In football, a successful player does not run to where the ball was, or where it is right now. They run to where the ball is going to be. The same idea is followed by successful investors. They are typically less interested in the successful businesses of yesteryear, or even today’s success stories. For successful investors, searching for the truly great businesses of the future will always remain the primary concern.

In 1957, the S&P 500 – an index of the largest 500 US-listed companies – was created. At the time, American Telephone and Telegraph (now known as AT&T) was the heaviest-weighted stock in the index. Today, AT&T (NYSE: T) still scrapes into the top 10. But today’s top 10 are dominated by new businesses, many of which did not even exist back in the 1950s, including: Apple (NASDAQ: AAPL), established in 1977; Amazon (NASDAQ: AMZN), established in 1997; and Facebook (NASDAQ): FB), established in 2004.

A New Business Model

The emergence of such dominating new businesses as Apple, Amazon and Facebook stems from the emergence of a new business model: the Online Technology Platform (OTP). The “platform” model has long been one of the truly great business models. But by implementing this model in software – which results in an effective zero cost of marginal production; and online – which results in a near-zero cost of global distribution: owners of successful OTPs often generate enormous economic profits stemming from a number of advantages which are both powerful and sustainable.

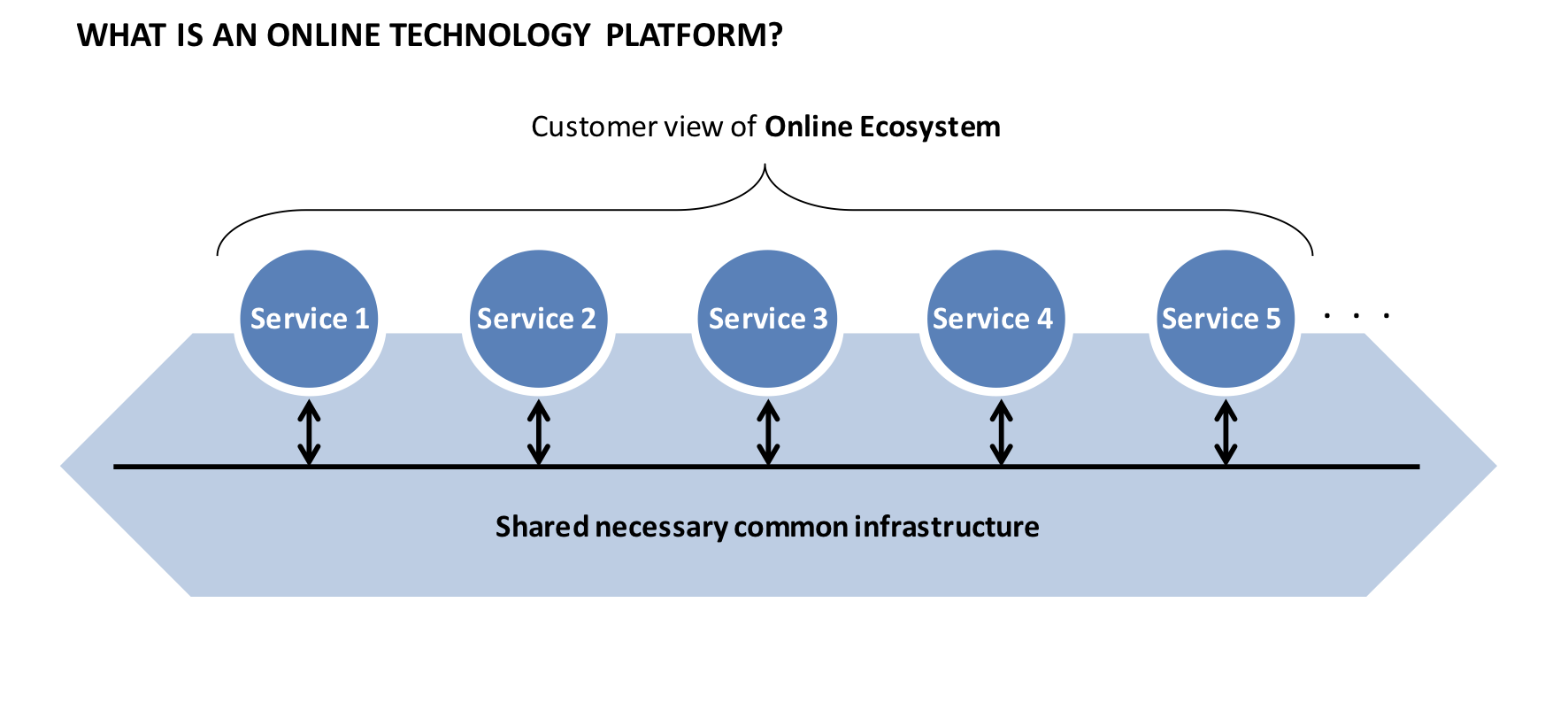

First, it is worth taking a moment to define what exactly we mean by an Online Technology Platform. We define an OTP as the necessary common infrastructure upon which an Online Ecosystem sits. In turn, we define an Online Ecosystem as a collection of online businesses, products, services and/or applications that can be utilized by users, customers, vendors and partners. The Online Ecosystem can scale quickly – and can easily incorporate new additional features, users, customers, vendors and partners. Most Online Ecosystems typically embrace third-party collaboration seeking symbiotic and mutually beneficial relationships. We believe there are four major sources of advantage for owners of OTPs.

