|

Getting your Trinity Audio player ready...

|

Following the U.S. Federal Reserve Bank’s recent decision to raise short term interest rates by 25bps (to 1.75-2.00%) and indicate 2 more are on the way this year, we thought it was an opportune time to revisit one of ourfavorite asymmetries when looking at businesses from the short side, namely debt and leverage. Generally speaking, if a company is taking on debt to fund projects that are unlikely to yield economic benefits, against a backdrop ofincreasing borrowing costs, we have identified the key ingredients that go into an excellent short opportunity. However, what happens if we are NOT looking at a company and are in fact talking about the world’s largest economy, namely the United States.

Fiscal legislation passed by the governing Republican party eliminated $1.5 trillion worth of tax receipts (over 10 years) and lifted the ceiling on discretionary spending, causing the U.S. Congressional Budget Office (CBO) to raise budgetdeficit estimates by ~50% YoY in 2018 andincrease to $1.5 trillion by 2028 causing the debt burden to eclipse levels last seen during World War II. The CBO noted:

“As a result of these deficits, U.S. debt held by the public will increase by more than $13 trillion over the next decade, from $15.5 trillion today to $28.7 trillion by 2028. Debt as a share of the economy will also rise rapidly, from today’s post-war record of 77% of GDP to above 96% of GDP by 2028″

U.S. Federal Debt as % of GDP

We should point out that deficits aren’t necessarily a bad thing in themselves, assuming they result in economic growth that pays for the investment (similar to capex and earnings for a business). However, this is another key point ofcontention, with the CBO strongly disagreeing with the Trump Administration’s estimate of where GDP growth will end up as a result of the fiscal package. The CBO estimates real GDP will grow at 1.8% p.a. over the 2018-2028 period, which is 60% lower than the~3.00% p.a. growth rate assumed by the Trump Administration in the 2019 budget.

