|

Getting your Trinity Audio player ready...

|

The 2018 Black Friday shopping weekend is all but over and initial reports from retailers, Wall St analysts and third-party analytics providers suggest a robust start to the holiday season. Unsurprisingly, online sales continued to take share, with Adobe Systems estimating a 26% year-over-year increase in online sales through Black Friday, and various estimates of brick-and-mortar foot traffic declining between -1% and -9% over 2017. While strong online sales continue to drive healthy comp sales, investors need to consider whether the tail end of 2018 and 2019 will mark a continuation of the profitless growth that retailers experienced in the first half of 2018.

The first half of 2018 can be characterised by accelerating top-line comp growth offset by flat to declining EBIT dollars and declining EBIT margins. Despite the robust mid-single-digit comp growth reported by several large brick-and-mortar retailers, operating leverage was nowhere to be seen. This was largely due to gross margin pressure driven by planned price investments, higher freight and transportation costs, hourly wage increases and of course the dilutive impact of lower-margin e-commerce growth, partially offset by good SG&A cost control. Investors were happy to reward retailers that reported strong sales growth and look past the margin pressure on the belief that sales growth would continue and margins would inflect.

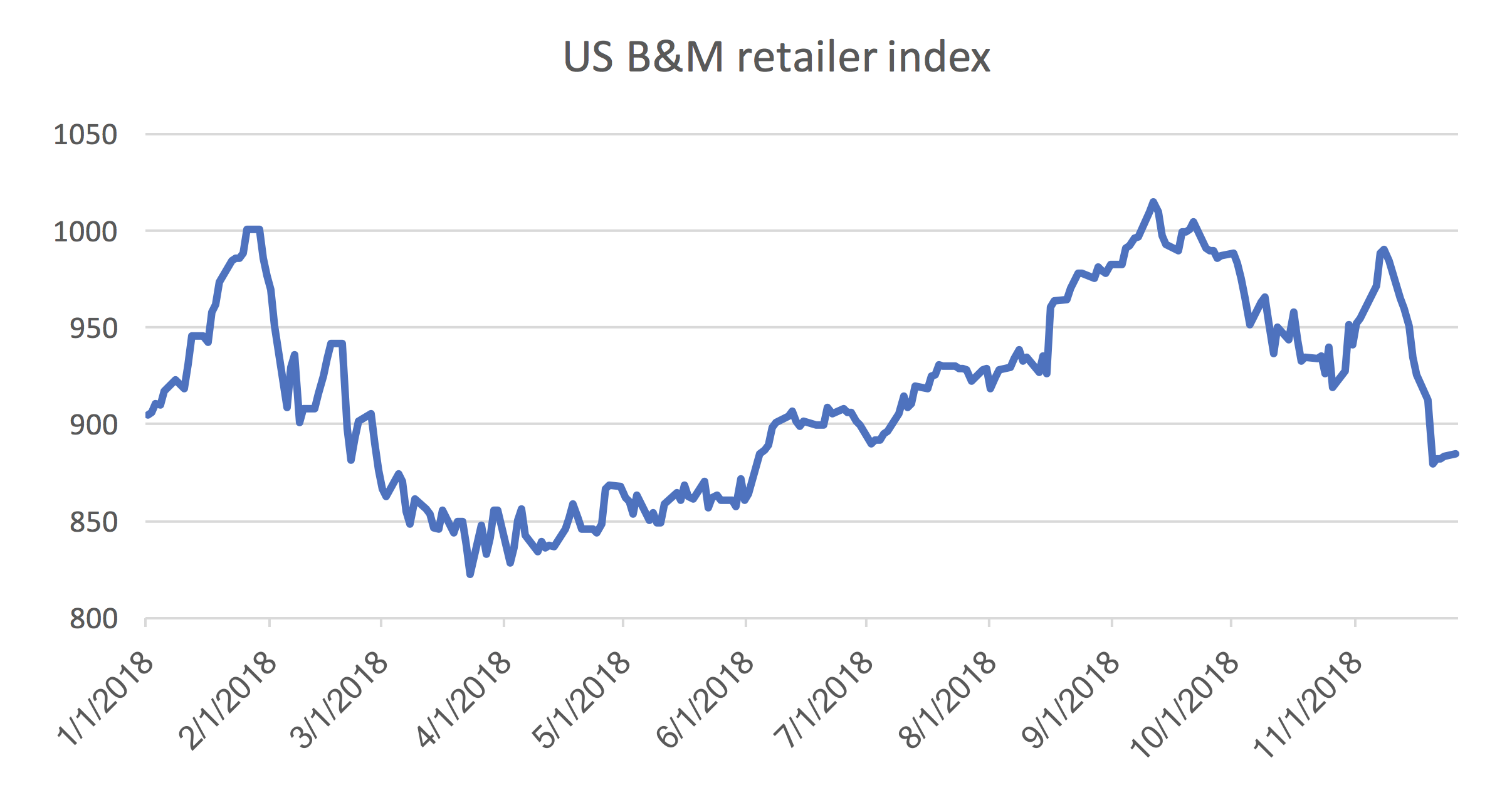

Chart 1: Custom market cap weighted index of 11 large US brick-and-mortar retailers and department stores

However, as can be seen in the chart above, 3Q18 results in November have largely dispelled any hope of a near-term margin inflection, as continued robust (but decelerating) comp growth failed yet again to generate operating leverage. And with Q4 typically being the most promotional quarter of the retail calendar, it seems unlikely that the strong start to the holiday shopping season, especially in the margin-dilutive online channel, will lead to an inflection in operating margins.

Furthermore, we believe that the following factors that have negatively impacted retailer margins are largely structural in nature and expect them to persist into 2019 and beyond.