We believe there are four major sources of advantage for owners of OTPs.

- Scale – Research & development, sales & marketing and capital investments can be spread across a larger base of revenues stemming from the cumulative sales of the entire ecosystem. Furthermore, the platform’s bargaining power over vendors will be larger than that of any single individual business from within the ecosystem.

- Data – The owner of the platform has sole access to the data generated by all of the users, applications and/or services within the ecosystem. Such data is critical for designing intelligent and highly-valuable algorithms to enhance marketing, advertising and customer utility.

- Network Effects – As more businesses, applications and/or services are added to the platform, more users and customers are attracted to the ecosystem – thereby increasing the value of these businesses, application and/or services, as well as the platform itself. Furthermore, the more revenue that is generated by the ecosystem, the greater the investment in the platform by the owner which further enhances the ecosystem incenting new members to join.

- M&A Value Extraction – The benefits of acquired technology can be shared across a larger base of businesses, applications and/or services. Therefore, newly developed value-adding technology is more valuable to platform owners than to any other owner. Platform owners can, in turn, rationally outbid competing suitors for the same target.

With the above structural advantages, owners of OTPs essentially become effective-shareholders in every current and future business contained within the ecosystem.

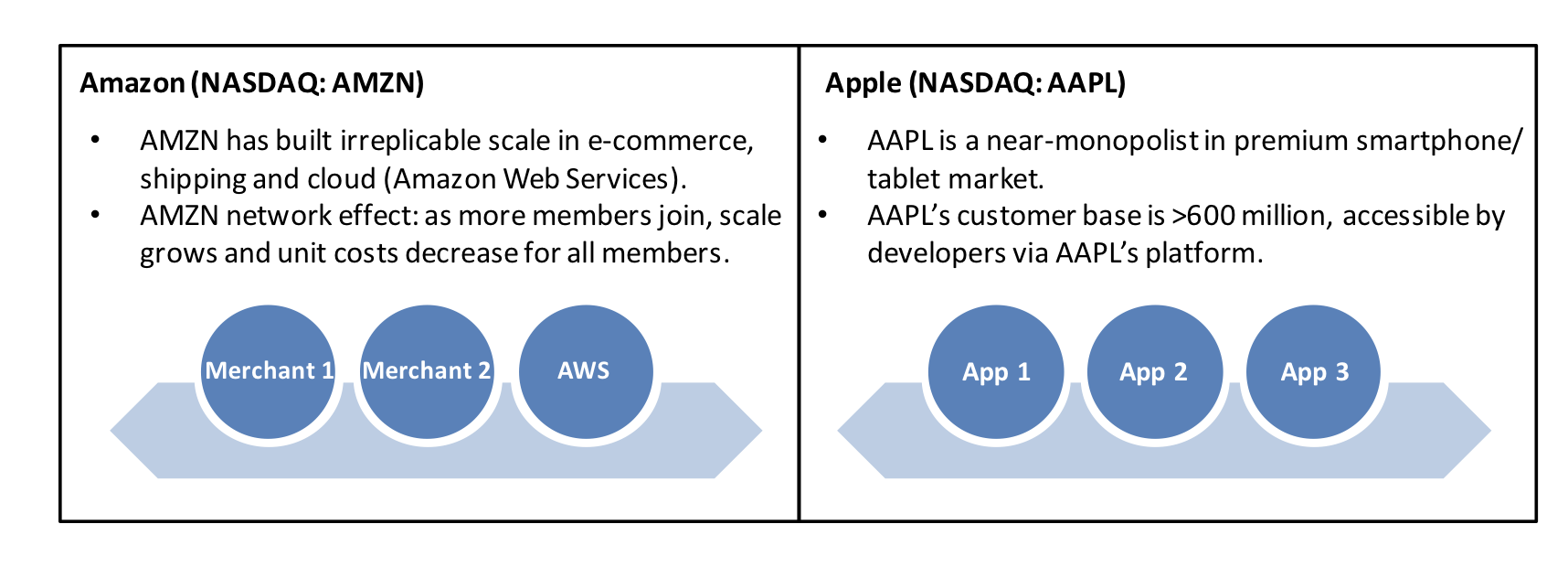

Examples of these dynamics in practice include Amazon and Apple. Amazon is a US$430 billion technology platform that has reduced costs for all of its members through its increased scale. This, in turn, has encouraged new members to join – and so the “flywheel” continues. Furthermore, Amazon uses data intelligently to offer each member customised experiences. For example, it knows your shopping history so can serve you relevant new offerings and product advertising.

