|

Getting your Trinity Audio player ready...

|

“Take a look out there at Port Phillip Bay. It’s so calm you could water ski across it. But who knows how big the shark is lurking just beneath the surface.”

Powerfully capturing the investing backdrop of today, I would like to be able to claim these words as my very own. Or attribute them to Andrew, Montaka’s CIO and my business partner for the past 3 years. Or tag it to any member of the Montaka team. Rather, this quote is a testament to the astute and insightful partners that we work for at Montaka. On a recent morning in Melbourne, a client and friend of the firm paused during our meeting and, with this concise phrase, reminded us of the non-linear nature of financial markets, human psychology, and the unique role of the Montaka strategy in dealing with them.

Calm on the Surface

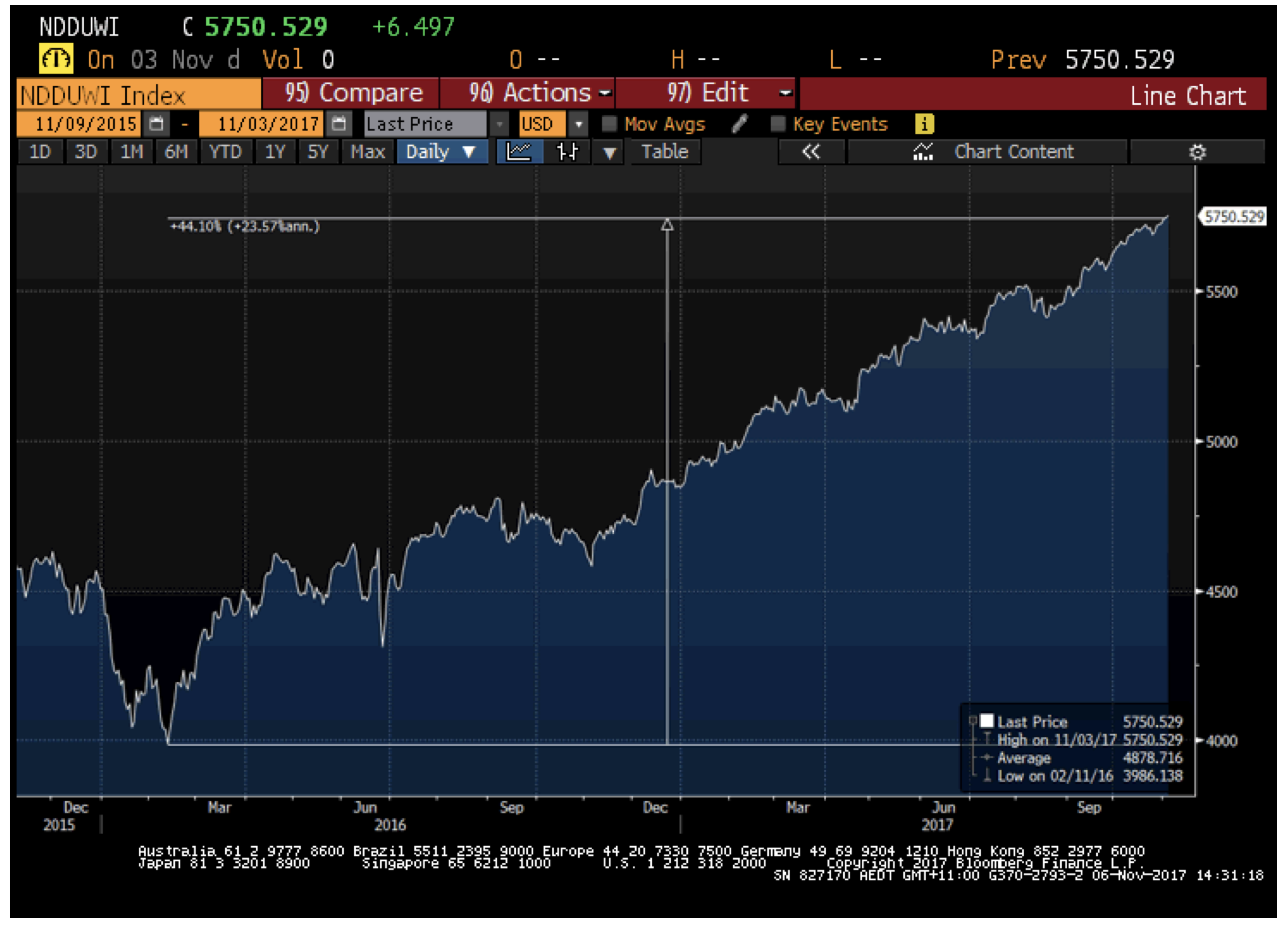

