Through the course of 2018, major central banks, such as the Fed and the ECB, were gently tightening monetary conditions following the strength of the global economy in 2017. Economic growth had improved and inflation expectations had recovered back towards target levels following nearly a decade of monetary stimulus.

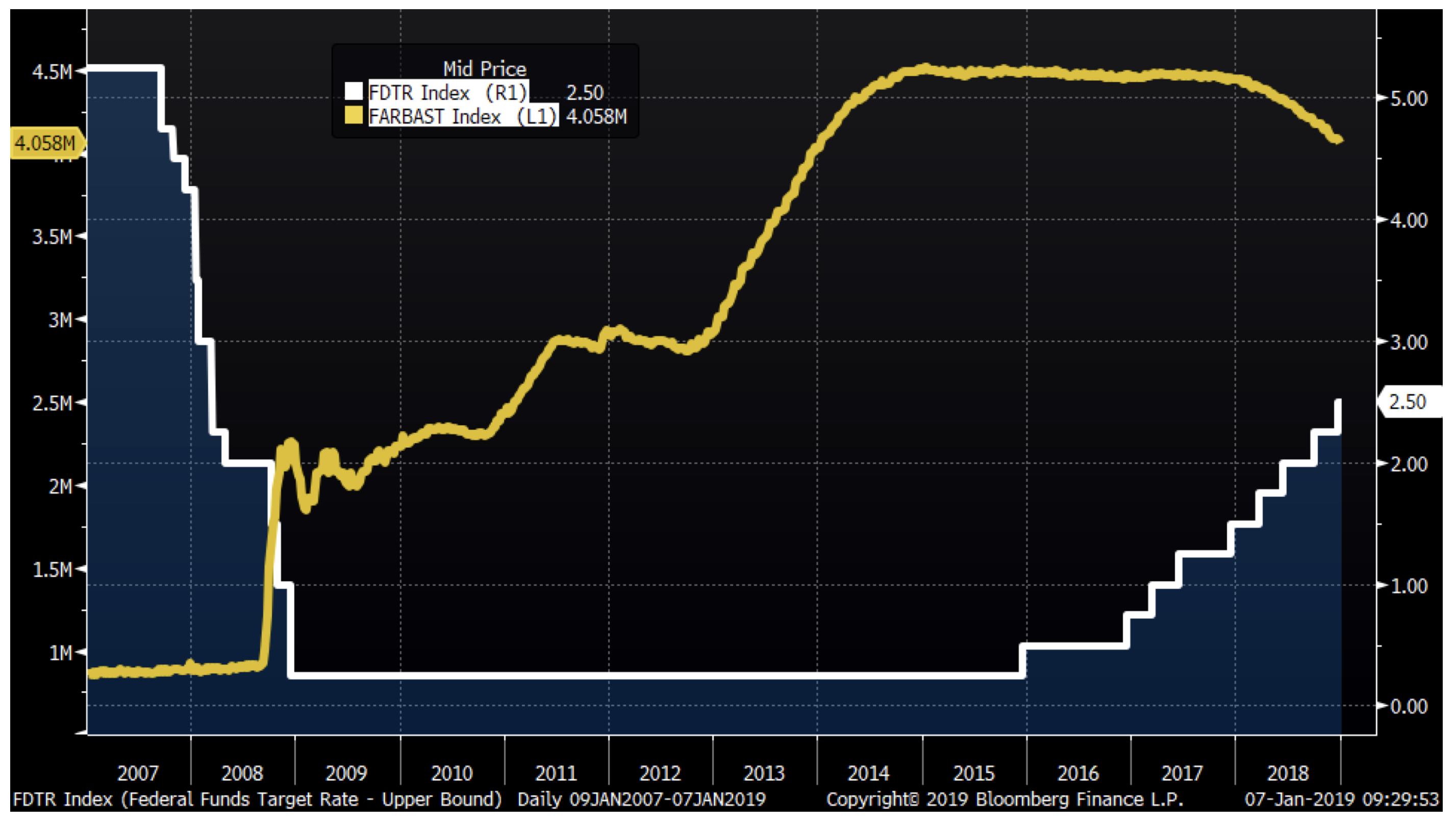

Tightening in the US can be neatly observed by the chart below. In addition to increases in the Federal Funds Target Rate (shown in white), Fed policymakers have also been pursing a gentle unwind of its US$4.5 trillion balance sheet (shown in yellow). As the Fed’s balance sheet shrinks, this removes a significant buyer of US Treasuries and Mortgage-backed securities. This has a monetary “tightening” effect and pushes bond yields higher.