Similarly, Apple, a US$750 billion platform, has created an enormous Online Ecosystem with its customer base of more than 600 million global users. With more than two million apps available in its app store, not to mention other available services (including music, video and payments), the incentive for customers to join and remain in the ecosystem are strong. And with so many highly-profitable customers in the network, most third-party app developers will always prioritize Apple’s ecosystem for new product development.

A New Geography

A New Geography

Most global investors are lured first to the United States in search of opportunity. This is not illogical given it is the largest economy in the world; with around 320 million relatively wealthy citizens driving significant annual consumption; and the political institutions are stable (or at least they have been historically).

But in many ways, the US is what is and what has been. But is it what is going to be? Consider this: China already has over three times the online population of the United States. Indeed, in the year of 2016 alone, China added 43 million internet users – equivalent to the population of Argentina, or nearly double the population of Australia. And while the US has the highest GDP per capita at over US$50,000, China’s GDP per capita of $13,000 is enough to be meaningful and is growing far more rapidly.

A mistake that many Western investors make is to assume that the evolution of a developing nation will echo the evolution that has already taken place in more advanced developed nations. But in the same way that younger children avoid the mistakes of their elder siblings, developing nations too often develop in more efficient ways.

Film-producer Kodak, for example, used to tout the emergence of developing economies as reasons for optimism over its business prospects. But unlike those in developed economies, consumers in developing countries never bothered with film cameras. They instead went straight to digital cameras, adopting these natively.

And the same is true with mobile and e-commerce today. Did you know that the largest e-commerce market in the world is not in the US? It is in China and it is already double the size of US e-commerce and growing at a significantly faster pace. And China’s adoption of mobile e-commerce far outweighs that observed in the US, by a factor of about five times! The Chinese have not evolved like the Americans. They have simply skipped over older technologies and instead adopted the most advanced technologies immediately.

