|

Getting your Trinity Audio player ready...

|

For years now, there has been an almost-structural increase in the amount of capital allocated to passive equity index funds; and a corresponding decrease in the amount allocated to active equity funds. The rationale has been simple: passive funds are typically much lower cost and their returns have outperformed most active funds over recent years. What’s not to like?

Source: Investment Company Institute; Bloomberg

We are entirely sympathetic to the advantages of passive equity index investing. The value proposition for investors is that they are basically certain to receive the average market return, less the cost of the fund which is typically minimal. Actively-managed equity funds come with the prospect of generating returns higher than the market though are typically accompanied by higher fees. And the market outperformance is far from guaranteed.

In recent years, investors in many actively-managed funds have been frustrated by the ugly combination of higher fees and returns that were less than the market average. For many, this situation has made it easy to make the switch to passive equity index funds.

An interesting question we pose today is the following: does the above calculus change in a structurally lower-returning world?

We’ve suggested on a number of occasions that the future of long-run average equity returns may not look as attractive as they have looked in the past. The reason for this hypothesis is simply that a number of the major drivers of equity returns are likely to present headwinds instead of tailwinds.

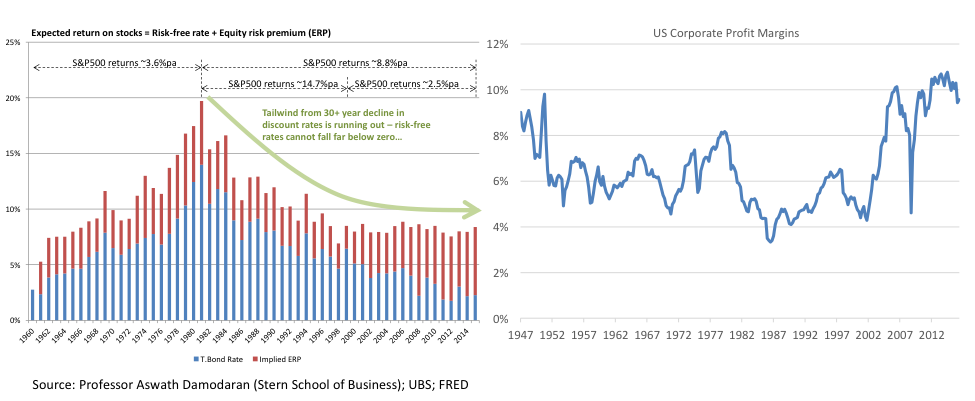

First of all, consider interest rates. Over the last thirty years, interest rates have fallen to zero (or in some cases, are now negative). Lower interest rates make the relative earnings yield of an equity security appear more attractive. The result is an expanded valuation multiple and higher stock price. Should interest rates increase, on the other hand, the reverse becomes true.

Second, corporate profit margins are near all-time highs driven by a period of cost-reduction following the global financial crisis; as well as by reduced interest costs. Costs cannot be cut forever and at some point margins should start to mean-revert via price competition. Compressing margins result in slower earnings growth and relatively weaker stock prices, all else being equal.

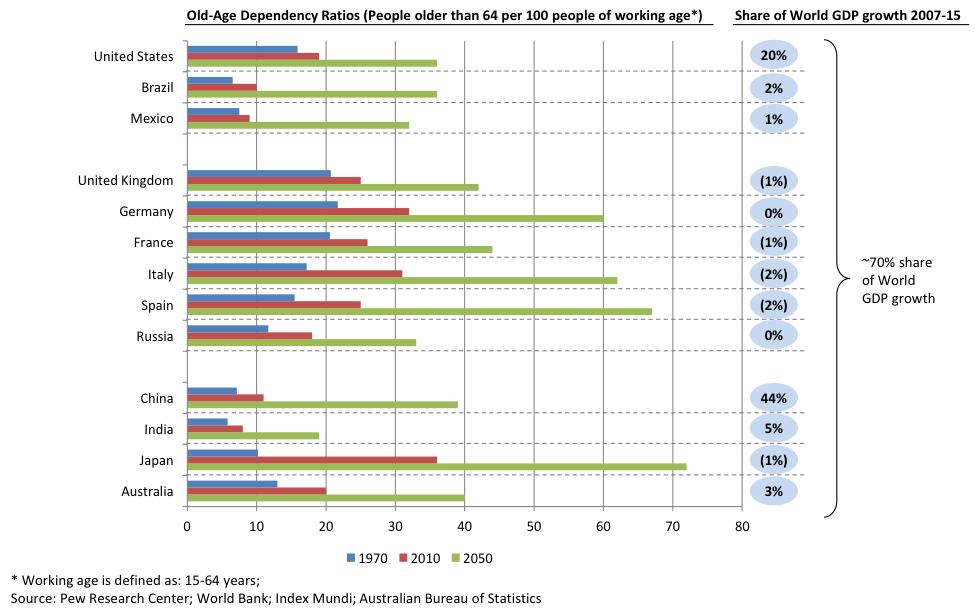

Third, demographics in many parts of the world including North America, China, Europe and Australia are deteriorating. By deteriorating, we mean that the dependency ratio between retirees and workers is increasing at an accelerating rate. Slower growth in the working-age population results in slower GDP growth (all else being equal); while higher growth in retirees likely strains public budgets that fund healthcare and pensions.

From the above three headwinds alone, we suggest there is a high probability that future long-run average equity returns will not be as attractive as they have been over the past 30 years. But for a passive equity investor, the return which is absolutely assured is this precise average long-run equity return. Nothing more, nothing less (except for the management fee).

For a high-quality active manager, on the other hand, he (or she) retains the opportunity to outperform the market, despite a typically higher fee structure. And in a low-returning environment, any outperformance – even a small outperformance – becomes a relatively higher share of the overall total return. And over the long term, this outperformance results in serious value accretion.

Imagine, hypothetically, that the equity market will give you an average return of only 5% per annum for the next 20 years. Well, if you can identify an active manager that can add just 3% per annum in outperformance after fees, then this manager will add an extra 76% to your capital base relative to where it would have been in a passive equity index strategy, at the end of 20 years.

And should your manager be even more capable and can deliver an extra 6% per annum in outperformance, then your capital base will be triple what it would have been under a passive equity index strategy, at the end of 20 years. These simple calculations help demonstrate the relative value of outperformance in a low-returning world.

We encourage investors to consider carefully what makes sense for them. Proponents of passive equity funds argue that it is better to lock in the market index return than risk missing it with an active manager. But in a low-returning world, how sensible is it to lock in this market index return?

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.