By Andrew Macken

As Warren Buffett rightly pointed out: “Price is what you pay, while value is what you get.”

The distinction between value and price is one of the most important for an investor to keep in mind. This is particularly true when stock prices – or even unit prices of managed funds – fall.

Montaka’s funds are no exception – unit prices have fallen, driven most substantively by declines in many of the stocks we own, as well as a significant rally in the AUD, which hurts the translation of our global returns in local-currency terms.

But do these price falls reflect declines in the underlying business value of our holdings?

We don’t think so.

As you’ll see in the analysis below, when it comes to revenues and earnings, Montaka’s holdings continue to perform very well fundamentally.

The only change is that in recent months their valuation multiples have significantly derated.

That disconnect – between price (what investors are paying) and performance (what investors are getting) – means that companies with strong competitive advantages are ‘on sale’ today.

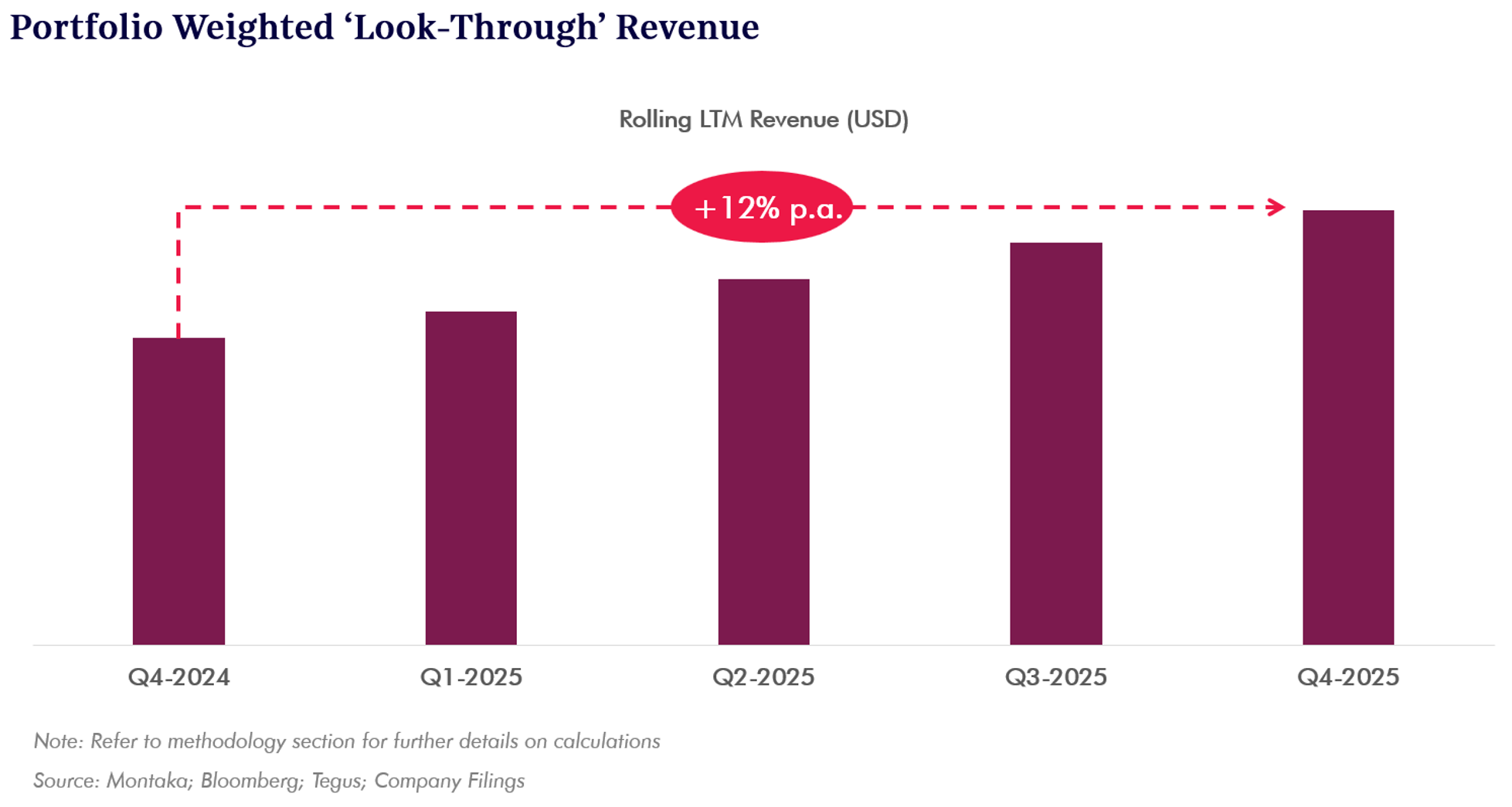

Revenues continue to grow strongly

When we calculate a measure of weighted look-through revenues (aggregate revenue adjusted for the size of each investment) of Montaka’s indicative portfolio over time, we see consistent double-digit percentage annual growth, up to and including the most recent quarter.

This was underpinned by consistently strong revenue growth from the likes of Meta, Microsoft, Amazon, Alphabet, ServiceNow, and S&P Global, to name just a few.