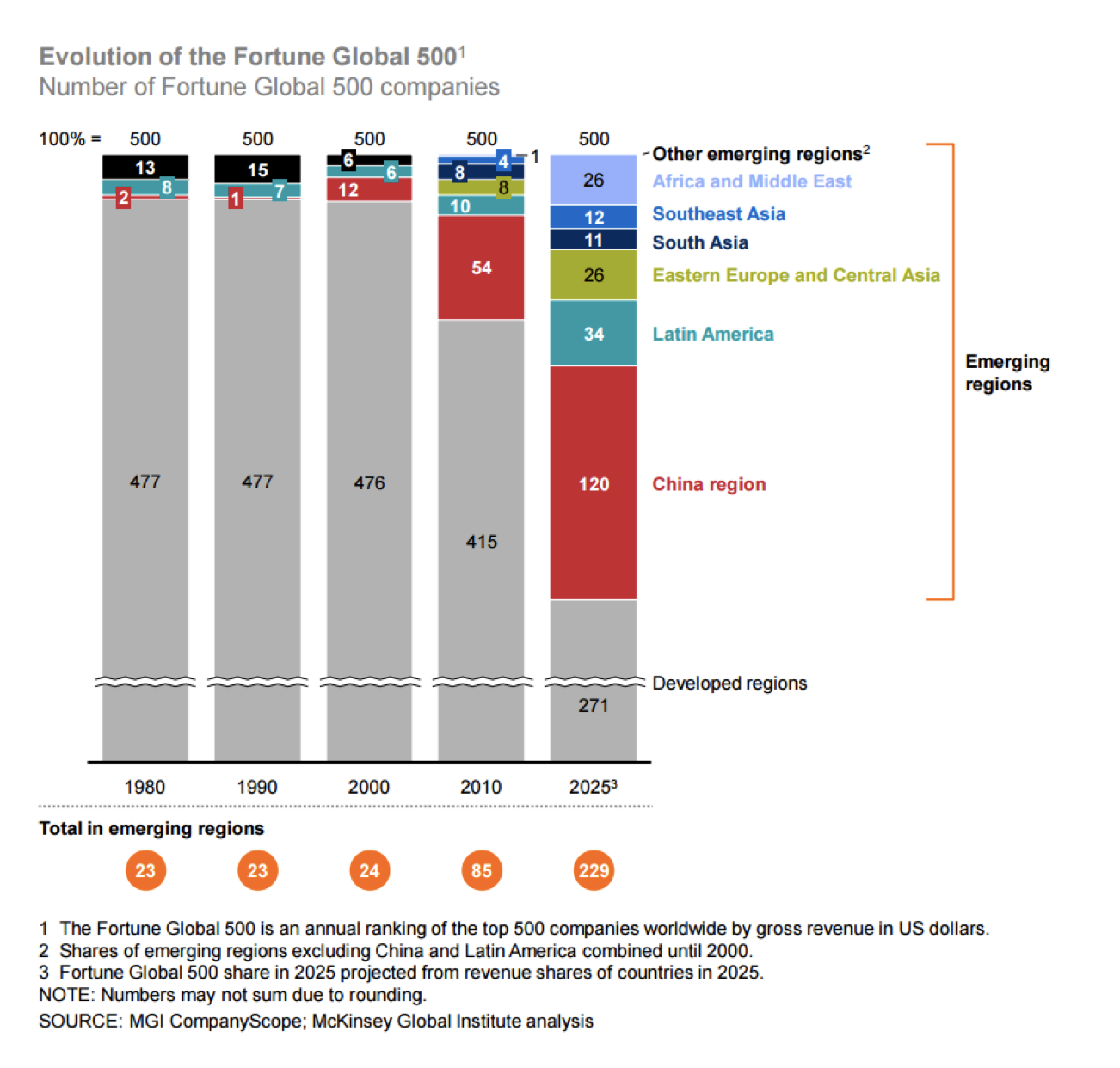

Against this backdrop, one should not be surprised to learn that more of tomorrow’s great businesses will be located in China; and far fewer in developed regions. McKinsey Global Institute compiled the following forecast in recent years. By 2025, emerging regions are expected to be home to almost 230 companies in the Fortune Global 500, up from just 85 in 2010.

Tomorrow’s Great Businesses

Putting the two together, we believe that tomorrow’s great businesses will include Online Technology Platforms, domiciled in China. It is a powerful combination of one of the greatest business models the world has ever seen with a highly-evolved and rapidly-growing online mobile consumer base. Businesses like Alibaba (NYSE: BABA) and Tencent (HKEx: 700) are emerging as likely candidates for tomorrow’s great global businesses.

Take Alibaba, for example, the world’s largest e-commerce platform upon which more than half a trillion US dollars worth of merchandise is transacted each year; and more than three-quarters of which is effected via a mobile device. Alibaba exemplifies the concept of an ecosystem network effect: the more merchants that join the Alibaba e-commerce platform, the more attractive it becomes to consumers; which in turn drives more merchants.

What is particularly interesting about Alibaba, however, is that today, more than half of its revenue comes from a completely new business: online marketing services. With more than 500 million highly-engaged monthly active users and complete access to all user and merchant data, Alibaba can create highly-effective marketing algorithms to target consumers based on highly-specific criteria. This, in turn, significantly increases the “return on investment” of marketing spend via Alibaba’s online channel. As a result, Alibaba now attracts the lion’s share of Chinese mobile advertising spend – to the tune of around 30 percent national market share.

Or take Tencent, for example, owner of WeChat, China’s most popular messaging app. Internet users in China spend nearly two hours per day, on average, on Tencent’s mobile properties – most of which relates to WeChat. With nearly 900 million monthly-active-users, Tencent has been effective at creating an entire online ecosystem within its messaging app.

Tencent’s “app-within-an-app” model creates significant network effects: app developers want their apps to be on WeChat to access the enormous customer base; while at the same time, consumers are attracted to Tencent’s ecosystem to interact with other users, as well as access the millions of apps that exist within the WeChat app.

Like Alibaba, Tencent has also created a new mobile advertising business in recent years. Owning the most popular mobile properties in China makes Tencent the natural future leader of Chinese mobile advertising. While still very much in its infancy (less than 19 percent of total revenues), Tencent’s online advertising business is growing by more than 50 percent per annum. To be clear, this side-business of Tencent’s will be the future Facebook of China. And believe it or not, Facebook is doing all it can to become more “Tencent-like” in the way Tencent has successfully monetised its mobile properties. That’s quite the compliment.

It is clear that Alibaba and Tencent are becoming the duopolists of Chinese mobile internet traffic. And this means that they stand to dominate many industries as they move online: payments, video, gaming and cloud computing to name just a few.

And what’s more, the two businesses also manage what are essentially very active venture capital funds. They own stakes in numerous new up-and-coming businesses such as:

- Ant Financial – the largest third-party payment platform in the world;

- Micromax Mobile – the largest domestic mobile phone maker in India;

- me – a leading food delivery service in China;

- Snapdeal – an Indian online marketplace;

- Didi Kuaidi – the Uber of China;

- com – one of the largest online B2C retailers in China;

- Meilishuo – an online Chinese fashion platform; and

- eLong – a Chinese online travel agent, to name just a few.