For almost the past two years, global equity markets have only known one direction. Since bottoming in February 2016 the MSCI World Net Total Return Index, a broad measure of the performance of stocks worldwide, has risen 44% in US dollar terms to a record level. The appreciation represents an annualised pace of 24%, more than 4 times the average annual gain in equities over the last half century. Astoundingly equities have advanced strongly despite the threats and realizations (both should rattle equity investors) of myriad macroeconomic and political upheavals.

MSCI World Net Total Return Index (USD): Last 2 Years

Source: Bloomberg

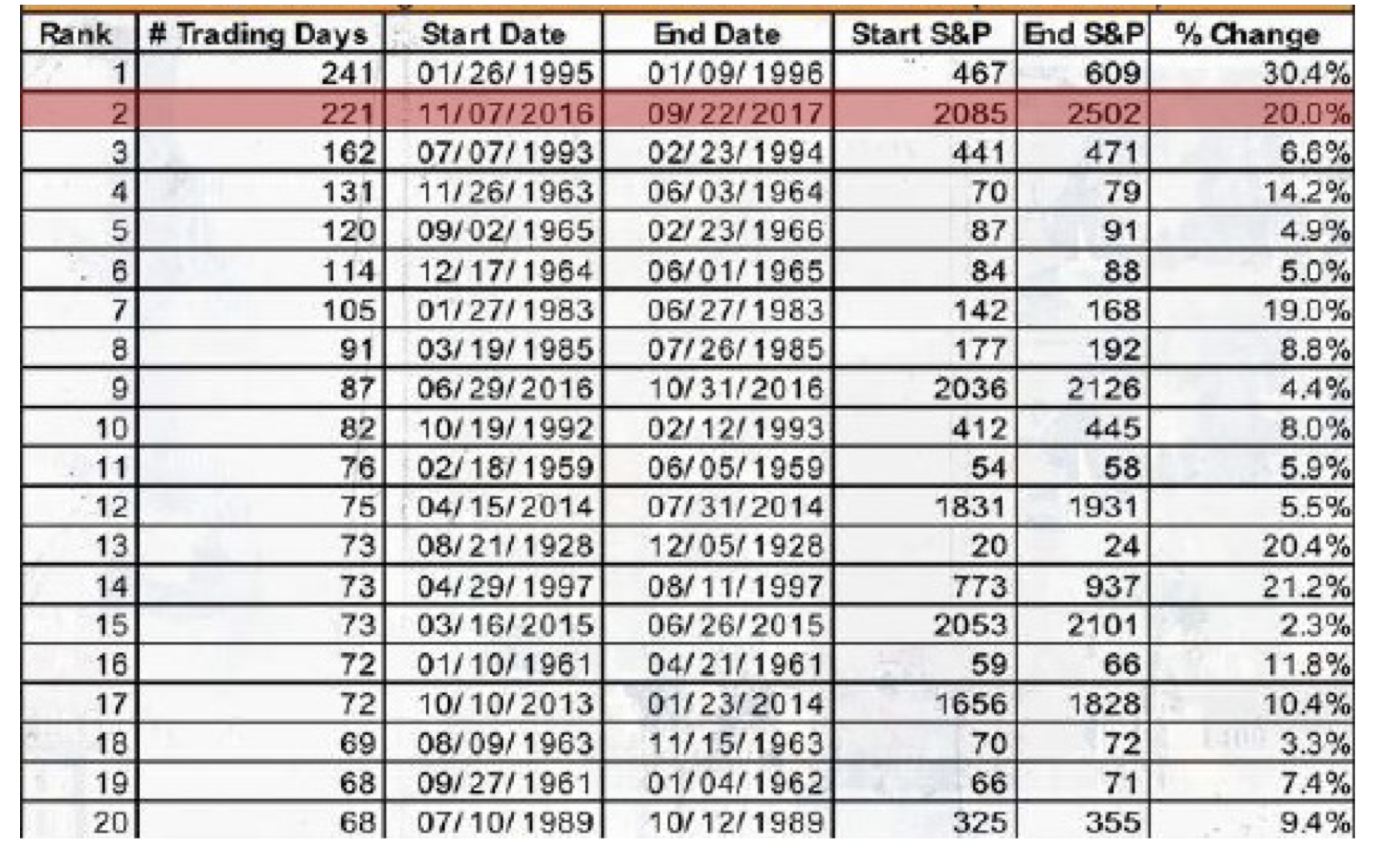

Even more astonishing is that equity markets have not taken a backward step in their march to repeated new highs. The current run in the US equity market, as measured by the S&P500 index, is the second longest stretch in a 90-year history without a 3% pull back. As the publisher of this data, Real Vision, comments: down days appear to be a thing of the past.