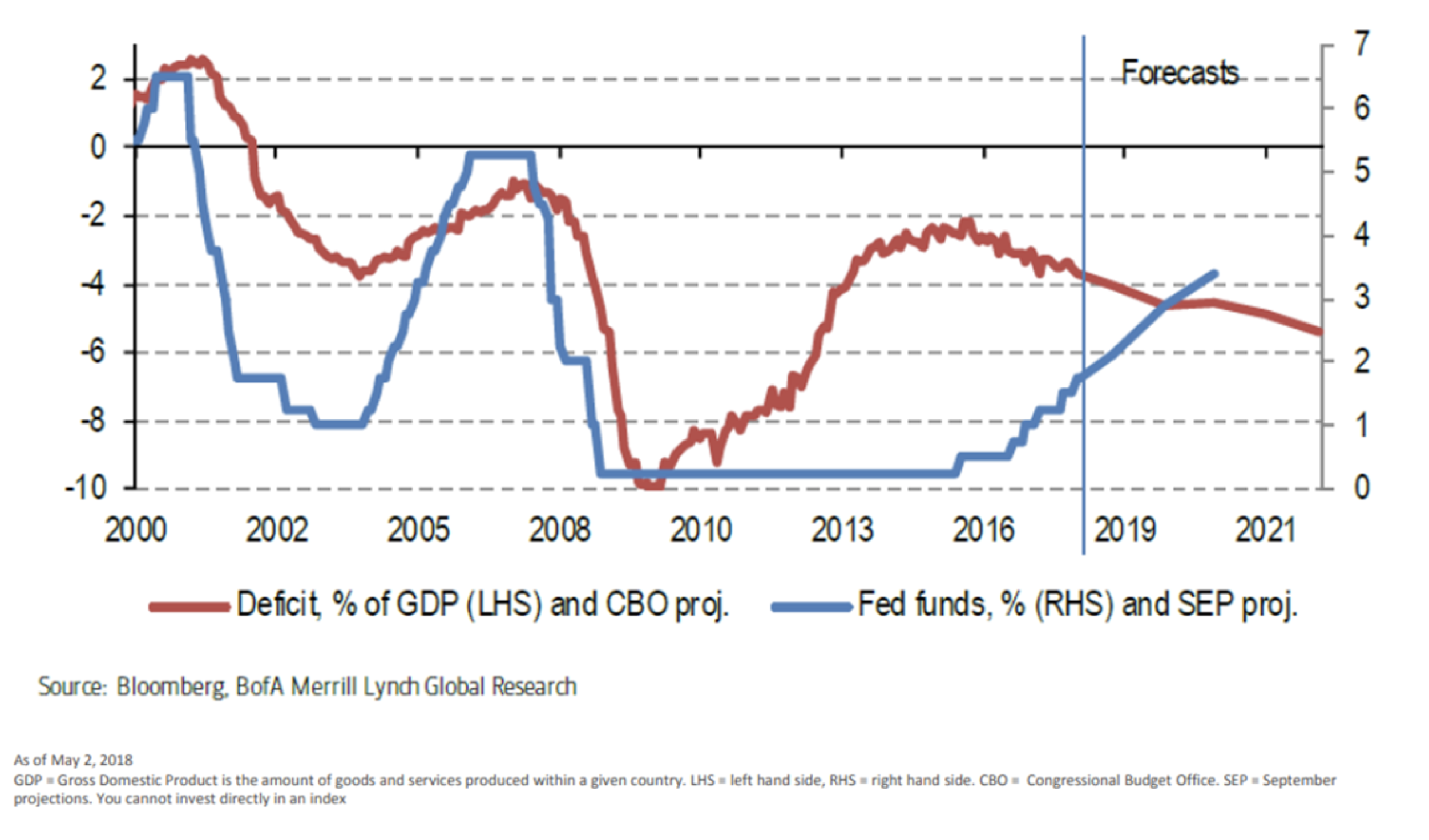

Meanwhile on themonetary side of the equation, the Federal Reserves’ dual mandate of full employment and price stability are consistently being met, with the jobless rate at 3.8% (a 17-year low) and inflation moving through its 2% target (CPI was 2.8% in May). Which is what makes the deficit expansion (driven by government policy) so unusual this late in the economic cycle. Historically speaking, the deficit expands when the Federal Reserve is cutting interest rates typically during or following a recession. DoubleLine’s Jefferey Gundlach sums up the paradox quite succinctly:

“This is almost like a suicide mission…at some point, with debt and its service cost increasing, there will be a collision. There could be a solvency problem” – Jeffrey Gundlach (June 12, 2018)

For a business this would indeed create the “solvency problem” Gundlach refers to, however for the U.S.a federal bankruptcy is basically impossible as it can print as much money as it needs to pay its debts. However doing so may create a negative feedback look and cause inflation and borrowing costs to spiral out of hand, which may be what Gundlach isalluding to. Perhaps more interestingly, Gundlach (aka “the bond king”) reiterated his forecast that U.S. 10-year Treasury yields would hit 6% in either 2020 or 2021, “we are right on track for that…exactly on pace” he said, which would see the long-term risk-free rate double from current ~3% levels.

