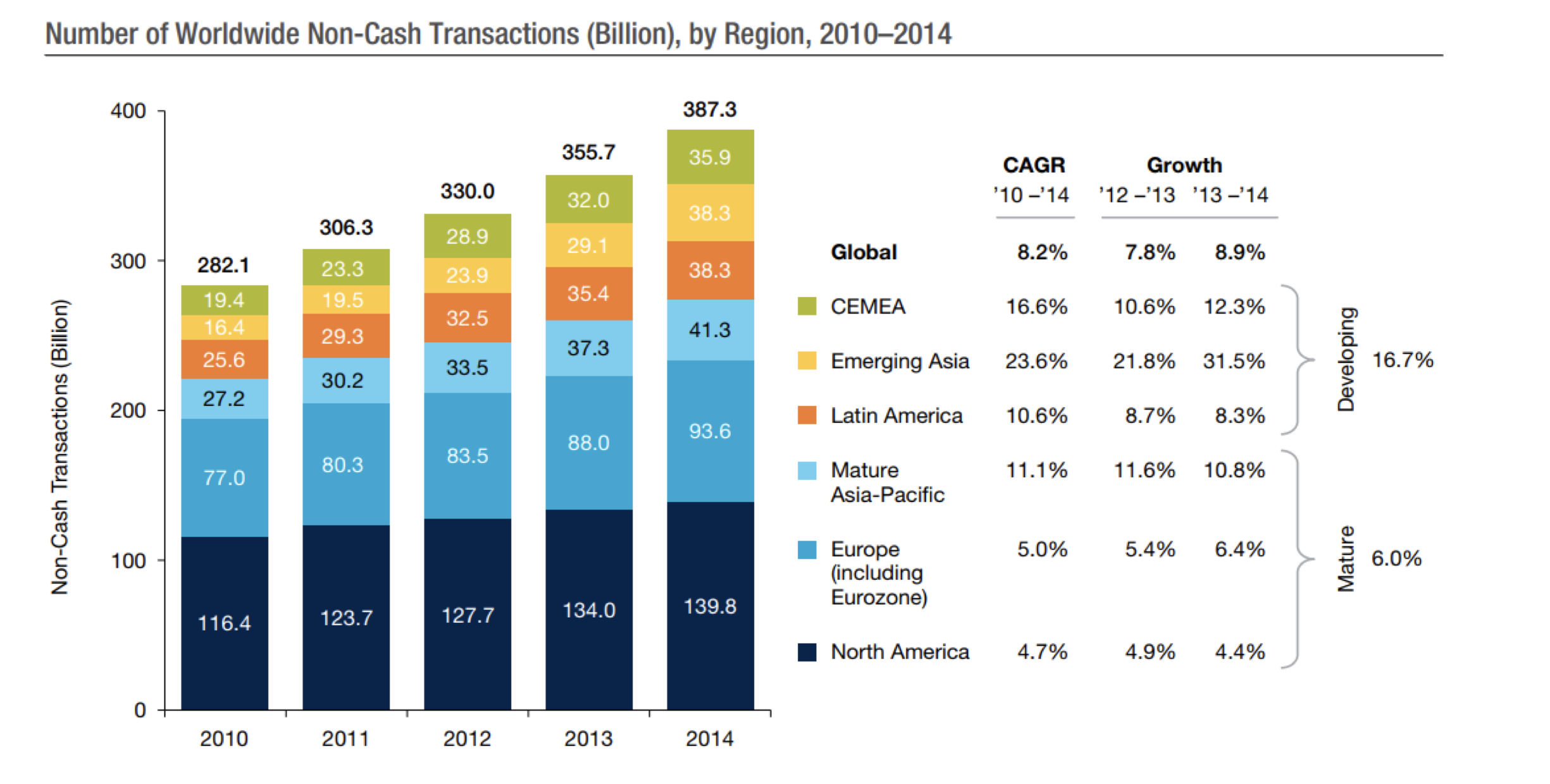

The Montaka team is constantly scouting for longer term technological shifts that may produce opportunities on either the long or short side of the portfolio. One such inexorable trend is the move toward cashless transactions, in place of traditional cash-based payments. Despite being the predominant way of transacting for centuries, cash usage has been in decline, usurped by more convenient electronic payment methods. In the World Payments Report, put together by Capgemini and BNP Paribas, there were $387 billion of global non-cash transaction volumes in 2014, growing at an 8.2 percent annual rate since 2010.