Fed Funds Target Rate (White) vs Federal Reserve Assets (Yellow)

Source: Bloomberg

Meanwhile, in the Eurozone, the ECB started 2018 making monthly net bond asset purchases of €30 billion. By September, this had been reduced to €15 billion; and by the new year just days ago, this form of “quantitative easing” had ended. While the ECB plans to continue reinvesting principal payments of maturing securities for the foreseeable future, the balance sheet has now stopped growing.

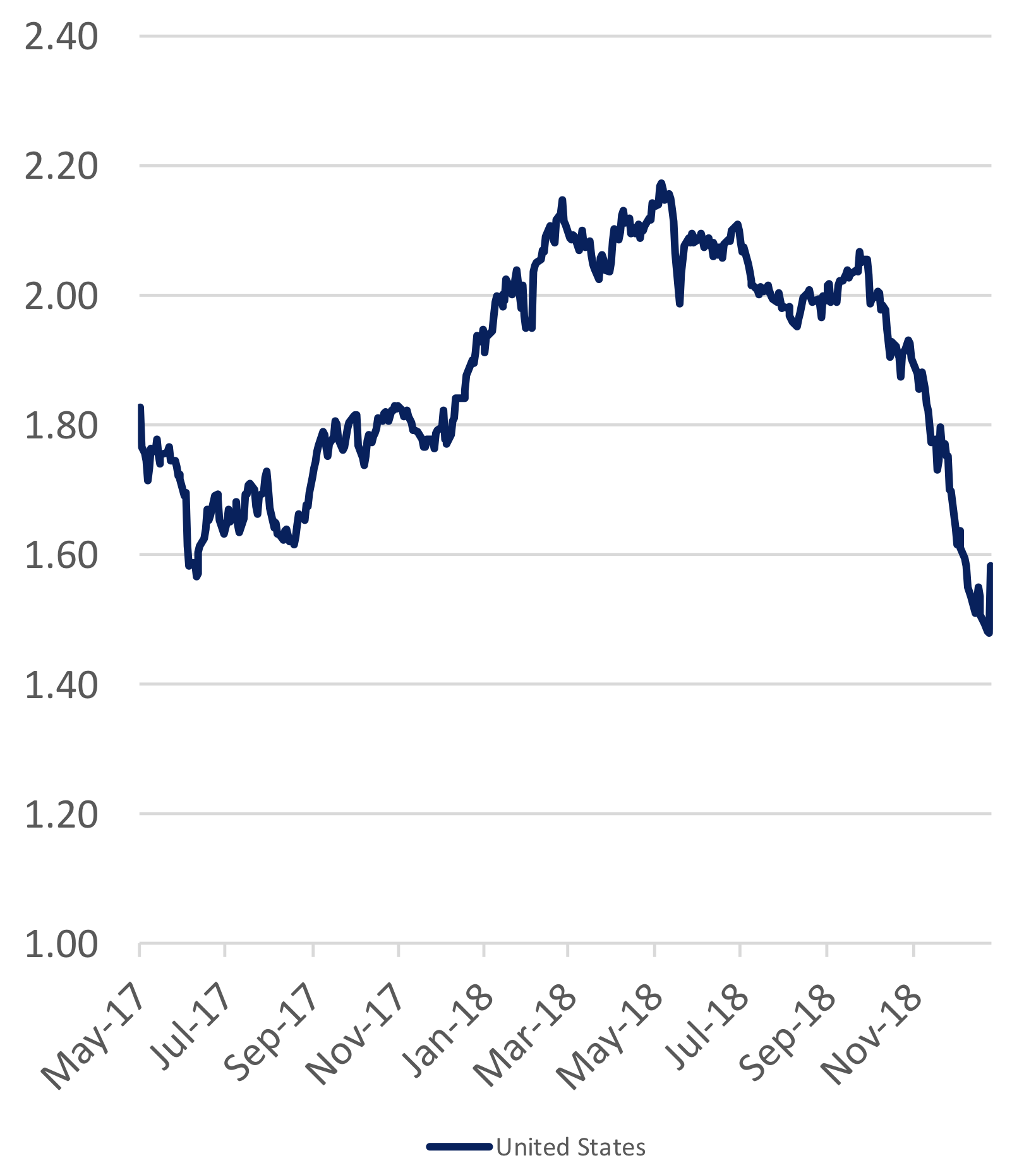

But signals from the bond market in recent weeks suggest inflation expectations have changed. In the US, for example, market-implied inflation expectations have fallen sharply from north of 2.0 percent per annum (the Fed’s target) to less than 1.6 percent per annum.

