|

Getting your Trinity Audio player ready...

|

Next week will mark the two-year anniversary of Microsoft first being added to Montaka’s long portfolio. At the time Microsoft traded at around $50 per share, which we believed to be considerably cheap. Since then the stock has risen strongly, peaking at $95 last week and trading at $85 overnight. At the same time the business has outperformed expectations, increased its earnings power and demonstrated the potential to continue to grow strongly into the future. So much so that even at today’s share price Microsoft still deserves its position in Montaka’s long portfolio. You might say that Microsoft has shifted the goal posts on us – in a very pleasing way.

Microsoft share price performance (last two years)

Microsoft today

Founded as Micro-Soft in 1975 by childhood friends William Henry Gates III (he goes by “Bill”) and Paul Allen, today Microsoft is the world’s largest software company by revenue, on target to surpass US$100 billion of sales this financial year. Most readers will identify Microsoft by the programs used on work and personal computers, like Windows and Excel. Yet the company offers even more software across a range of purposes and (perhaps surprisingly for some) heavily weighted toward business users.

Microsoft breaks itself into three reportable divisions, any one of which would itself be among the top 2 global software companies by revenue. The three segments are:

- Productivity and Business Processes (PBP), which is essentially the suite of Office applications including Word, Excel, Outlook and PowerPoint. Traditionally these applications were installed on the PC. Today most new business is going toward the cloud subscription version called Office365. Either way Microsoft has a virtual monopoly with these business process apps. PBP generates around $35 billion of revenues annually

- Intelligent Cloud (IC), which includes the SQL Server database software and Windows Server operating system for business datacenters. Like PBP, new sales in the IC segment are flowing to cloud services called Azure. Along with Oracle and IBM, Microsoft dominates the market for this type of software. IC generates around $30 billion of revenues annually

- More Personal Computing (MPC), includes a lot of different consumer computing offerings from the Xbox gaming console to the Surface tablet. But the jewel in MPC is the Windows franchise. Windows is the operating system that allows almost every PC sold to run. Microsoft has a virtual monopoly here (I know there are Mac users in the readership, but I did say virtual). MPC’s revenues are closer to $40 billion

Better than expected

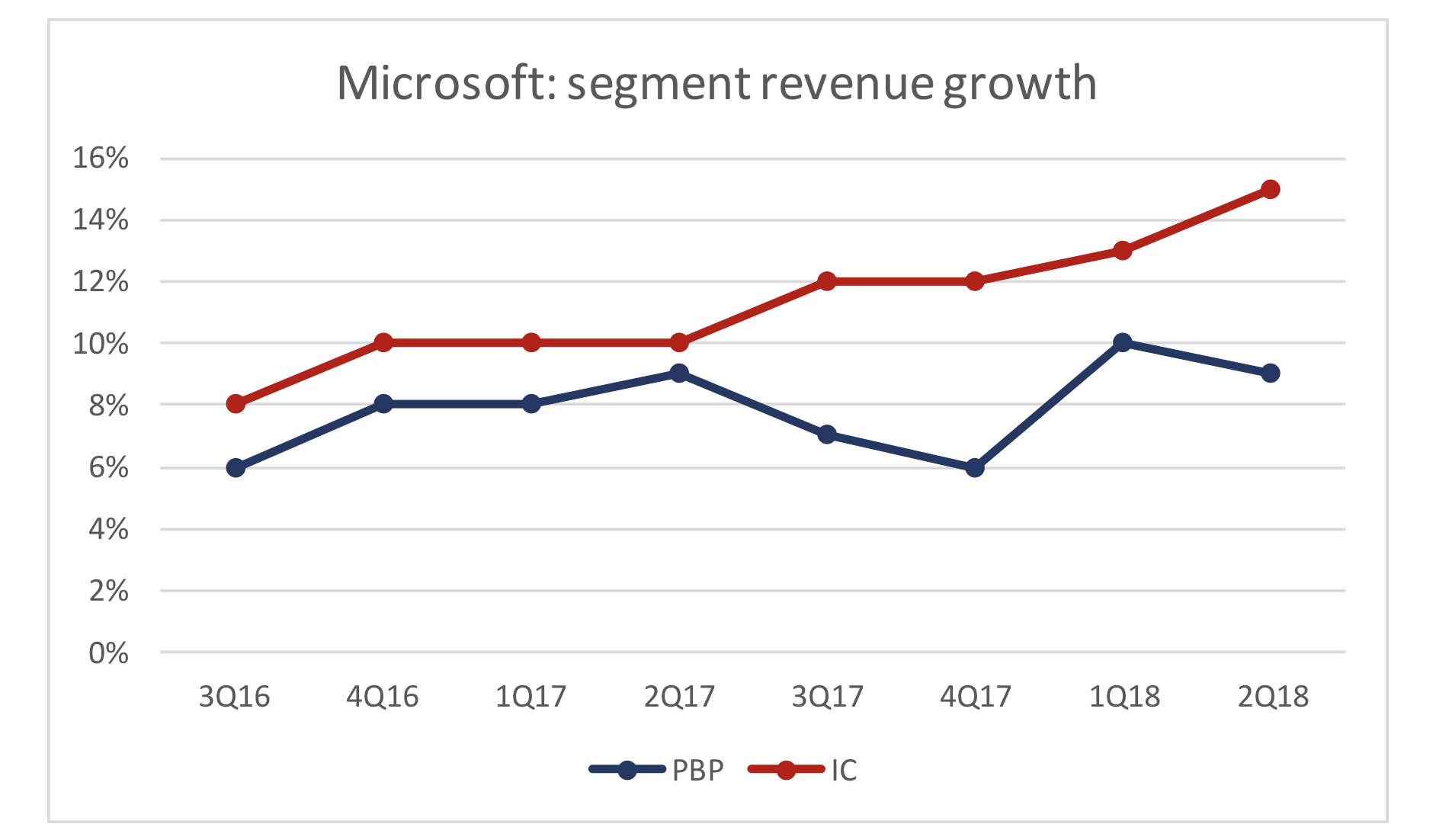

When we analysed Microsoft at the beginning of 2016 we took the same approach we take to every stock – that is, to reverse engineer the market implied expectations for the key drivers of the business, and then determine if these are unreasonably conservative or otherwise. In short, we believed that at $50 per share the market was pricing in average annual revenue growth over the next 20 years (we take the long view) for the key PBP and IC segments of around 5% and 6%, respectively. And we thought this was quite conservative. By comparison, in the 2016 financial year PBP grew 6% in constant currency terms and IC grew 11% on the same measure.