The rising prevalence of mobile and electronic payments has been facilitated by the development of payment systems such as Paypal, Venmo, mPesa, and Apple Pay, amongst many others. These technologies provide a more convenient and efficient means of purchasing goods and services relative to cash.

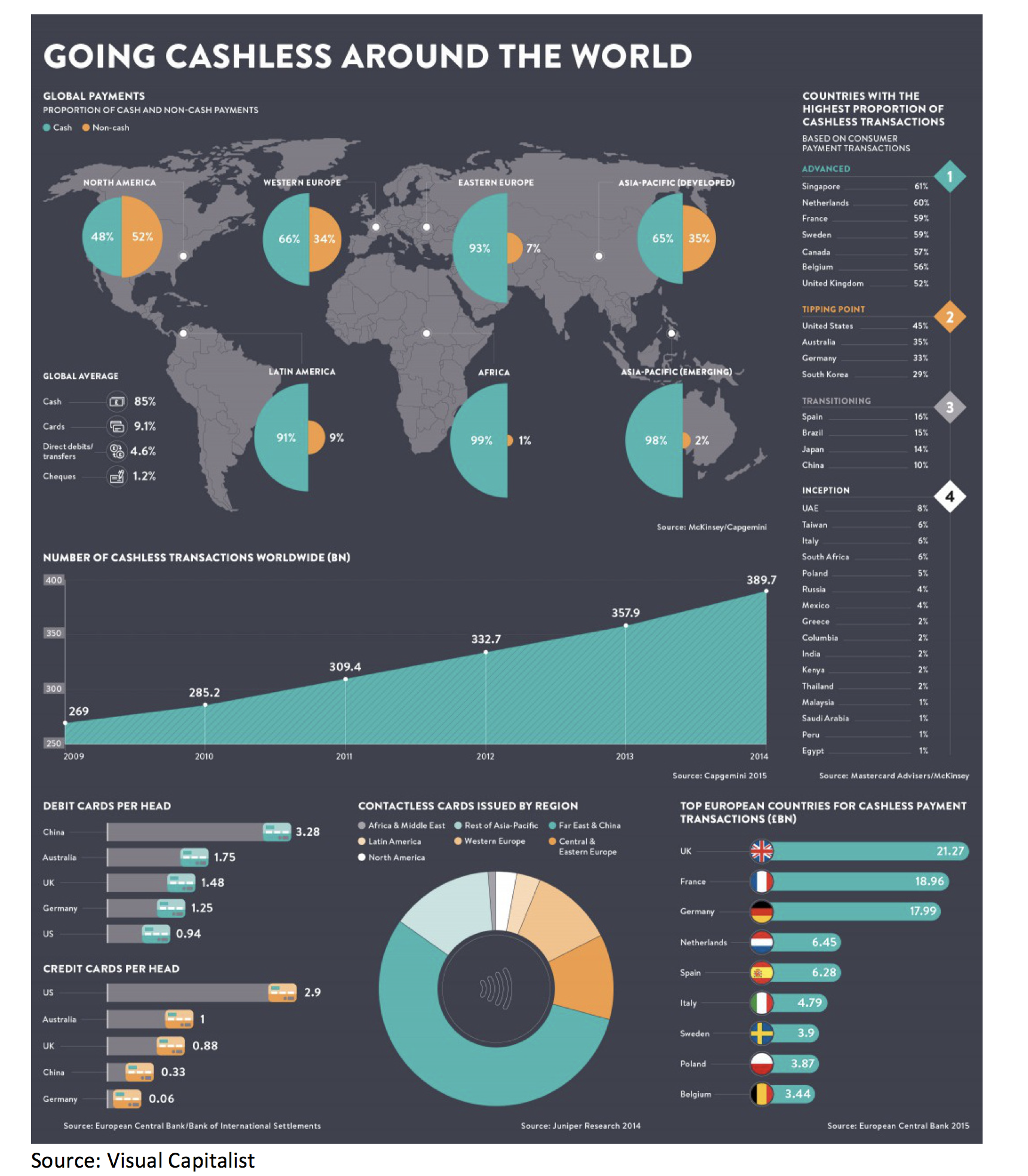

The below infographic highlights the differing stages of cashless penetration amongst global economies.