The point is this: not only will Alibaba and Tencent be among the great global businesses of tomorrow; but they will also likely participate in the growth of other great businesses of tomorrow.

Investing in Quality

Investing solely in high-quality businesses, such as Alibaba and Tencent, is a choice. Investing in quality (at the right price) is certainly not the only way to preserve and grow wealth but it does offer a level of peace of mind that other strategies perhaps do not.

High-quality businesses exhibit a sustained ability to earn high returns on the capital invested in their business; and often have scope to reinvest a large proportion of their profits back into the business at these high rates of return. For shareholders, this really is a panacea for growing wealth. As capital is reinvested at high rates of returns, business earnings compound and the share price will follow over time.

But this dynamic is a consequence of the quality. How does a business actually build quality in the first place? It creates valuable offerings that are extremely difficult, or impossible, for a competitor to replicate. If you own an asset that I can easily replicate in a day, then that asset is essentially a commodity and it will not generate attractive returns on capital. If, on the other hand, you own an asset that is impossible for anyone to replicate, then you are an effective-monopolist. Monopolies are great for their owners as they allow super-normal value-extraction from their customers who have little alternative but to use them.

In the case of Alibaba and Tencent, these businesses have created two of the largest online technology platforms in China. Alibaba owns the largest e-commerce platform in China (and the world) with more than 500 million monthly active users; while Tencent owns the largest social platform in China with nearly 900 million monthly active users. The network effects these platforms have created have already reinforced themselves so far that it would not be controversial to suggest that these respective assets are, in-effect, impossible for a competitor to replicate. And this means they are among the highest-quality businesses that exist – that also happen to be located in an enormous and rapidly growing geographical market.

But what is particularly interesting about these near-monopolists is that their customers actually love doing business with them. It is not like the monopolist owner of a bridge simply charging an ever-increasing toll for customers to cross it. As their platforms grow, so too does the value of the platform to users, customers, vendors and partners. So while Alibaba and Tencent are near-monopolists, they have been very strategic in ensuring they prioritize customer-value above their own profitability. This has underpinned the strengthening of the platforms which effectively locks in even higher profitability in the future.

Take digital advertising, for example. Both Alibaba and Tencent are leveraging their enormous base of user-data to develop intelligent algorithms that can target users based on highly-specific parameters. For instance, an advertiser could employ these algorithms to target men aged 40-44 years old living in a specific Chinese location who have owned a specific type of car for three years and have recently expressed an interest to his friends or family about looking to upgrade.

With these intelligent algorithms at their disposal, advertisers are flocking to Alibaba’s and Tencent’s digital advertising properties. And what does Alibaba and Tencent charge for this service? Enough to make money but nowhere near what they could charge based on their lead over alternative advertising channels. Instead, by keeping the cost of advertising low relative to its very high efficacy (resulting in a high advertising return-on-investment), the advertising businesses of Alibaba and Tencent are growing at around 50 percent per annum and taking significant market share from their competitors.

Online technology platforms are much closer to “winner takes all” than most other business models. As the winners of tomorrow become clear and their platforms continue to strengthen, these businesses are effectively locking in their ability to generate high returns on invested capital for decades to come. These high-quality businesses will continue to compound their earnings and their share prices will follow.

The Golden Rule

At this point we must remind ourselves of the golden rule of investing: one can never expect to generate outsized returns if one overpays for an asset – no matter the quality of this asset. Said another way: businesses must always be acquired for less than they are worth. There is no amount of “quality” that can offset overpaying for an asset.

There is a logical equivalent to the golden rule which we believe is more meaningful. It begins by viewing each and every stock price in the world as a numerical representation of future market-implied expectations. These expectations relate to the key value drivers of the business: revenue growth, profit margins, capital requirements, and others. As stock prices rise, this is equivalent to the market’s expectations increasing; and vice versa.

Through this lens, the golden rule of investing becomes as follows: stocks must only be acquired when their market-implied expectations are unreasonably conservative. As the saying goes: ‘To outperform the market, you have to be different and you have to be right.’ Well, by understanding how your own expectations differ to those of the market’s, you will at least know where you are different and why you believe you are right.

Investing with Montaka

At Montaka, we believe that the price of a business and the value of a business are two different things. Over the medium term, value acts as a magnet for price; but over the short term, the two can deviate from each other – thereby creating opportunities to buy and sell. This idea is the core premise of value investing.

But we apply our value investing practice only to the universe of high-quality global businesses, including businesses like Alibaba and Tencent. We believe that by owning only high-quality global businesses, our portfolio that we manage on behalf of our investors exhibits a level of “resilience” that other portfolios may lack.