We saw a few reasons that Microsoft’s key business segments should outpace expectations and begin to accelerate. As a near-monopolist in both the business process applications market (Office) and the operating and database software markets (Windows, SQL) we thought Microsoft should enjoy pricing power and positive mix shift to higher value products, services and tools. At the same time the number of business users and use cases for Microsoft’s PBP and IC offerings were growing. Further, both segments were actively transitioning their sticky user bases to cloud versions of their traditional products. And with cloud would come a greater share of each customers’ wallet.

Over the subsequent two years Microsoft went on to surprise to the upside against market implied expectations. PBP averaged 8% annual revenue growth in constant currency terms (versus a 5% hurdle) and IC averaged 11% growth (versus a 6% hurdle). Even more impressive has been the acceleration demonstrated in both segments. PBP exited the most recent quarter growing at close to double-digit rates and IC had lifted its growth rate to 15%.

The cloud

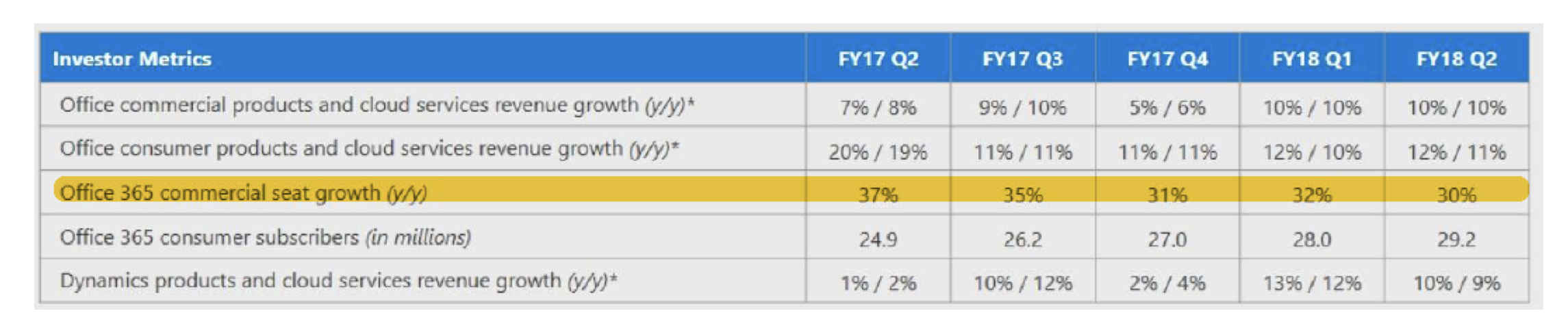

As we suspected the cloud pieces of each segment would go on to drive higher growth rates. In PBP, the Office365 suite of cloud applications (recall: this is all the old favourites like Excel, Word, Outlook and PowerPoint installed on Microsoft’s computers and delivered over the internet rather than being installed on the user’s computer) has seen annual commercial user seat growth of more than 30% over the last five quarters. At the same time average revenue per user (ARPU), which reflects price increases and the sale of higher value offerings, has consistently grown at double digit rates over this period. Said another way, as Microsoft pulls the pricing lever it still attracts more and more customers. Actually, said an even better way, Microsoft has pricing power!

Office365 commercial seat growth 30%+

*reported growth/constant currency growth

*reported growth/constant currency growth

And in IC, Microsoft’s cloud platform Azure has seen even more astounding growth, almost doubling year-over-year in each of the last five quarters. While this is a fantastic result in and of itself, we think it even more impressive that IC’s traditional server/database business is still growing, even as customers transition workloads to the Azure cloud offering.

Azure almost doubling year over year

*reported growth/constant currency growth

What now?

When a stock is up 70% in two years it usually begs the question: have you sold? In fact, we often talk with clients about our position sizing framework, which goes something like this:

“When a stock price appreciates all else equal, the market implied expectations for the business have increased and are becoming less conservative. In other words, the stock is becoming less cheap/more expensive and we would systematically trim the position”

The all else equal is important. When it comes to the case of Microsoft all else is not equal. To begin with, in the past two years the earnings power of the business has increased significantly. In financial year 2016 Microsoft generated revenues of $92 billion and earned $28 billion in operating income (that is, before interest and taxes). This year Microsoft is set to generate $105 billion in revenues and earn around $33 billion in operating income.

Just as importantly, or perhaps even more importantly, Microsoft has demonstrated an ability to grow at higher and accelerating rates in its two key segments: PBP and IC. Sure, expectations have risen. We think an $85 share price now requires 7% to 8% average annual growth rates in PBC and IC. But growth is already exceeding these levels, has done for a while now, and has been on an upward trajectory. With all the same growth drivers in place today as were present a couple of years ago, we think Microsoft is likely to continue beating market implied growth estimates. And while we continue to hold this view we will continue to be long Microsoft shares on behalf of Montaka clients.

Montaka owns shares in Microsoft

![]() Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.