|

Getting your Trinity Audio player ready...

|

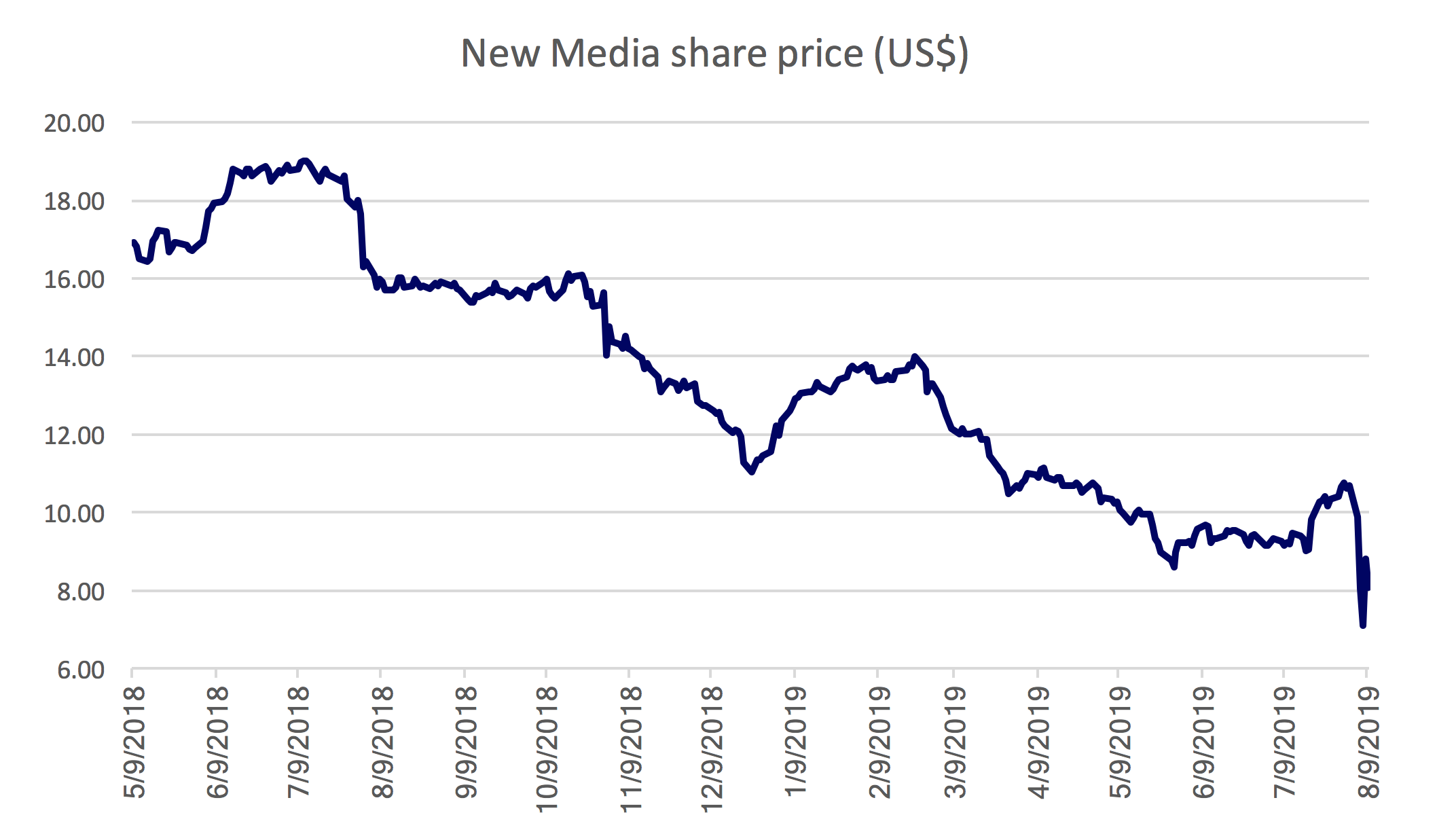

Last Monday, New Media Investment Group, the listed holding company of GateHouse Media, formally announced the previously leaked acquisition of Gannett Co. in a deal that would combine the number one and two publishers of newspapers in the U.S. by circulation volume. In a classic case of buy the rumour, sell the news, positive sentiment around the leak evaporated when the actual details of the deal were announced, causing the New Media share price to crash to all-time lows and erasing one third of the company’s market capitalisation.

The New Media short thesis

Readers of this blog are no doubt aware that newspaper publishing is a dying industry as the internet has created a zero marginal cost playing field for anyone to publish fact and opinions, and smartphones put live news at everyone’s fingertips. Print advertising and circulation revenues have declined as both eyeballs and advertisers have transitioned to online platforms such as Google and Facebook.