We believe deeply in this idea of resilience which transcends our portfolio of owned businesses. Resilient demand drivers of the businesses we own include: aging populations in many large nations of the world; the structural shift to digital advertising from offline advertising; the emerging Asian middle-class; the structural growth of video-gaming; and the structural shift to online betting from offline betting, to name just a few.

The fundamental value drivers of the businesses we own are resilient. And we believe the value of resilience to investors only increases with uncertainty. And in our new Trump-led Western world, there is certainly no shortage of uncertainty out there. But no matter what the world throws the businesses we own, our investors can rest assured knowing that their underlying demand drivers are solid and will continue to grow structurally.

The net result of our unique approach to investing is as follows. Over the initial years of Montaka’s life, we have delivered our investors two key benefits:

- Returns that place our offering among the highest of our peer group; and

- A return profile – in terms of downside protection and relative correlation – that is unique relative to the market and to our peers. A consequence of these attributes is that our offerings blend unusually well with existing investor portfolios from a risk/reward perspective.

The decision to invest globally is one that all investors will face at some point. At Montaka, we offer a unique and logical approach to investing in high-quality global businesses which has resulted in attractive returns with a highly-complementary risk-profile. And we pride ourselves on delivering these results with a level of transparency for our investors that we believe remains unmatched in the marketplace.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Who are the businesses of the future?

In football, a successful player does not run to where the ball was, or where it is right now. They run to where the ball is going to be. The same idea is followed by successful investors. They are typically less interested in the successful businesses of yesteryear, or even today’s success stories. For successful investors, searching for the truly great businesses of the future will always remain the primary concern.

In 1957, the S&P 500 – an index of the largest 500 US-listed companies – was created. At the time, American Telephone and Telegraph (now known as AT&T) was the heaviest-weighted stock in the index. Today, AT&T (NYSE: T) still scrapes into the top 10. But today’s top 10 are dominated by new businesses, many of which did not even exist back in the 1950s, including: Apple (NASDAQ: AAPL), established in 1977; Amazon (NASDAQ: AMZN), established in 1997; and Facebook (NASDAQ): FB), established in 2004.

A New Business Model

The emergence of such dominating new businesses as Apple, Amazon and Facebook stems from the emergence of a new business model: the Online Technology Platform (OTP). The “platform” model has long been one of the truly great business models. But by implementing this model in software – which results in an effective zero cost of marginal production; and online – which results in a near-zero cost of global distribution: owners of successful OTPs often generate enormous economic profits stemming from a number of advantages which are both powerful and sustainable.

First, it is worth taking a moment to define what exactly we mean by an Online Technology Platform. We define an OTP as the necessary common infrastructure upon which an Online Ecosystem sits. In turn, we define an Online Ecosystem as a collection of online businesses, products, services and/or applications that can be utilized by users, customers, vendors and partners. The Online Ecosystem can scale quickly – and can easily incorporate new additional features, users, customers, vendors and partners. Most Online Ecosystems typically embrace third-party collaboration seeking symbiotic and mutually beneficial relationships. We believe there are four major sources of advantage for owners of OTPs.

We believe there are four major sources of advantage for owners of OTPs.

With the above structural advantages, owners of OTPs essentially become effective-shareholders in every current and future business contained within the ecosystem.

Examples of these dynamics in practice include Amazon and Apple. Amazon is a US$430 billion technology platform that has reduced costs for all of its members through its increased scale. This, in turn, has encouraged new members to join – and so the “flywheel” continues. Furthermore, Amazon uses data intelligently to offer each member customised experiences. For example, it knows your shopping history so can serve you relevant new offerings and product advertising.

Similarly, Apple, a US$750 billion platform, has created an enormous Online Ecosystem with its customer base of more than 600 million global users. With more than two million apps available in its app store, not to mention other available services (including music, video and payments), the incentive for customers to join and remain in the ecosystem are strong. And with so many highly-profitable customers in the network, most third-party app developers will always prioritize Apple’s ecosystem for new product development.

Most global investors are lured first to the United States in search of opportunity. This is not illogical given it is the largest economy in the world; with around 320 million relatively wealthy citizens driving significant annual consumption; and the political institutions are stable (or at least they have been historically).

But in many ways, the US is what is and what has been. But is it what is going to be? Consider this: China already has over three times the online population of the United States. Indeed, in the year of 2016 alone, China added 43 million internet users – equivalent to the population of Argentina, or nearly double the population of Australia. And while the US has the highest GDP per capita at over US$50,000, China’s GDP per capita of $13,000 is enough to be meaningful and is growing far more rapidly.