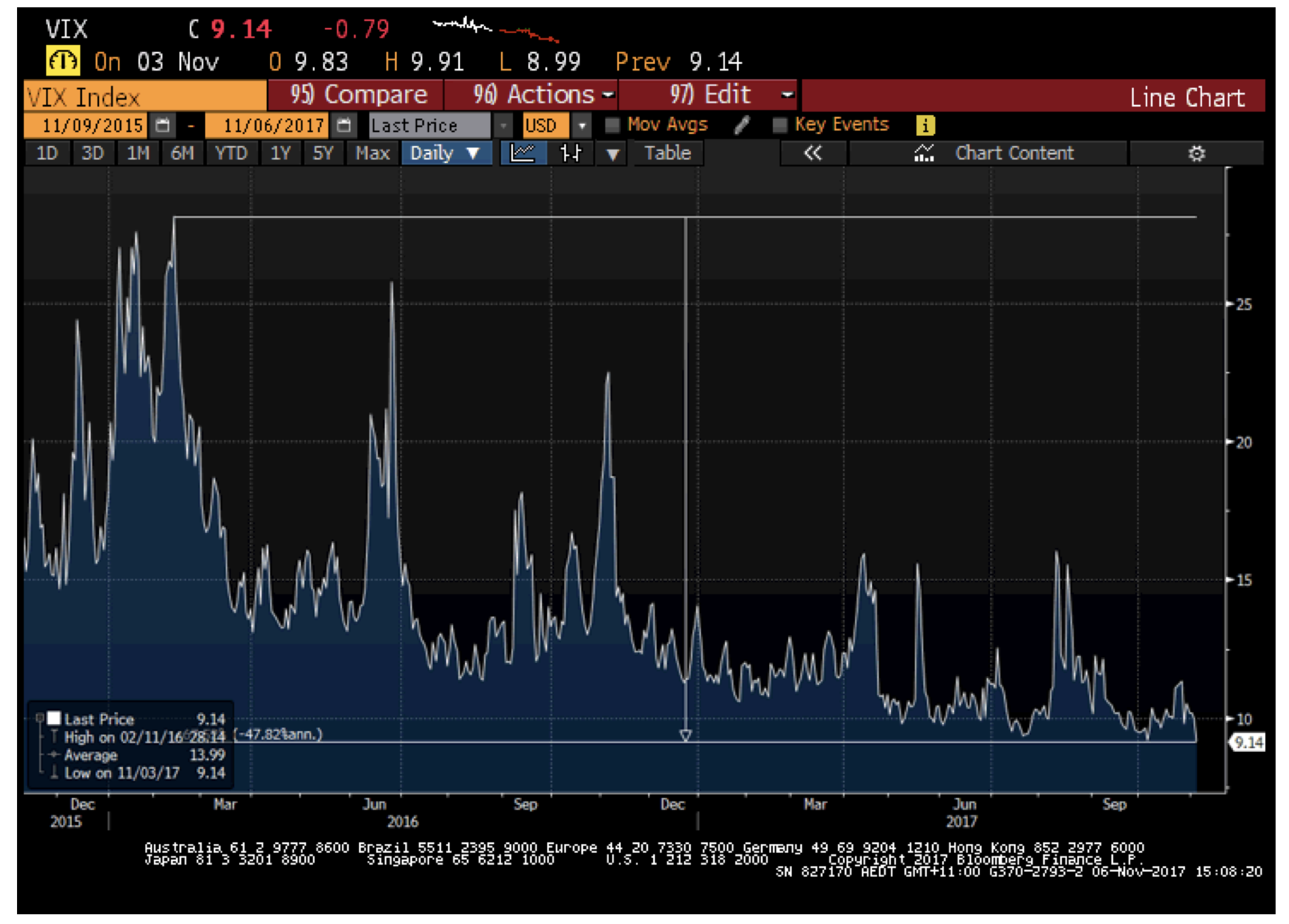

Moreover, the ride in equity markets is only expected to become smoother. The CBOE SPX VIX, or Volatility Index, which estimates future volatility in the S&P500 index has fallen by about two-thirds from a short peak in February 2016 to a record low level of just 9.