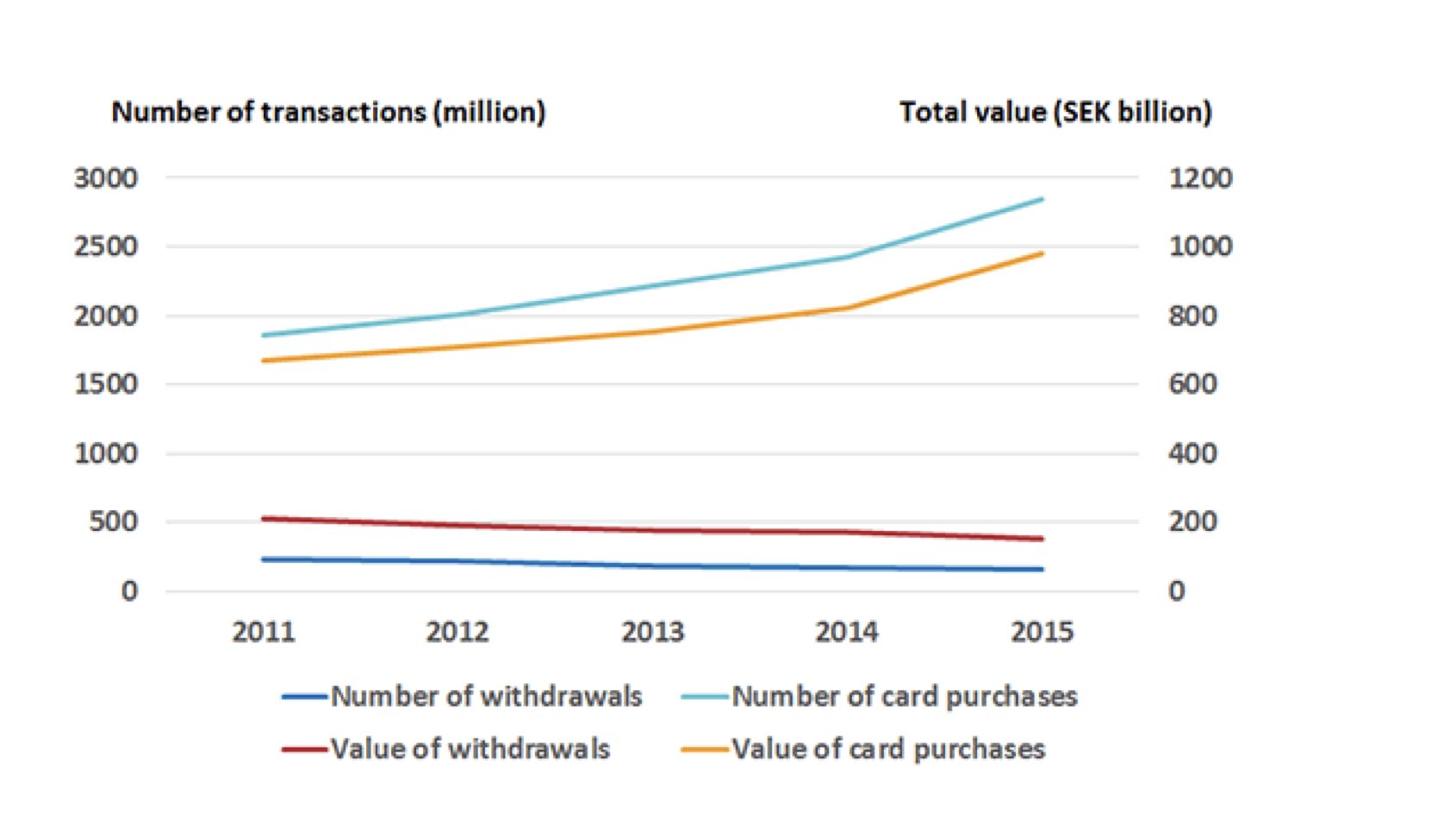

Sweden is a standout example of a country whose citizens have wholeheartedly embraced cashless transactions. According to the Swedish Trade Federation, 80 percent of all transactions are completed by card in Sweden. In a recent three day visit to Stockholm, your author was pleasantly surprised by not having to use cash at any point during his stay. In the graph below, the growth in value of card purchases over the 2011-2015 period has seen a corresponding decline in the value of ATM withdrawals over the same period.