A mistake that many Western investors make is to assume that the evolution of a developing nation will echo the evolution that has already taken place in more advanced developed nations. But in the same way that younger children avoid the mistakes of their elder siblings, developing nations too often develop in more efficient ways.

Film-producer Kodak, for example, used to tout the emergence of developing economies as reasons for optimism over its business prospects. But unlike those in developed economies, consumers in developing countries never bothered with film cameras. They instead went straight to digital cameras, adopting these natively.

And the same is true with mobile and e-commerce today. Did you know that the largest e-commerce market in the world is not in the US? It is in China and it is already double the size of US e-commerce and growing at a significantly faster pace. And China’s adoption of mobile e-commerce far outweighs that observed in the US, by a factor of about five times! The Chinese have not evolved like the Americans. They have simply skipped over older technologies and instead adopted the most advanced technologies immediately.

Against this backdrop, one should not be surprised to learn that more of tomorrow’s great businesses will be located in China; and far fewer in developed regions. McKinsey Global Institute compiled the following forecast in recent years. By 2025, emerging regions are expected to be home to almost 230 companies in the Fortune Global 500, up from just 85 in 2010.

Tomorrow’s Great Businesses

Putting the two together, we believe that tomorrow’s great businesses will include Online Technology Platforms, domiciled in China. It is a powerful combination of one of the greatest business models the world has ever seen with a highly-evolved and rapidly-growing online mobile consumer base. Businesses like Alibaba (NYSE: BABA) and Tencent (HKEx: 700) are emerging as likely candidates for tomorrow’s great global businesses.

Take Alibaba, for example, the world’s largest e-commerce platform upon which more than half a trillion US dollars worth of merchandise is transacted each year; and more than three-quarters of which is effected via a mobile device. Alibaba exemplifies the concept of an ecosystem network effect: the more merchants that join the Alibaba e-commerce platform, the more attractive it becomes to consumers; which in turn drives more merchants.

What is particularly interesting about Alibaba, however, is that today, more than half of its revenue comes from a completely new business: online marketing services. With more than 500 million highly-engaged monthly active users and complete access to all user and merchant data, Alibaba can create highly-effective marketing algorithms to target consumers based on highly-specific criteria. This, in turn, significantly increases the “return on investment” of marketing spend via Alibaba’s online channel. As a result, Alibaba now attracts the lion’s share of Chinese mobile advertising spend – to the tune of around 30 percent national market share.

Or take Tencent, for example, owner of WeChat, China’s most popular messaging app. Internet users in China spend nearly two hours per day, on average, on Tencent’s mobile properties – most of which relates to WeChat. With nearly 900 million monthly-active-users, Tencent has been effective at creating an entire online ecosystem within its messaging app.

Tencent’s “app-within-an-app” model creates significant network effects: app developers want their apps to be on WeChat to access the enormous customer base; while at the same time, consumers are attracted to Tencent’s ecosystem to interact with other users, as well as access the millions of apps that exist within the WeChat app.

Like Alibaba, Tencent has also created a new mobile advertising business in recent years. Owning the most popular mobile properties in China makes Tencent the natural future leader of Chinese mobile advertising. While still very much in its infancy (less than 19 percent of total revenues), Tencent’s online advertising business is growing by more than 50 percent per annum. To be clear, this side-business of Tencent’s will be the future Facebook of China. And believe it or not, Facebook is doing all it can to become more “Tencent-like” in the way Tencent has successfully monetised its mobile properties. That’s quite the compliment.

It is clear that Alibaba and Tencent are becoming the duopolists of Chinese mobile internet traffic. And this means that they stand to dominate many industries as they move online: payments, video, gaming and cloud computing to name just a few.

And what’s more, the two businesses also manage what are essentially very active venture capital funds. They own stakes in numerous new up-and-coming businesses such as:

The point is this: not only will Alibaba and Tencent be among the great global businesses of tomorrow; but they will also likely participate in the growth of other great businesses of tomorrow.

Investing in Quality

Investing solely in high-quality businesses, such as Alibaba and Tencent, is a choice. Investing in quality (at the right price) is certainly not the only way to preserve and grow wealth but it does offer a level of peace of mind that other strategies perhaps do not.

High-quality businesses exhibit a sustained ability to earn high returns on the capital invested in their business; and often have scope to reinvest a large proportion of their profits back into the business at these high rates of return. For shareholders, this really is a panacea for growing wealth. As capital is reinvested at high rates of returns, business earnings compound and the share price will follow over time.

But this dynamic is a consequence of the quality. How does a business actually build quality in the first place? It creates valuable offerings that are extremely difficult, or impossible, for a competitor to replicate. If you own an asset that I can easily replicate in a day, then that asset is essentially a commodity and it will not generate attractive returns on capital. If, on the other hand, you own an asset that is impossible for anyone to replicate, then you are an effective-monopolist. Monopolies are great for their owners as they allow super-normal value-extraction from their customers who have little alternative but to use them.