- The shift to omni-channel. E-commerce is perhaps the largest structural shift to ever hit retailers, and its rapid adoption by US consumers is unlikely to abate any time soon. It is no secret that online sales (click & collect and delivery) carry lower margins than in-store sales due to additional fulfillment and/or delivery costs, while the expectation of fast and free shipping means retailers will recover less and less of these costs directly from customers. Overall e-commerce penetration of retail sales is 10% in the US compared to 17% in China. For online grocery, US penetration is even lower at less than 2% compared to 8% in the UK and 20% in South Korea. Typically considered the most difficult e-commerce category to operate, grocery is shaping up to be the next big online battleground, not least due to Amazon’s 2017 acquisition of Whole Foods Market and consumer demand for omni-channel shopping.

- Rising freight costs, largely due to a structural shortage of US truck drivers exacerbated by a strong US economy, are likely to persist. While freight rates might not continue to rip higher at the double-digit growth seen throughout 2018, structurally elevated rates will continue to depress retailer margins.

- Rising wages. Numerous large retailers have recently announced or implemented wage increases for their lowest-paid store associates to as high as $15/hr in some instances. In a tight labour market, retailers have been forced to raise wages to reduce employee turnover. While this can be mitigated by higher employee productivity, rising wages will nonetheless be a contributor to margin pressure over the next several years.

- Price investments by US grocers are likely to continue, as the US grocery industry remains highly competitive. Walmart has staunchly committed to price leadership and recently returned to its Everyday Low Price (EDLP) roots, while other retailers have either committed to EDLP as well, or to maintain their price gaps with Walmart.

- It should be noted that the margin compression experienced throughout the year were largely before the imposition of tariffs. The tariff impact, should there be no quick deal between the US and China, will likely be far more pronounced in 2019, especially as the 10% tariffs on $250 billion of Chinese imports are set to rise to 25% in January. President Trump has also threatened to impose tariffs on the entire $500 billion spectrum of imports from China.

- Finally, retailers will face tougher comps as they lap the strong sales performance of 2018 YTD, with 2Q19 being a particularly tough quarter. The retailers we follow largely failed to generate operating leverage on strong mid-single-digit comp sales, so we believe it may be difficult for them to prevent further margin contraction should 2019 comp sales stall.

![]() Daniel Wu is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Daniel Wu is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.