|

Getting your Trinity Audio player ready...

|

The concept of “disruption” is the subject of a great deal of discussion inside the four walls of Montaka. Whether it’s Uber disrupting taxis, or Airbnb disrupting hotels, disruption is forcing every incumbent business (and employee) to think deeply about who or what might “displace” it next.

A recent book written by senior directors of the McKinsey Global Institute called No Ordinary Disruption discusses the major disruptive forces that the world is currently facing – and is well worth the read.

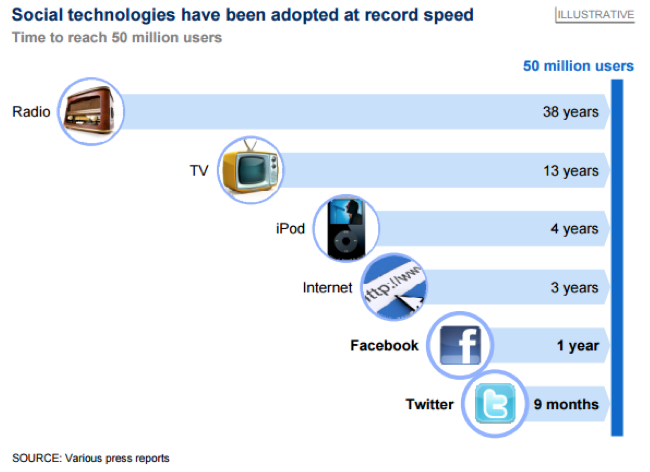

One major disruptive force naturally relates to technology and how we use it. One observation I thought was insightful was around the accelerating rate of new technology invention; combined with an accelerating rate of user adoption. We have arguably seen more instances of major technological advancement over the last 30 years than we had over the previous 200 years. And the propensity for consumers (particularly young consumers) to adopt new technology has increased materially, as the chart below by McKinsey serves to illustrate. The world is effectively speeding up.

Rapidly changing technologies combined with rapid consumer adoption is creating all sorts of new business models and industries. This spells both opportunity and threat for incumbent businesses – and is therefore highly relevant to investors as well.

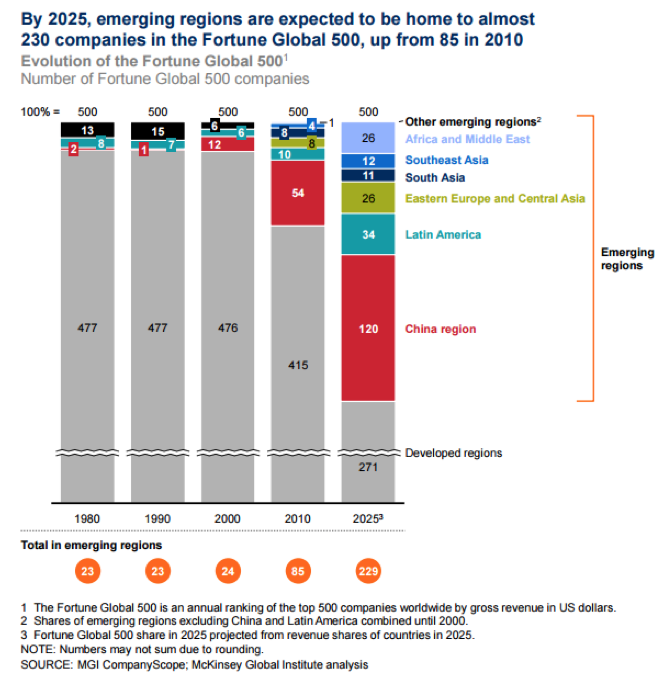

Consider that, in 1950, the average S&P 500 company could expect to stay in the index for more than 60 years. In 2011, that average was down to 18 years and, according to McKinsey, that trend shows no sign of easing. According to the consultancy, around 75 percent of the current S&P 500 will be replaced by 2027.

As illustrated by the chart below, it’s not just the Californian start-ups that are expected to disrupt the current Fortune Global 500. Indeed, the largest share gains in the Global 500 over the coming decade belong to China.

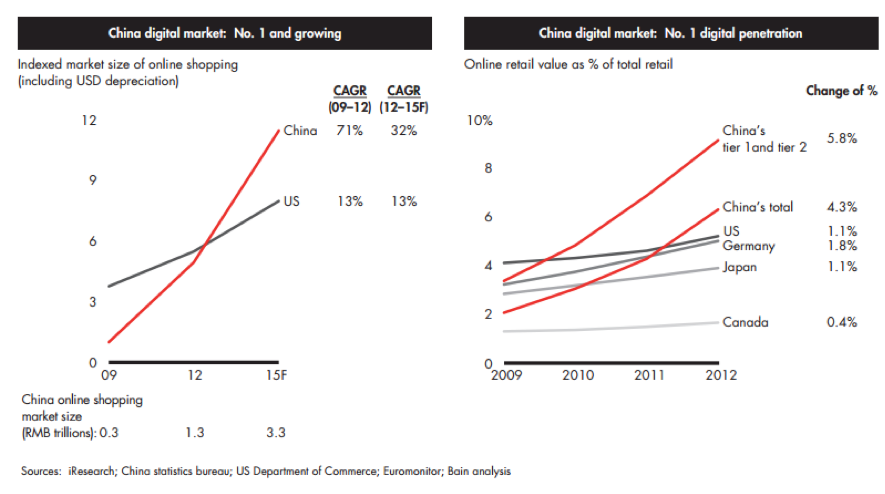

The emergence of China is not a new idea. Naturally, as a country of 1.4 billion citizens rapidly increases its wealth, opportunities to deliver goods and services emerge. We have already seen this in China’s online retail market. China’s online sales not only continue to grow rapidly, they are growing off a base that has well and truly surpassed that of the United States, as illustrated by Bain’s charts below.

Consider Alibaba (NYSE:BABA), China’s primary online retail platform – and the largest retail platform in the world. It already has around 400 million active users and processes around half a trillion US dollars in gross merchandise transactions every year. And it’s still growing north of 30 percent!

Chinese consumers have adopted online shopping extremely quickly. And most of this is now transacted via mobile (around 62 percent of current gross merchandise value on Alibaba to be precise). Consider that, Flipkart (the Amazon of India), is switching to a mobile-only offering.

The point is that technologies are changing rapidly and consumer behaviours are changing structurally. What worked in the past may not work in the future; and investors need to think carefully about who the winners and losers might be.

As we think about the Montaka portfolio today, we are positioned to benefit from a number of winners, such as Alibaba, on the long side; and a number of losers that are being disrupted on the short side. This ability to profit on behalf of clients from both winners and losers of these major global forces is one of the key propositions that makes Montaka’s strategy so valuable.

Montaka has owned the share of Alibaba since its inception.

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.