In the case of Alibaba and Tencent, these businesses have created two of the largest online technology platforms in China. Alibaba owns the largest e-commerce platform in China (and the world) with more than 500 million monthly active users; while Tencent owns the largest social platform in China with nearly 900 million monthly active users. The network effects these platforms have created have already reinforced themselves so far that it would not be controversial to suggest that these respective assets are, in-effect, impossible for a competitor to replicate. And this means they are among the highest-quality businesses that exist – that also happen to be located in an enormous and rapidly growing geographical market.

But what is particularly interesting about these near-monopolists is that their customers actually love doing business with them. It is not like the monopolist owner of a bridge simply charging an ever-increasing toll for customers to cross it. As their platforms grow, so too does the value of the platform to users, customers, vendors and partners. So while Alibaba and Tencent are near-monopolists, they have been very strategic in ensuring they prioritize customer-value above their own profitability. This has underpinned the strengthening of the platforms which effectively locks in even higher profitability in the future.

Take digital advertising, for example. Both Alibaba and Tencent are leveraging their enormous base of user-data to develop intelligent algorithms that can target users based on highly-specific parameters. For instance, an advertiser could employ these algorithms to target men aged 40-44 years old living in a specific Chinese location who have owned a specific type of car for three years and have recently expressed an interest to his friends or family about looking to upgrade.

With these intelligent algorithms at their disposal, advertisers are flocking to Alibaba’s and Tencent’s digital advertising properties. And what does Alibaba and Tencent charge for this service? Enough to make money but nowhere near what they could charge based on their lead over alternative advertising channels. Instead, by keeping the cost of advertising low relative to its very high efficacy (resulting in a high advertising return-on-investment), the advertising businesses of Alibaba and Tencent are growing at around 50 percent per annum and taking significant market share from their competitors.

Online technology platforms are much closer to “winner takes all” than most other business models. As the winners of tomorrow become clear and their platforms continue to strengthen, these businesses are effectively locking in their ability to generate high returns on invested capital for decades to come. These high-quality businesses will continue to compound their earnings and their share prices will follow.

The Golden Rule

At this point we must remind ourselves of the golden rule of investing: one can never expect to generate outsized returns if one overpays for an asset – no matter the quality of this asset. Said another way: businesses must always be acquired for less than they are worth. There is no amount of “quality” that can offset overpaying for an asset.

There is a logical equivalent to the golden rule which we believe is more meaningful. It begins by viewing each and every stock price in the world as a numerical representation of future market-implied expectations. These expectations relate to the key value drivers of the business: revenue growth, profit margins, capital requirements, and others. As stock prices rise, this is equivalent to the market’s expectations increasing; and vice versa.

Through this lens, the golden rule of investing becomes as follows: stocks must only be acquired when their market-implied expectations are unreasonably conservative. As the saying goes: ‘To outperform the market, you have to be different and you have to be right.’ Well, by understanding how your own expectations differ to those of the market’s, you will at least know where you are different and why you believe you are right.

Investing with Montaka

At Montaka, we believe that the price of a business and the value of a business are two different things. Over the medium term, value acts as a magnet for price; but over the short term, the two can deviate from each other – thereby creating opportunities to buy and sell. This idea is the core premise of value investing.

But we apply our value investing practice only to the universe of high-quality global businesses, including businesses like Alibaba and Tencent. We believe that by owning only high-quality global businesses, our portfolio that we manage on behalf of our investors exhibits a level of “resilience” that other portfolios may lack.

We believe deeply in this idea of resilience which transcends our portfolio of owned businesses. Resilient demand drivers of the businesses we own include: aging populations in many large nations of the world; the structural shift to digital advertising from offline advertising; the emerging Asian middle-class; the structural growth of video-gaming; and the structural shift to online betting from offline betting, to name just a few.

The fundamental value drivers of the businesses we own are resilient. And we believe the value of resilience to investors only increases with uncertainty. And in our new Trump-led Western world, there is certainly no shortage of uncertainty out there. But no matter what the world throws the businesses we own, our investors can rest assured knowing that their underlying demand drivers are solid and will continue to grow structurally.

The net result of our unique approach to investing is as follows. Over the initial years of Montaka’s life, we have delivered our investors two key benefits:

The decision to invest globally is one that all investors will face at some point. At Montaka, we offer a unique and logical approach to investing in high-quality global businesses which has resulted in attractive returns with a highly-complementary risk-profile. And we pride ourselves on delivering these results with a level of transparency for our investors that we believe remains unmatched in the marketplace.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Who are the businesses of the future?

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.