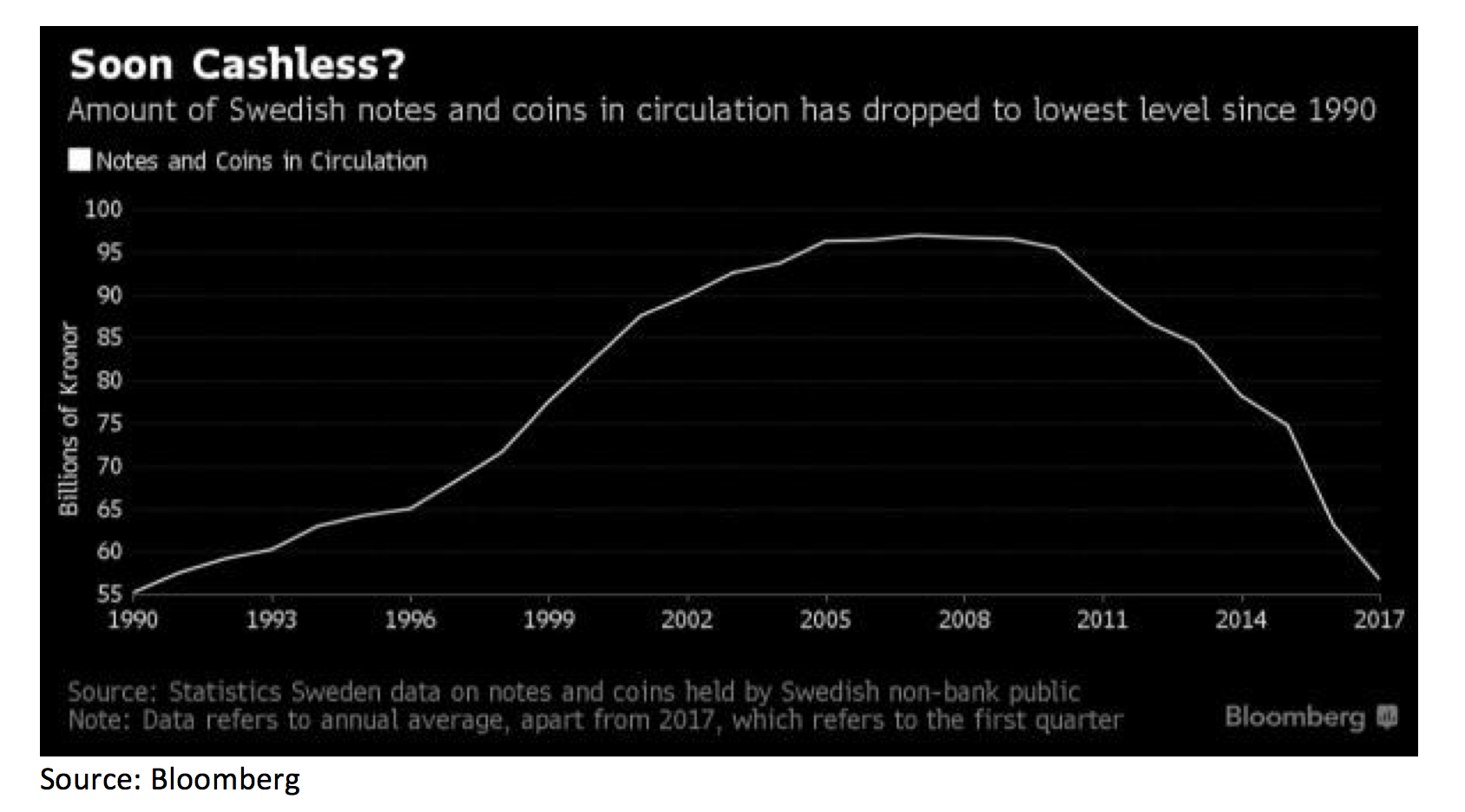

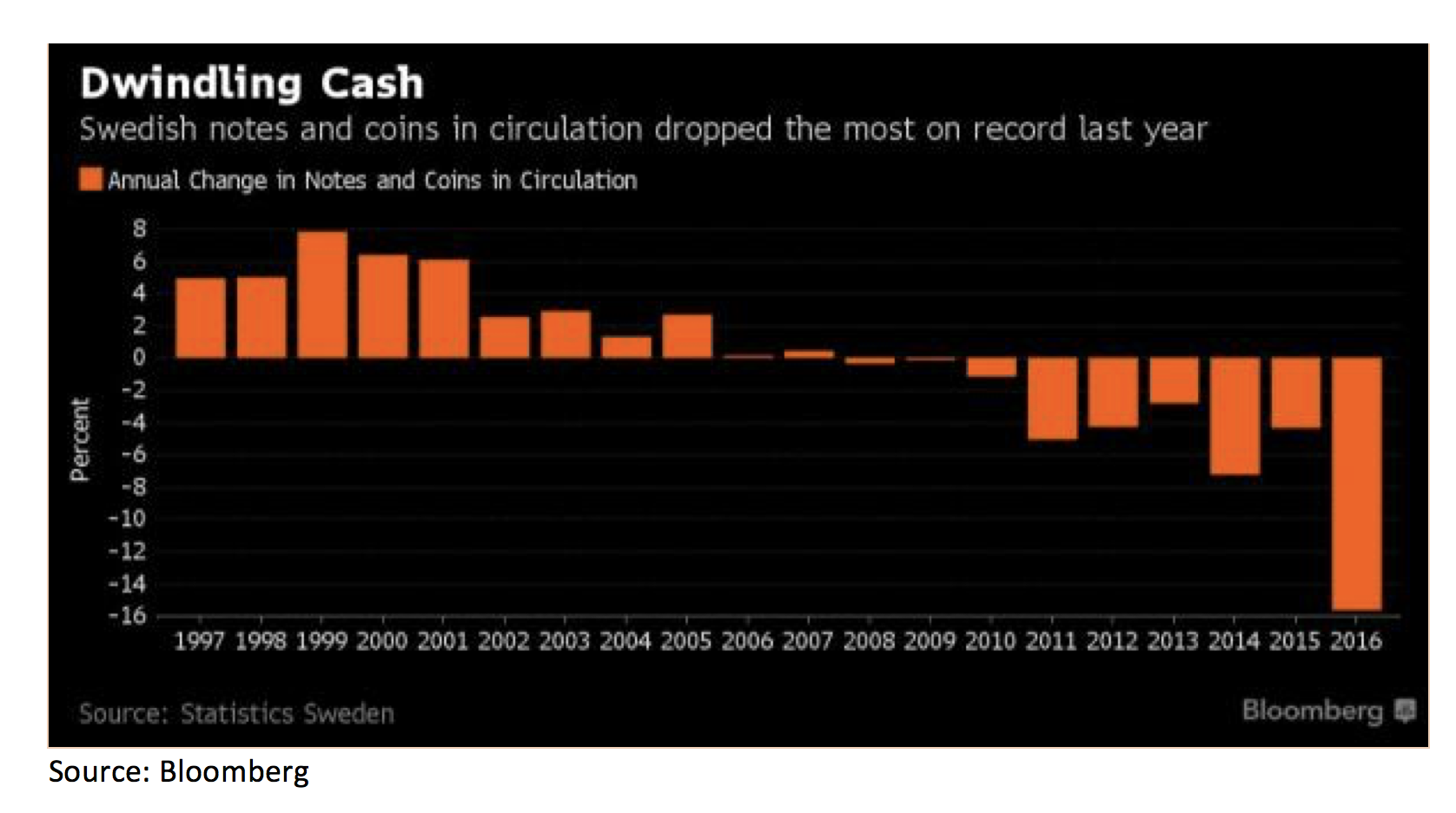

The shunning of cash by Swedes has had implications for the physical currency in circulation in Sweden. As can be seen from the graph below, notes and coins in circulation dropped to an average of just 56.8 billion kronor (around $7 billion), the lowest level since 1990 and more than 40 percent below its 2007 peak.

Notes and coins in circulation dropped by more than 15 percent in 2016, an acceleration from the pace of declines in physical witnessed in prior years.

Interestingly, an increasing number of Swedish churches are now accepting donations via mobile apps. Many of Sweden’s banks have actually stopped handling cash, and even Stockholm’s homeless are accepting credit card payments for their magazine.

The push forward toward a cashless society, however, involves countries grappling with a number of considerations. On the one hand there are numerous benefits of cashless transactions – convenience, traceability of transactions, closing tax loopholes, removing the primary means criminals use to transact on the black market, etc. On the other hand, there are a number of factors that may give us pause, such as privacy concerns with government surveillance of our spending, disruptions if the internet is down, cybertheft and other hacking risks.

