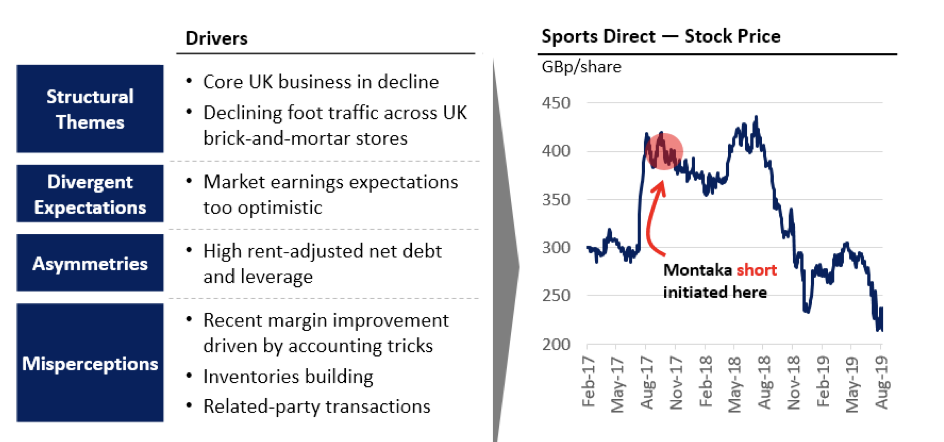

Sports Direct, a stock that Montaka has been short, announced on 14 August 2019 that Grant Thornton, the firm’s auditor since it listed in 2007, had expressed its intention to not seek reappointment as SPD’s auditor. Ordinarily, this might cause only minimal disruption. After all, a firm can simply appoint another auditor. In its preliminary results for FY19, SPD signalled difficulties the company was facing in persuading one of the “big 4”accounting firms to take on the role of SPD’s auditor:

“Our early discussions with the big 4 have thrown up some barriers; Deloitte who do our tax compliance and advisory work cannot perform audit work at the same time and thus would currently be unable to tender. KPMG have indicated conflicts of interest based on an existing portfolio of clients, however we do not believe based on our understanding of big 4 independence procedures that this is insurmountable. EY had some reluctance based on their close proximity to the House of Fraser administration which they ran, however as time has passed we do not believe this should be a barrier when a tender process is run. PwC have had some widely publicised fines in recent years and we understand there is a reluctance to engage based on our ownership structure.”

Mike Ashley, CEO of SPD, essentially ruled out the use of small- to mid-tier accounting firms in his CEO letter due to SPD’s burgeoning complexity, posing further difficulties for the Group in securing an auditor: “The SD Group has grown exponentially in size, geography, and complexity over recent years and we do not believe a firm outside of the Big 4 will potentially be able to cope with such an audit in the future.”

In a remarkable, and possibly unprecedent action, SPD asked the Department for Business, Energy and Industrial Strategy for clarification around whether the UK government is able to appoint an auditor to a public company in the event that it fails to appoint one itself. The UK Companies Act specifies that in the event that a company is unable to appoint an auditor, the secretary of state for the department of business is able to appoint an auditor to that quoted company. To our knowledge there does not appear to be precedent as to how this process works, but regardless, the department of business in a statement to the FT has so far expressed an unwillingness to become involved: “The secretary of state’s powers to intervene only apply in particular circumstances, which do not currently apply here.”

One would have to think that this would be playing on the mind of Mike Ashley, given that in the event that SPD is unable to secure an auditor, the firm will be taken to have contravened the London Stock Exchange listing rules, specifically LR 9.8.10 which requires the auditors to review certain provisions of the Annual Report. In the event that this plays out, SPD would presumably be delisted at some point thereafter if it still fails to appoint an auditor.

This latest announcement by the company is just one of many issues to bubble to the surface for SPD in recent months. In the last month and a half SPD has seen its Retail Chief, Company Secretary, and CFO all depart the company. The company also had to delay the publication of its full-year results multiple times, initially scheduling the release of these results for 18 July 2019, but finally reporting them on 26 July. When combining the reluctance of auditors to take on SPD as a client with these other red flags that we have observed in recent months, it paints the picture of a business with mounting signs of distress.

This is a business facing a crisis, and we continue to believe that the market is still failing to adequately reflect these pressures in the share price. In other words, we believe that there is a high likelihood the stock has further to fall, and a chance that over the years the equity of SPD LN will be wiped out completely.

The Montaka Funds are short shares in Sports Direct.

![]() George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.