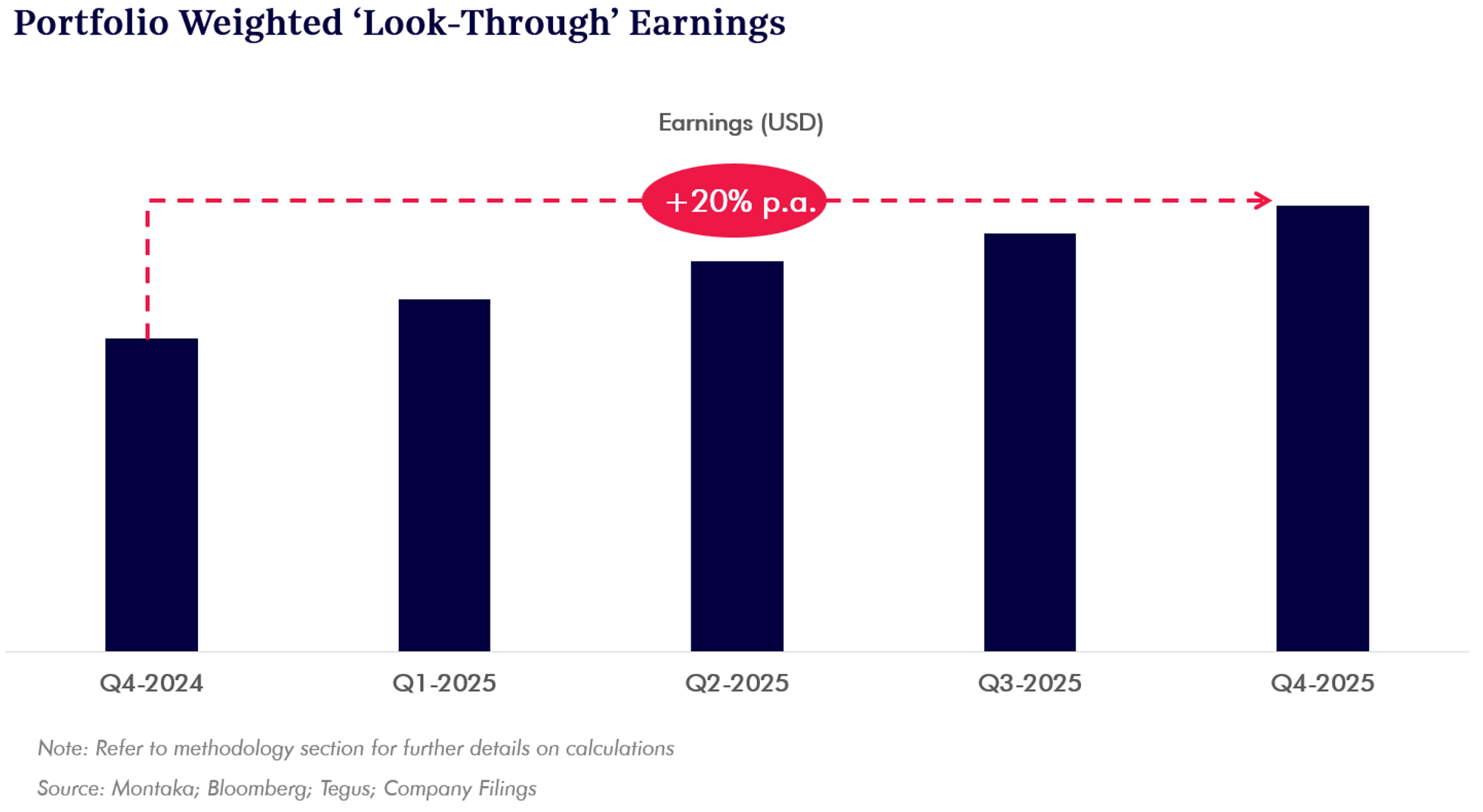

Earnings also continue to grow strongly

Similarly, Montaka’s indicative portfolio weighted look-through earnings shows even faster growth.

This relatively faster earnings growth is driven by highly favorable incremental economics.

Incremental profit margins, for example, are the profit margins on the growth in revenues (or how much extra profit the company makes when it sells more), rather than the margin on the company’s existing base of recurring revenues.

When a company’s incremental profit margins hold, the overall operating profit margin will gradually approach this level. The incremental margin works like a ‘magnet’, slowly attracting the average margin towards it over time.

Tencent provides a wonderful case study in incremental economics. In its most recent quarter, which was handed down a couple of weeks ago, the company reported the following:

- Gross margin of 56%, but with an incremental gross margin of 80%.

- Operating profits (EBITA) margin of 36%, but with an incremental operating profit margin of 89%.[1]

Tencent has demonstrated it can grow revenues at higher profit margins than its existing revenues.

That’s because most of the incremental revenues have been built on top of the existing (mostly fixed cost) technology platform. So the incremental variable costs required to earn these new revenues are much lower.

This is why profit margins have been expanding. And this is why, with only 13% per annum revenue growth, Tencent was able to grow its operating profits by nearly 40% per annum!

A unique opportunity

Montaka’s holdings, including the likes of Tencent, Meta, Microsoft and S&P Global can maintain strong earnings and revenue growth because they have strong competitive advantages.

Yet despite their sustained growth in revenues and earnings, the share prices of many of these companies have declined sharply in recent months.

This is because the market is valuing these earnings at a lower level today, forecasting a decrease in future earnings, or both.

As a result, the unit prices of Montaka’s funds have also declined over the last twelve months.