Rising Deficits and Interest Rates: An Unusual Combination

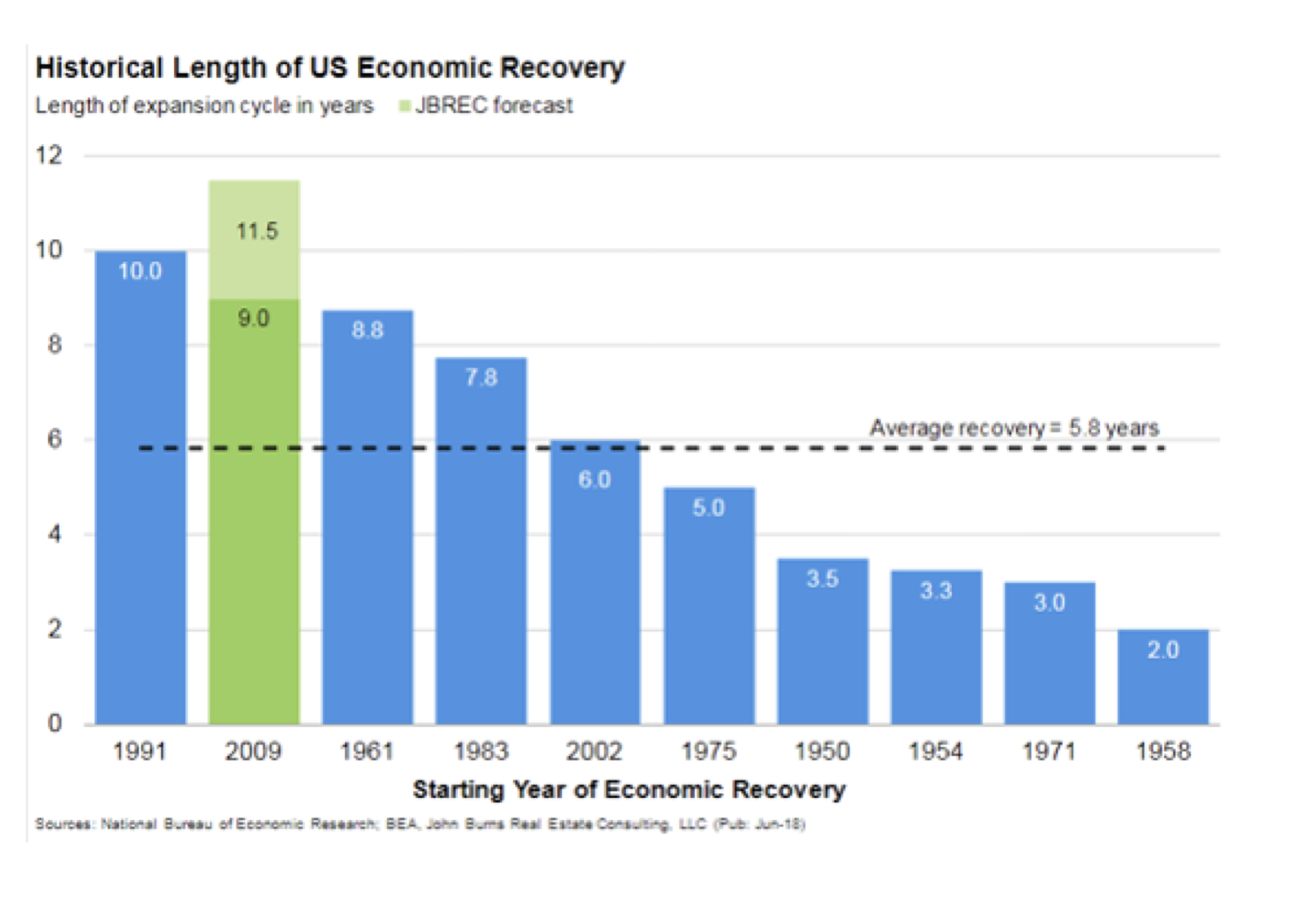

Finally, we are also approaching the longest post-recession economic recovery in U.S. history, which is now ~9 years in length with many indicators (shape of the yield curve, economic growth, etc) and commentators suggesting things will remain supported for the next couple of years. That said, there are very few asymmetries more powerful than a leverage imbalance. Debt can drive a seemingly calm and stable situation, into a disorderly, uncontrolled dislocation far more violently than most people expect. The embedded downside protection contained in the Montaka Global portfolio (i.e. the short book) is well prepared for such an outcome whenever it may occur, and perhaps even looking forward to it just a little!

Finally, we are also approaching the longest post-recession economic recovery in U.S. history, which is now ~9 years in length with many indicators (shape of the yield curve, economic growth, etc) and commentators suggesting things will remain supported for the next couple of years. That said, there are very few asymmetries more powerful than a leverage imbalance. Debt can drive a seemingly calm and stable situation, into a disorderly, uncontrolled dislocation far more violently than most people expect. The embedded downside protection contained in the Montaka Global portfolio (i.e. the short book) is well prepared for such an outcome whenever it may occur, and perhaps even looking forward to it just a little!

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.