Bond-market-implied 5YR inflation rate

Source: Bloomberg

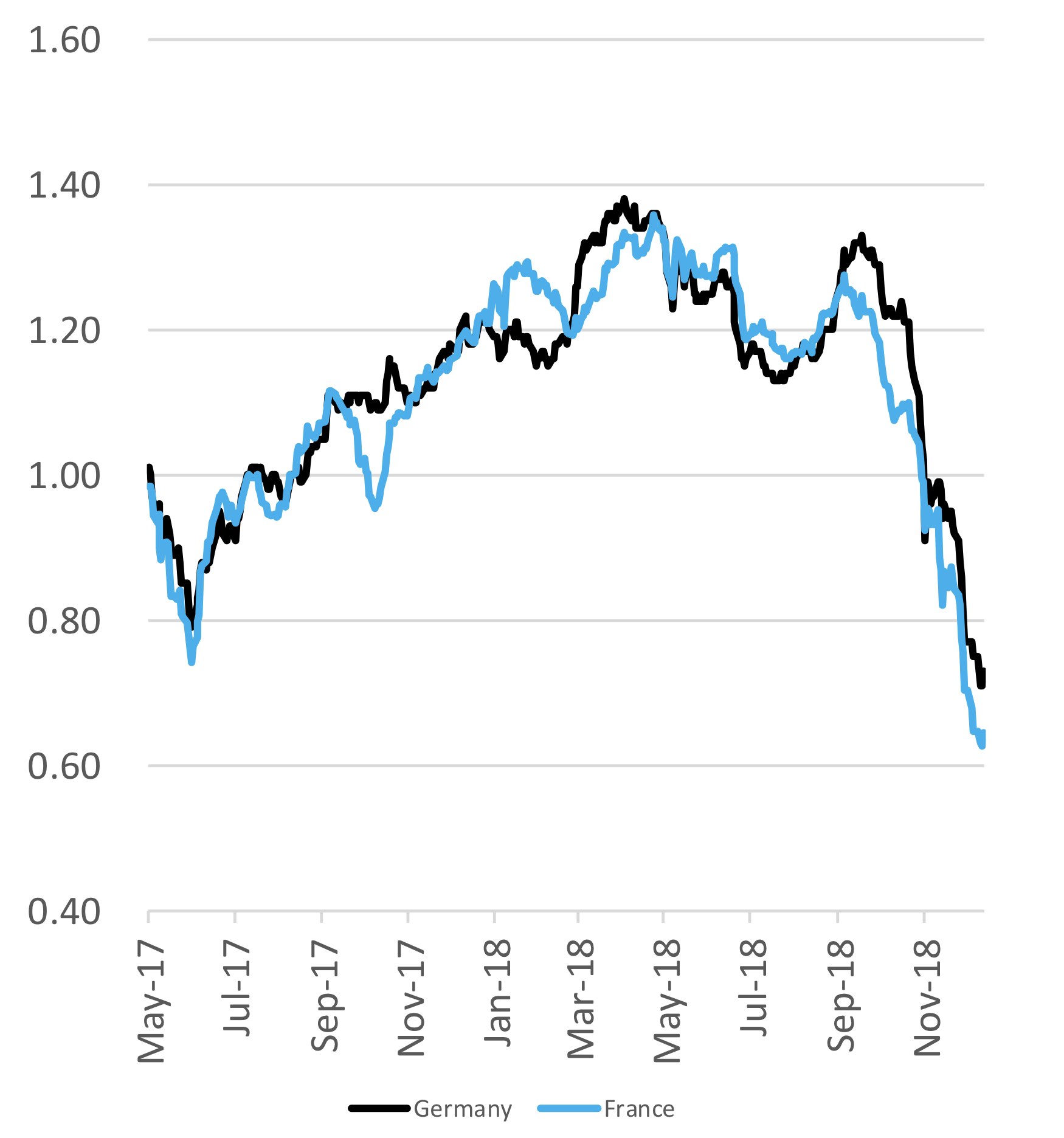

Similarly, market-implied expectations in major Eurozone economies have also fallen. Shown below are the five-year inflation rates for Germany and France that are implied by bond markets. In both countries, inflation expectations have fallen sharply in recent weeks.

Bond-market-implied 5YR inflation rate

Source: Bloomberg

In light of the ongoing US/China trade dispute, the slowing Chinese and European economies and the deflationary impact of the significantly lower oil price, it is difficult to see how policymakers can continue to tighten monetary conditions against this backdrop.

In the US, for example, while the conventional wisdom has been for sustained interest rate hikes throughout 2019, the probability of a Fed cutby year-end recently spiked to nearly 50 percent! At the same time, Fed Chair, Jerome Powell, said: “With the muted inflation readings that we’ve seen coming in, we will be patient as we watch to see how the economy evolves.” He went on to indicate that the Fed was ready to change course “significantly if necessary.”

Bond-market-implied Fed Policy Probabilities

Source: Bloomberg

Meanwhile in the Eurozone, we note that early in 2018, the ECB used to include the following language in their monetary policy press release:

“If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration.”

It would not be surprising to us to see this sentiment be put into effect over the coming weeks and months.

Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Signals from the bond markets

Through the course of 2018, major central banks, such as the Fed and the ECB, were gently tightening monetary conditions following the strength of the global economy in 2017. Economic growth had improved and inflation expectations had recovered back towards target levels following nearly a decade of monetary stimulus.

Tightening in the US can be neatly observed by the chart below. In addition to increases in the Federal Funds Target Rate (shown in white), Fed policymakers have also been pursing a gentle unwind of its US$4.5 trillion balance sheet (shown in yellow). As the Fed’s balance sheet shrinks, this removes a significant buyer of US Treasuries and Mortgage-backed securities. This has a monetary “tightening” effect and pushes bond yields higher.

