|

Getting your Trinity Audio player ready...

|

-Christopher Demasi

Passive investing has surged in popularity in the past decade, and more recently during Covid-19. According to Morningstar, Australians poured $24.5 billion into passively managed funds in the year to March 31, 2021, while active funds shed $6.7 billion.

That’s not surprising given that funds that track broad stock market indexes such as the ASX200 and S&P500 have performed strongly and outpaced most actively managed stock funds, at a fraction of their cost.

Many argue that this is compelling evidence that actively managed funds are doomed to perennially underperform and should continue to be shunned entirely by investors.

We believe this could be a costly mistake. The conditions that made passive funds winners are changing. In the next decade, actively managed funds will be vital for investors to reach their important financial goals.

But when choosing active funds, investors will need to be selective. There are two essential traits that identify exceptional managers that do outperform in the long run. In the current environment investors should be looking to add these funds to their portfolios to power superior compounding in the future and maximise their wealth.

The two characteristics of active outperformance

In 2016, Martijn Cremers and Ankur Pareek published a ground-breaking research report. It showed that only the most distinct and most patient funds go on to meaningfully outperform the stock market over very long periods. Importantly, these characteristics are not just useful in hindsight. Investors can use them in advance to select funds that outperform.

* High Active Share

The most distinct funds, firstly, have high Active Share. Active Share is the proportion of a portfolio that is invested differently from the market at the beginning of a period. Highly concentrated stock pickers, for example, have high Active Share of 90% or more typically. On the other hand, ‘closet indexers’ with diversified and undifferentiated portfolios that look like the market (often despite claims otherwise) have low Active Share of 60% or less.

* Long Fund Duration

The second characteristic of outperforming active funds is long Fund Duration. Fund Duration is the average length of time a fund has held the stocks in its portfolio over the previous five years. Managers with long Fund Duration hold stocks at least two years, while short Fund Duration managers usually sell stocks eight months after purchasing them.

The Active Share edge

In their study of more than 3,000 equity mutual funds over 26 years from 1990 to 2015, Cremers and Pareek found that only funds in the top quintile of Active Share – typically the stock pickers scoring above 90% – tend to outperform the broader share market by almost 1% per annum, while lower Active Share funds generally underperform, some dramatically so.

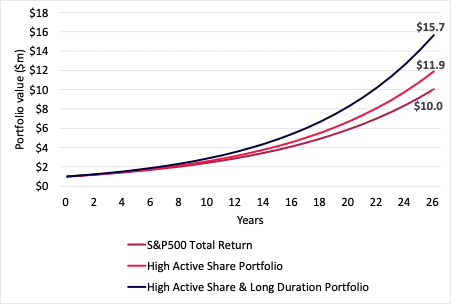

This seemingly small yearly benefit becomes extraordinarily large when compounded over more than a quarter of a century, when the market appreciated at 9.4% per annum on average. A portfolio of the highest Active Share funds would have beaten the market by more than 180%. A hypothetical investor with initial capital of $1 million would be almost $2 million wealthier by allocating to the most active managers, instead of a passive index fund.

The result is powerful and underscores the importance of distinguishing concentrated active funds from the rest, especially closet index funds, which Cremer first recognized in a 2009 paper.

The power of patience

But building on this, the two researchers then examined how differently patient managers performed when compared to funds trading frequently. The results were more striking still.

Among the funds with highest Active Share, Cremers and Pareek found that only those also in the top quintile of Fund Duration – the long-term investors that stick to their convictions longer than two years – outperform … and by almost 2% per annum. Less patient managers underperformed regardless of how active and concentrated they were, and, in fact, the more they traded the worse they performed.

Basically, patience paid off in spades.

By allocating the initial $1 million of capital to a portfolio of those most concentrated active managers that were also the most patient with their holdings, the earlier hypothetical investor would have outperformed the market by an additional 380% and be another $3.8 million richer.

Concentrated and patient active portfolios compared to the market

(Initial capital of $1 million grown over 26 years)

Source: Montaka

Perverse forces at play

Armed with this insight it may then be surprising to learn that the set of managers who are both highly concentrated and very patient is very limited.

After all, if these are the hallmarks of success wouldn’t you expect more managers would want to be like this?

The researchers suggest this is easier said than done because there are strong perverse forces at play in the funds management industry. Being concentrated and holding long-term convictions may be a pathway to superior profitability in the long run, but it comes with a high likelihood of frequent short-run underperformance, jeopardizing a fund manager’s career and irritating impatient clients.

Concentrated and patient

At Montaka, ‘High Conviction’ and ‘Long-Term Perspective’ are two of our core principles. We have created a structure and mindset required to achieve superior long-term compounding by owning a concentrated portfolio of high-conviction investments and patiently holding them for many years or even decades.

This becomes clear by applying the research measures to our funds.

Montaka’s funds have very high Active Share. The Montaka Global Long Only Equities Fund (MOGL) scores around 90%, in line with the most concentrated stock pickers on the planet. The Montaka Global Extension Fund (MKAX) scores almost 130%. This reflects a limited number of 27 holdings in the long portfolios (we exclude 84% of the market index), and large investments in the best opportunities – our top holdings are 8% and 14% of the funds’ assets, respectively.

While the funds hold some of the world’s largest companies in common with the index, given we believe they represent extraordinary long-term compounding opportunities, we back them heavily. For example, Alphabet, Google’s parent company, is a 7.4% holding in MOGL and 9.6% in MKAX whereas the MSCI World Index only holds a 2.3% position in this excellent business.

Montaka’s funds also have very long duration holdings; much longer than some of the most patient equity funds in the world. The average holding period of the top 10 stocks in the long portfolios is approximately four years – double the threshold in the study – and we expect continued low turnover in future.

A different world

Passive investing strategies have undoubtedly been a rewarding experience for investors for more than a decade. Performance has been strong, and it has come cheaply. The longest equity bull market in history was only briefly interrupted, volatility has otherwise been extraordinarily low, interest rates have fallen towards zero, central banks have flooded markets with liquidity, and governments have made enormous fiscal injections into their economies.

But the conditions that made passive gains so easy are changing.

Now more than ever, investors need funds that will outperform the broad stock market indexes to power the compounding needed to reach their financial goals and maximise their wealth in the decades ahead. Active management as an industry has failed to deliver in the past, but the most concentrated and patient fund managers do outperform over the long term. Investors should consider adding managers with these important attributes to their portfolios – and soon.

Note: Montaka owns shares in Alphabet

Chris Demasi is a Portfolio Manager with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.