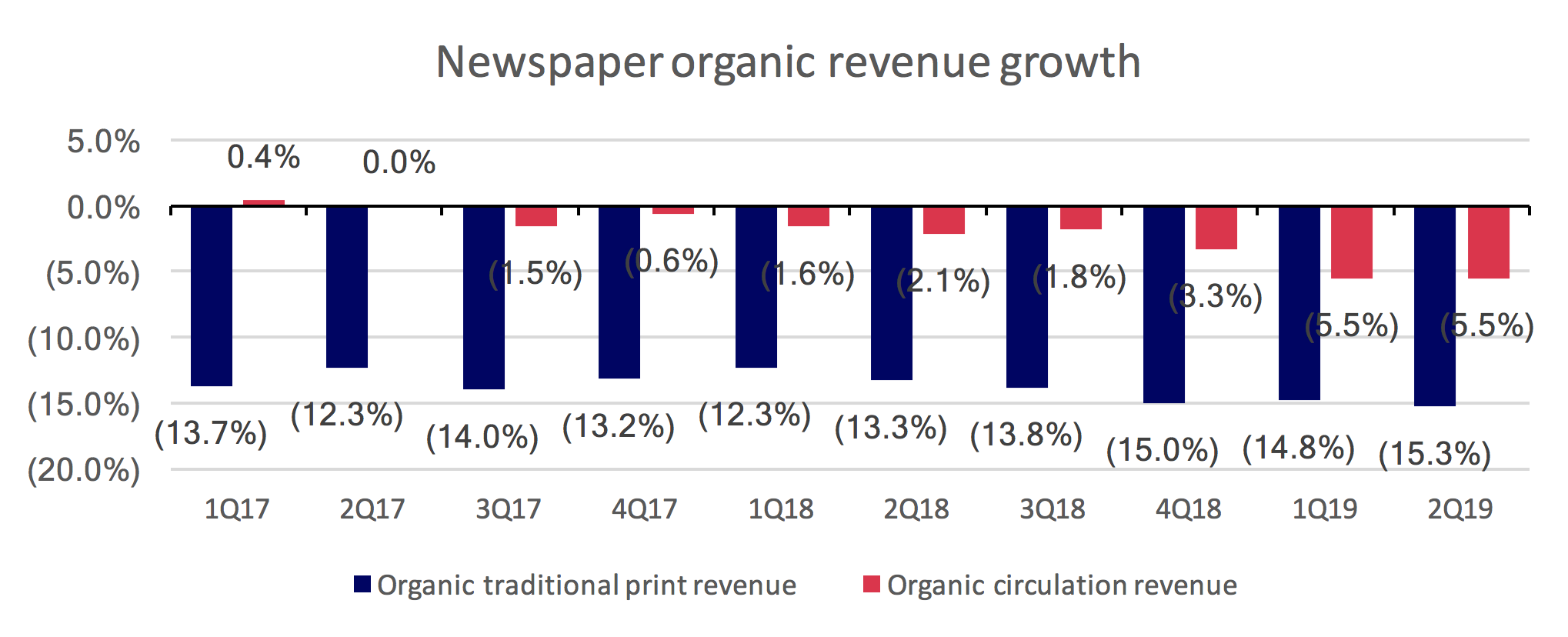

New Media has felt this squeeze acutely, largely due to its huge stable of local and regional publications and lack of a flagship national masthead or compelling digital content. The stock has been a compelling short as the business satisfies all four criteria of the Montaka short framework. In addition to the structural headwinds faced by the wider newspaper industry, New Media’s acquisitive roll-up strategy has masked the organic declines in its print business and created misperceptions that have caused the stock to be overvalued. While the company has consistently reported positive headline growth inflated by acquisitions, organic revenue has been in decline since at least 2013. The organic decline of the print business has in fact accelerated in recent quarters as management implemented a new – and as yet unsuccessful – strategy to push volume over cover price increases.