It is perhaps due to some of these negative considerations that the migration toward a cashless society has not been uniform or universal, despite the benefits of cashless transactions. While a country like Sweden is very advanced in cashless penetration, India has cash accounting for upward of 95 percent of all transactions.

Countries are shifting toward non-cash payments at different paces. China for example has seen a rapid uptake of cashless transactions, particularly mobile payment transactions. In 2009, over two-thirds of the e-commerce payments in China involved paying cash upon delivery of the goods. Mobile payments now represent 70% of Chinese e-commerce transactions.

In a similar vein, Australians have also been quick to move to cashless transactions. According to the Reserve Bank of Australia (RBA), the number of cash transactions fell by a third between 2007 and 2013. In Australia, cash payments comprised 47 percent of all transactions in 2013, falling from 70 percent in 2007.

What is clear is that there is a global shift toward cashless transactions, and there will certainly be winners and losers. The Montaka team is staying abreast of these trends and constantly looking for opportunities.

George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 8046 5000.

The Decline of Cash

The Montaka team is constantly scouting for longer term technological shifts that may produce opportunities on either the long or short side of the portfolio. One such inexorable trend is the move toward cashless transactions, in place of traditional cash-based payments. Despite being the predominant way of transacting for centuries, cash usage has been in decline, usurped by more convenient electronic payment methods. In the World Payments Report, put together by Capgemini and BNP Paribas, there were $387 billion of global non-cash transaction volumes in 2014, growing at an 8.2 percent annual rate since 2010.

The rising prevalence of mobile and electronic payments has been facilitated by the development of payment systems such as Paypal, Venmo, mPesa, and Apple Pay, amongst many others. These technologies provide a more convenient and efficient means of purchasing goods and services relative to cash.

The below infographic highlights the differing stages of cashless penetration amongst global economies.

Sweden is a standout example of a country whose citizens have wholeheartedly embraced cashless transactions. According to the Swedish Trade Federation, 80 percent of all transactions are completed by card in Sweden. In a recent three day visit to Stockholm, your author was pleasantly surprised by not having to use cash at any point during his stay. In the graph below, the growth in value of card purchases over the 2011-2015 period has seen a corresponding decline in the value of ATM withdrawals over the same period.

The shunning of cash by Swedes has had implications for the physical currency in circulation in Sweden. As can be seen from the graph below, notes and coins in circulation dropped to an average of just 56.8 billion kronor (around $7 billion), the lowest level since 1990 and more than 40 percent below its 2007 peak.

Notes and coins in circulation dropped by more than 15 percent in 2016, an acceleration from the pace of declines in physical witnessed in prior years.

Interestingly, an increasing number of Swedish churches are now accepting donations via mobile apps. Many of Sweden’s banks have actually stopped handling cash, and even Stockholm’s homeless are accepting credit card payments for their magazine.

The push forward toward a cashless society, however, involves countries grappling with a number of considerations. On the one hand there are numerous benefits of cashless transactions – convenience, traceability of transactions, closing tax loopholes, removing the primary means criminals use to transact on the black market, etc. On the other hand, there are a number of factors that may give us pause, such as privacy concerns with government surveillance of our spending, disruptions if the internet is down, cybertheft and other hacking risks.

It is perhaps due to some of these negative considerations that the migration toward a cashless society has not been uniform or universal, despite the benefits of cashless transactions. While a country like Sweden is very advanced in cashless penetration, India has cash accounting for upward of 95 percent of all transactions.

Countries are shifting toward non-cash payments at different paces. China for example has seen a rapid uptake of cashless transactions, particularly mobile payment transactions. In 2009, over two-thirds of the e-commerce payments in China involved paying cash upon delivery of the goods. Mobile payments now represent 70% of Chinese e-commerce transactions.

In a similar vein, Australians have also been quick to move to cashless transactions. According to the Reserve Bank of Australia (RBA), the number of cash transactions fell by a third between 2007 and 2013. In Australia, cash payments comprised 47 percent of all transactions in 2013, falling from 70 percent in 2007.

What is clear is that there is a global shift toward cashless transactions, and there will certainly be winners and losers. The Montaka team is staying abreast of these trends and constantly looking for opportunities.

George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 8046 5000.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.