S&P500: Longest Streaks Without 3% Drawdown (1928-2017)

Source: Real Vision

VIX Index: Last 2 Years

Source: Bloomberg

Turkeys?

Human beings are notoriously bad at being able to envisage the possibility that tomorrow might look very different to yesterday. In fact, the longer the stock market’s appreciation goes on and with less disturbance along the way, the harder it will be for investors to prepare for the possibility that it might one day change. Worse still it becomes unimaginable that the change may be dramatic.

Nassim Taleb, the famed scholar and author, whose works such as the 2007 book The Black Swan have focussed on the human mind’s indefensibility against random patterns, describes this concept with the metaphor of a feeding turkey:

“The turkey is fed 1,000 days in a row. The feedings reinforce the turkey’s sense of security and well-being, until one day before Thanksgiving an unexpected and uninvited bad event occurs. All of the turkey’s experience and feedback is positive until fortune take a turn for the worse.”

While we may think the looming spectre of nuclear war or a disastrous end to central banker experimentations would serve to temper our expectations, and the market’s advances, Nobel Prize winner Richard Thaler may argue that their recurring presence over the past two years might actually embolden investors.

In his 2008 book Nudge, co-authored with Cass Sunstein, Thaler explains the availability heuristic, one of several behavioural biases that lead to poor decision-making. Simply put the availability heuristic is a mental shortcut that relies on the notion that if something is easily recalled it is more important. Consequently, people systematically weight their judgements toward the most recent experience. Perhaps we could extrapolate that each time the market rises against the risk of potentially harmful macro event, the more investors become desensitized to the next, and the market keeps marching higher despite them (or because of them?!)

ETFs Might Lie Beneath

By now some readers might surmise that exogenous risks have a tough time jolting equity markets. By the numbers those readers would be right. In a 2007 paper Michael Mauboussin, Director of Research at BlueMountain Capital Management and adjunct professor at Columbia Business School, estimates that “80 percent of the market’s largest moves in the past 60 years are attributable to endogenous [internal] activity”. So if Brexit nor Trump nor North Korea nor ISIS can stop the markets, where might a pullback come from?

