|

Getting your Trinity Audio player ready...

|

On January 15, 2019, Netflix announced that it would be raising the monthly prices on all three tiers of its subscription streaming service by as much as 18%, barely 15 months since the last price increase. This news was well received by the market, as any price increase is pure profit for Netflix that can then be reinvested into more content to drive more subscriber growth (if we ignore cash flow). Taken in a vacuum, one would be forgiven for thinking that Netflix has a monopolistic grip on online video streaming. But a significant shake-up is coming to the industry this year, and the timing of Netflix’s price increase can scarce be interpreted as anything less than a pre-emptive and necessary, albeit risky, land grab.

This year, Disney will launch its long-awaited Disney+ streaming service (and remove its content from Netflix) while beefing up its now majority-owned Hulu platform with recently acquired Fox content; AT&T’s WarnerMedia will launch a streaming platform in late 2019; NBCUniversal revealed plans to launch an ad-supported streaming service in early 2020; and Apple has been rumoured to be developing a content business. Some of these media companies may want to regain exclusivity of owned content for their own streaming services and follow Disney’s lead in pulling their owned content off the likes of Netflix. Given this pipeline, what is the strategy behind Netflix’s price hike and how will its pre-emptive strike affect the competition that will follow?

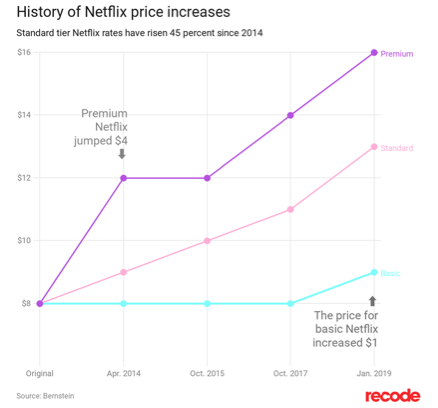

Unfettered pricing power is one of the most attractive competitive advantages for any company, and Netflix is no exception. When we look at Netflix’s pricing history, two things stand out – not only has the magnitude of price increases increased, the frequency is also increasing. The latest price increase comes only 15 months after the previous increase compared to 24 months last time.

Management’s justification for price increases has always been that Netflix is priced based on the value that the service provides to subscribers. While this is undoubtedly true, it is also hard to verify. Netflix doesn’t disclose what portion of viewing hours is original content, so it is difficult to determine if subscribers are really valuing and paying for Netflix original content (which is growing) or licensed content (which is shrinking). One could argue that Netflix is pre-emptively extracting a higher share of the entertainment wallet while competition is limited, thus leaving a smaller share of wallet for the new competitors to fight over. This would certainly hinge on subscribers valuing Netflix original content more than licensed content and would be positive for Netflix’s future pricing power in the face of tougher competition.

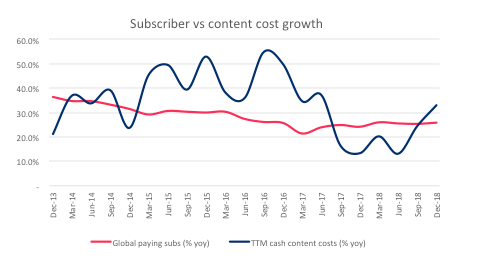

On the other hand, one could also argue that the price was increased out of necessity. The operating leverage inherent in a high fixed cost content business means the optimal strategy is to amortise said content costs over as many subscribers as possible. If subscriber growth exceeds the growth in content costs, then the business should not need to rely on pricing to fund content growth (yet). But if subscriber growth slows, pricing becomes an important contributor to sustaining the same level of content growth.

Source: company filings, MGI

While Netflix’s subscriber growth is still on the steepening section of the S curve for now, one can hypothesise that the new streaming services (particularly Disney) could put downward pressure on Netflix’s subscriber growth while putting upward pressure on content cost growth (to continue delivering differentiated content). If this is the case, pricing would be necessary to offset the slower subscriber growth. And if it is necessary for Netflix to raise prices, it is certainly easier to do so now, before the competing services have launched, rather than later.

Regardless of how one interprets the Netflix price increase, what is certain is that the launch of competing streaming services will result in the fragmentation of streaming video entertainment. The traditional cable bundle unravelled because consumers were fed up with paying a high and rising fixed cost for content that they weren’t interested in watching. Now consumers could face the opposite problem – overwhelmed by an extensive a la carte menu of $5-$15/month streaming options that can quickly add up to more than the old cable bill. In such an environment, two considerations will move to the forefront: original content and convenience.

As Ben Bajarin of Tech.pinions writes, storytelling becomes critical in a world where subscribers can binge-watch entire seasons of a show. Netflix, Amazon and studios such as HBO or Showtime are better at creating content with long story arcs over an entire season or seasons compared to traditional cable networks such as CBS, ABC or NBC that specialise in creating shows with self-contained episodes that air in 30-60 minute blocks every night or weekly. Services such as Netflix and perhaps even Disney+ may have an advantage in creating more engaging original content, so much so that Mr Bajarin expects the streaming offerings of the traditional cable networks to fail.

Convenience may also prove to be as important as original content. Before original content became the key differentiator for Netflix, its main competitive advantage was convenience – a one-stop repository for thousands of movies and TV series that could be browsed and consumed on demand, on one platform. In fact, one could argue that Netflix and equivalent streaming services only sell convenience (and trust). That is, all content, including original content, on these services could be streamed or pirated illegally, but most consumers are willing to pay some price for the convenience of having this disparate content aggregated on one secure, trusted platform.

As original and exclusive content continues to fragment across multiple streaming services, convenience is eroded in two ways. Firstly, in the aggregate, which is to say that consumers might now need to subscribe to two, three, four or more streaming services to access all the content they want, each contained within their own separate app or website which limits cross-browsing. Secondly, services such as Netflix lose some of their “one stop convenience” advantage as competing networks and studios pull their licensed content. Would subscribers be willing to pay $20+ per month for Netflix if they can’t access substantial content from other networks, especially if they’re also paying for other streaming subscriptions as well?

This of course creates an opportunity for a player to step in and “rebundle” the streaming market. Amazon has taken steps towards this end, but Apple is perhaps the most viable contender to create a streaming bundle for two reasons. Firstly, Apple has a non-existent content business so won’t be viewed as a competitor by the networks (unlike Amazon with its Prime Video); and secondly, it is well known that Apple users spend much more on content subscriptions and apps than their Android counterparts. If what Mr Bajarin says is correct, then there may soon be a handful of sub-scale standalone streaming services that could be packaged into more compelling streaming bundles.

The expected expansion of supply in direct-to-consumer video streaming services this year is likely to create new winners and losers not only in this segment of the market but may also reshape the wider media industry, if not immediately then certainly over the long term. The catalyst is of course Netflix, which remains a controversial stock and a dangerous short – as demonstrated by the one-month, 50% increase in the share price. Regardless of how we feel about Netflix, we are always on the lookout for opportunities that may emerge from the fallout of disruption. As with Amazon and retail, even if you don’t believe in the story of the disruptor, there may be bountiful opportunity to profit from the disrupted.

![]() Daniel Wu is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Daniel Wu is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.