Fed Funds Target Rate (White) vs Federal Reserve Assets (Yellow)

Source: Bloomberg

Meanwhile, in the Eurozone, the ECB started 2018 making monthly net bond asset purchases of €30 billion. By September, this had been reduced to €15 billion; and by the new year just days ago, this form of “quantitative easing” had ended. While the ECB plans to continue reinvesting principal payments of maturing securities for the foreseeable future, the balance sheet has now stopped growing.

But signals from the bond market in recent weeks suggest inflation expectations have changed. In the US, for example, market-implied inflation expectations have fallen sharply from north of 2.0 percent per annum (the Fed’s target) to less than 1.6 percent per annum.

Bond-market-implied 5YR inflation rate

Source: Bloomberg

Similarly, market-implied expectations in major Eurozone economies have also fallen. Shown below are the five-year inflation rates for Germany and France that are implied by bond markets. In both countries, inflation expectations have fallen sharply in recent weeks.

Bond-market-implied 5YR inflation rate

Source: Bloomberg

In light of the ongoing US/China trade dispute, the slowing Chinese and European economies and the deflationary impact of the significantly lower oil price, it is difficult to see how policymakers can continue to tighten monetary conditions against this backdrop.

In the US, for example, while the conventional wisdom has been for sustained interest rate hikes throughout 2019, the probability of a Fed cutby year-end recently spiked to nearly 50 percent! At the same time, Fed Chair, Jerome Powell, said: “With the muted inflation readings that we’ve seen coming in, we will be patient as we watch to see how the economy evolves.” He went on to indicate that the Fed was ready to change course “significantly if necessary.”

Bond-market-implied Fed Policy Probabilities

Source: Bloomberg

Meanwhile in the Eurozone, we note that early in 2018, the ECB used to include the following language in their monetary policy press release:

“If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration.”

It would not be surprising to us to see this sentiment be put into effect over the coming weeks and months.

Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Signals from the bond markets

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.