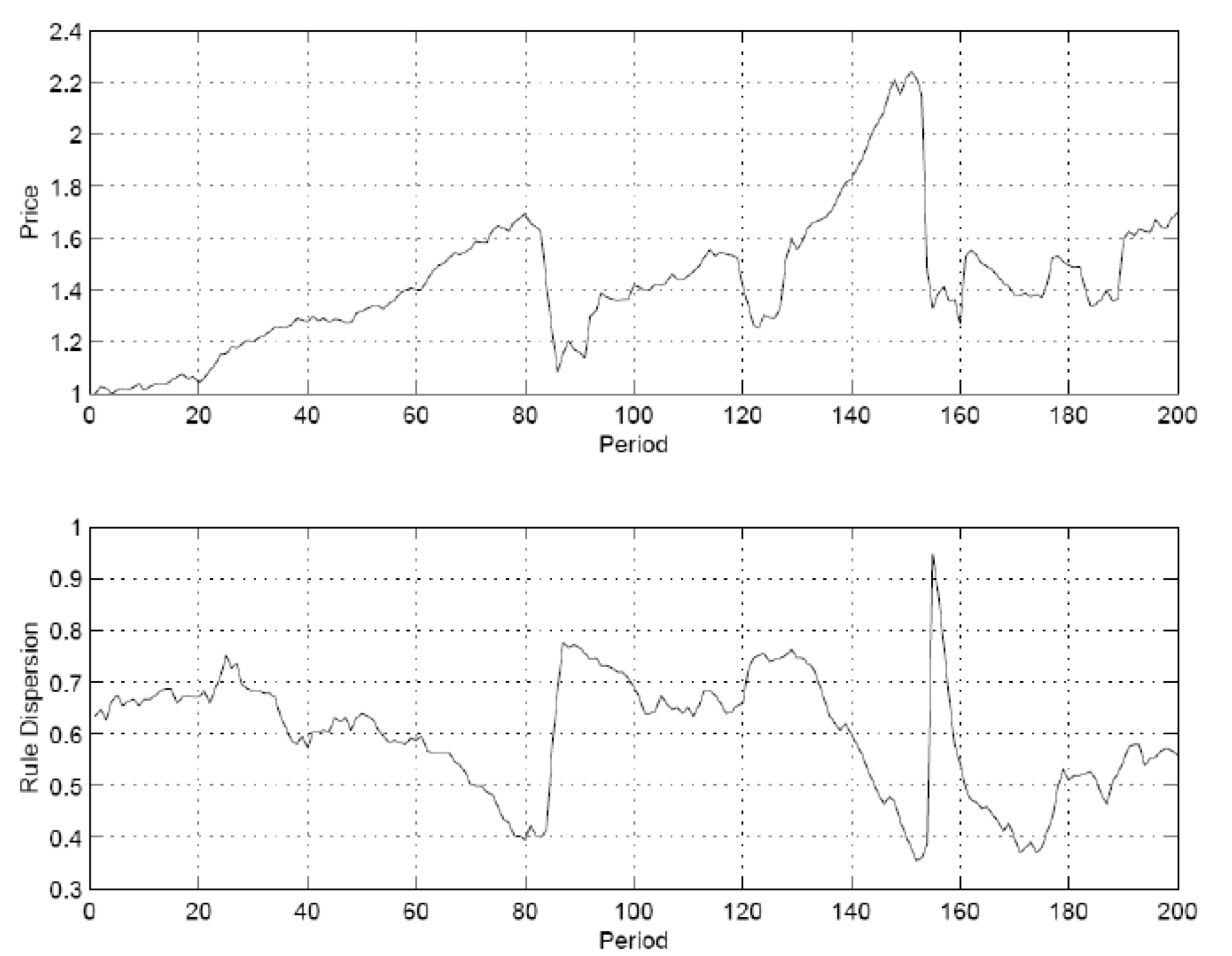

Mauboussin’s paper goes on to cite the work of economist Blake LeBaron, a leader in creating models to analyse economic problems, including asset pricing. In one such model LeBaron used 1,000 agents each with well-defined portfolio objectives and a menu of trading strategies. He then let them trade and watched the results. One key finding was the relationship between diversity – how disperse trading strategies, or how different traders were – and asset price.

As the diversity of trading strategies declined steadily, prices increased. Once diversity hit a low point asset prices reached an “invisible vulnerability”, much like the very fat and happy Turkey on day 1,000, and then fell significantly (see the first 80 trading periods in the two charts below).

As LeBaron described it:

“Agents begin to use very similar trading strategies as their common good performance begins to self-reinforce. This makes the population very brittle, in that a small reduction in the demand for shares could have a strong destabilizing impact on the market… Traders have a hard time finding anyone to sell to in a falling market since everyone else is following very similar strategies…this forces the price to drop by a large magnitude to clear the market.”

Asset Prices and Diversity (Dispersion)

Source: Blake LeBaron

While lack of diversity may be a plausible signal of the potential for a meaningful pullback in otherwise seemingly benign and rising equity markets, it is often difficult to accurately measure. That said, it has been clear to us for some time that one particular investor group is accounting for increasing ownership and trading flows of equities: exchange-traded funds (ETFs).