Source: Company filings, MGI

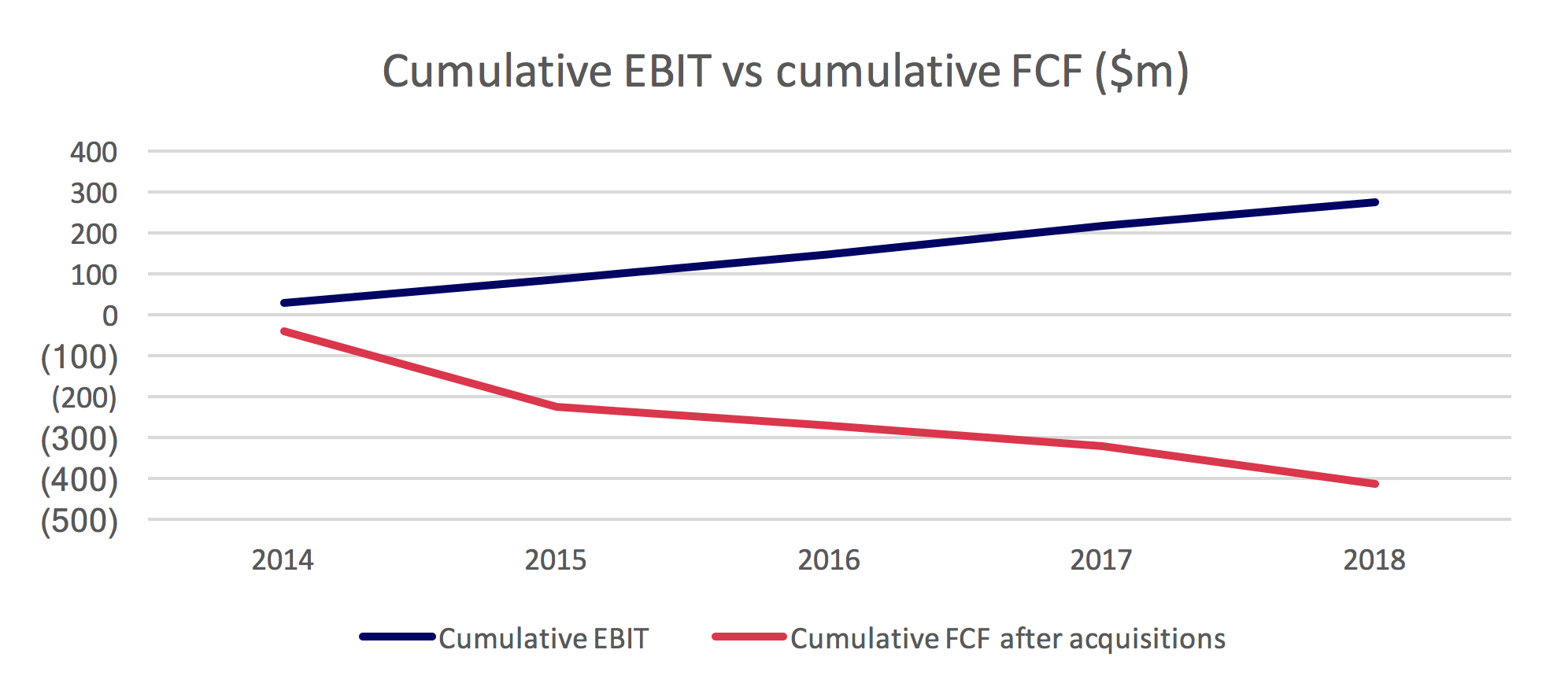

Furthermore, the strategy of rolling up disparate local newspapers, slashing costs and starving them of resources has started to weigh on the balance sheet. By our estimate, net debt to adjusted EBITDA has recently exceeded 3x (though management uses a more generous EBITDA definition), which is high for a structurally declining business and may limit future capacity for debt funded acquisitions. This wouldn’t be such a problem if New Media’s acquisitions were value accretive, but we believe that cumulatively, the acquisitions are in fact value destructive.

The company has spent $1.1 billion on acquisitions since 2013 at an average multiple of 4x LTM EBITDA according to management. We estimate that of the $261 million of cumulative annual EBITDA acquired since 2013, as little as $120 million remains in 2018 (considering total As Adjusted EBITDA is only $182 million), which would imply a medium-term acquisition multiple of 9x. Additionally, nearly half ($515 million) of the acquisition outflow has been funded by newly issued equity capital, likely incentivised by the 1.5% management fee that outsourced manager Fortress Investment Group receives on the book value of equity irrespective of shareholder returns. The widening gap between cumulative EBIT and cumulative free cash flow after acquisitions suggests that none of the company’s earnings are accruing to shareholders.

Source: Company filings, MGI

A deal with Gannett

When news of a potential merger between New Media and Gannett was first leaked in mid-July, sentiment around the deal was generally positive and sent the share prices of both companies spiking. The rationale of the deal was obvious – two struggling, outdated businesses would combine to cut costs and increase scale, which would give them breathing room to invest in a digital future.

Despite the initial optimism, the actual deal announcement was underwhelming. Announced synergies of $275 million to $300 million came in at the high end of the rumoured $200 million to $300 million range, but the debt funding for the deal was higher and more expensive than expected – a new $1.8 billion term loan at a whopping 11.5% interest rate from Apollo Global Management, a private equity firm. The incremental interest on this debt – $140 million – offsets roughly half of the announced synergies and leaves little headroom for the combined company to invest in its digital business, which is a key rationale of the deal in the first place.

At the announced offer price of $12.06, comprised of $6.25 in cash and 0.54 New Media shares per Gannet share, the combined market capitalisation of New Media and Gannett would have closed around $600 million higher than before the deal leak. The after-interest, after-tax NPV of the annual synergies at a generously low 12% cost of equity (considering cost of debt is 11.5%) is $700 million to $800 million assuming zero reinvestment. Throw in even $30 million of annual investment into the digital business and the deal becomes value destructive for New Media shareholders at the announced offer price. Combined with a weak second quarter performance that New Media reported concurrently with the deal announcement, it is no surprise that investors have punished the company’s share price.

Source: Bloomberg, MGI

As for two structurally outdated businesses buying time to undertake a modern transformation, the Sears and Kmart merger in 2005 is an instructive case study on the likelihood of success.

The Montaka funds are short the shares of New Media Investment Group (NYSE: NEWM)

![]() Daniel Wu is a Research Analyst with Montaka Global Investments.

Daniel Wu is a Research Analyst with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.