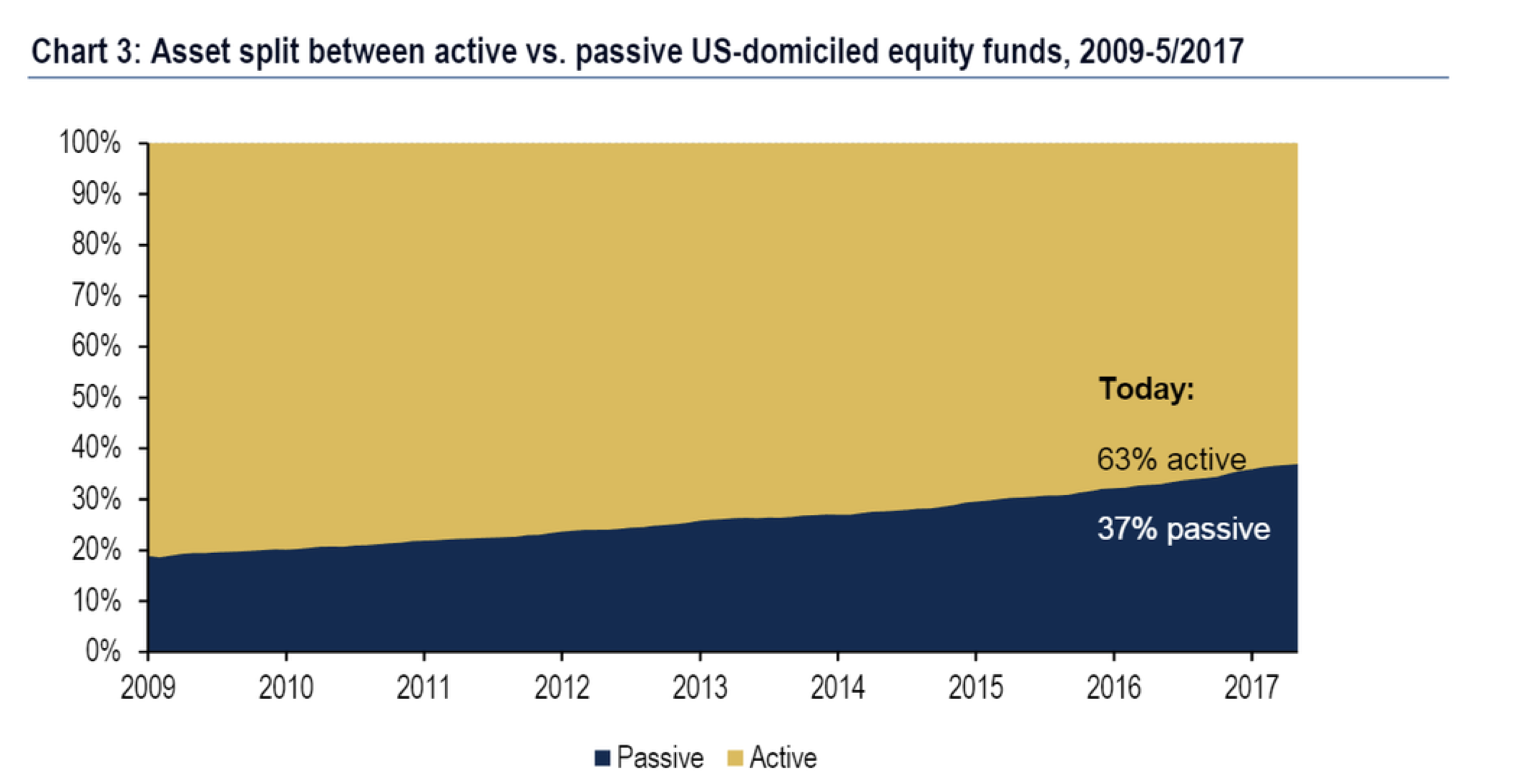

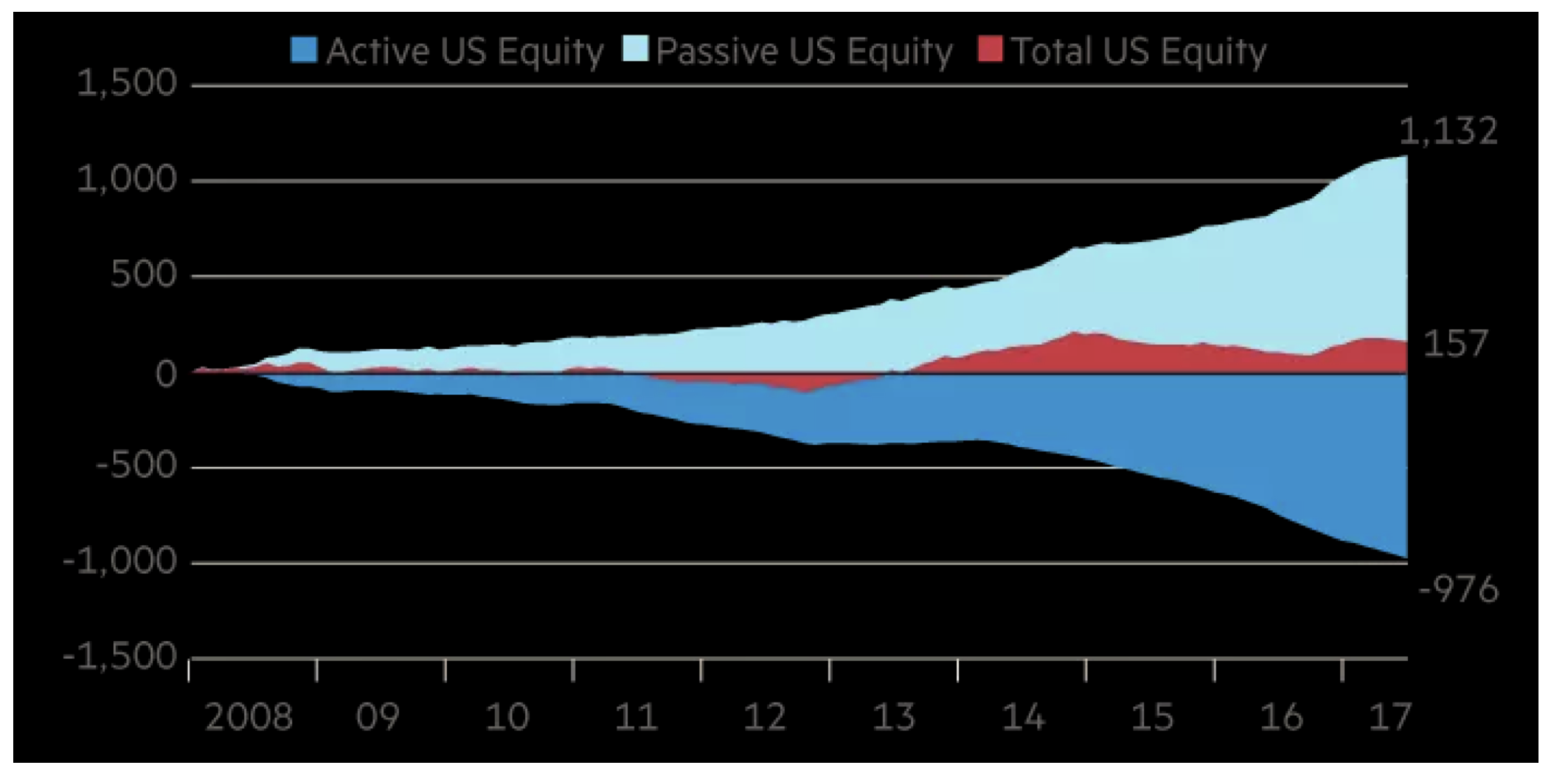

Following the financial crisis, the proportion of equity-fund assets owned by passive funds – largely ETFs – has increased from 19% in 2009 to 37% in 2017 according to Bank of America Merrill Lynch. Cumulative flows into passive equity ETFs in the US over this period now exceed US$1 trillion, while outflows from active equity ETFs in the US are around the US$1 trillion mark. Bernstein, a US broker, believes that passive funds will hold more than half all US equity assets by some time in 2018.

Equity Ownership by ETFs (Passive)

Source: Bank of America Merrill Lynch

Domestic US Equity Cumulative Flows (US$ billion)

Source: Morgan Stanley

To the extent that ETFs employ a similar trading strategy – buying stocks based on size and momentum, independent of price and value – and their prominence continues to rise, we should expect to see equity market diversity continue to decline.

Montaka’s Position(ing)

While we have no way of knowing if, let alone when nor precisely why, a fall in equity markets might occur, Montaka has the tools and positioning to protect client capital in a downside scenario.

The main line of defence is Montaka’s variable net exposure to the market, which today sits around 50%. All else equal we would expect the fund to realize just half of any broad-based fall in equity markets. Montaka’s protections extend deeper than the portfolio net exposure to the stock level.

On the long side, Montaka acquires shares in high quality businesses with expectations that are unreasonably conservative. This gives the long portfolio a collection of 22 stock positions, each with a significant margin of safety, which provides insulation against unexpected adverse developments.

On the short side, Montaka sells short deteriorating businesses that meet up to four exhaustive criteria that form a unique framework – it is proprietary to Montaka. When the market falls Montaka’s short book of around 30 stocks should act like an insurance policy when it is paying out.

Combined with a starting position low to the ground, Montaka’s unique frameworks for security selection give the fund a differentiated ability to protect the downside. In markets that are steadily rising the value of this protection may go underappreciated. When market conditions change, however unimaginable this may seem today, Montaka’s defensive features will prove invaluable to our insightful clients.

![]() Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.