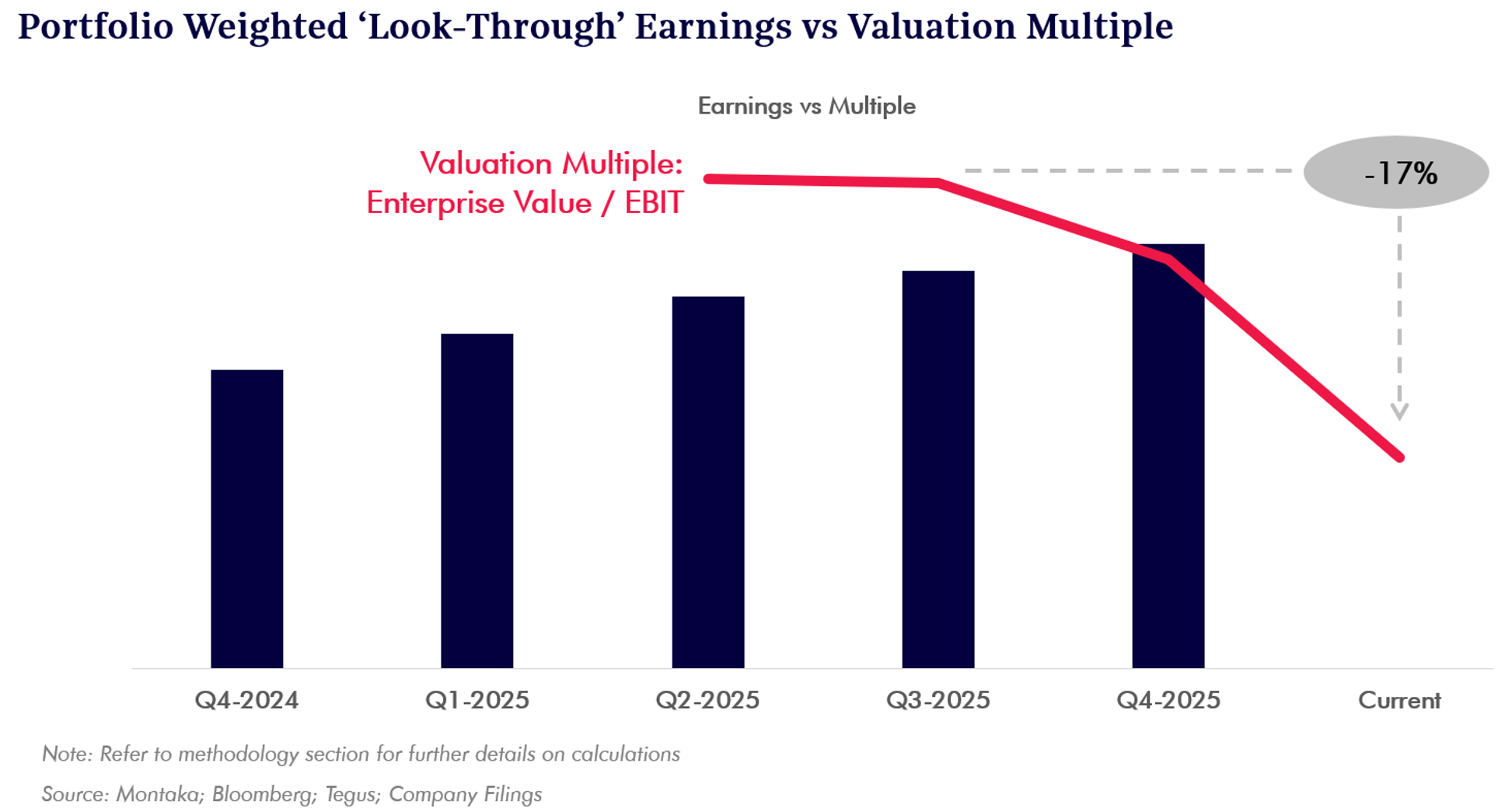

Because earnings of our holdings have grown strongly, whilst their share prices have fallen, the valuation multiple of Montaka’s indicative portfolio weighted look-through earnings has declined by approximately 17%.

This disconnect between value and price represents a unique opportunity.

Competitive advantages on sale

The distinction between price (what you pay) and value (what you get) is at the heart of value investing.

Buying competitively advantaged earnings power at discount prices has long been the name of Warren Buffett’s game.

And Montaka’s too.

Today, when you buy a unit in Montaka’s funds, you are buying what we believe to be some of the world’s most attractive and durable competitive advantages.

But you’re now buying those competitive advantages on sale.

Methodology Note

Analysis based on portfolio weightings of 11% Amazon, 11% Microsoft, 9.5% Meta Platforms, 8.5% Alphabet, 8% KKR, 6% ServiceNow, 6% Tencent, 5.5% Salesforce, 5% Floor & Decor, 4.5% Spotify, 4% Blackstone, 4% S&P Global, 4% Mastercard, 4% MongoDB, 4% DoorDash, 3% Visa, 2% Unity Software

The portfolio weightings have been developed by Montaka to provide an indicative portfolio based on companies held at Jan 2026 publishing quarterly earnings data. The indicative portfolio does not represent actual Montaka portfolio weightings at any point in time during the analysis period. The analysis uses constant portfolio weightings throughout the period. Analysis based on Montaka’s adjusted analysis of each company’s revenue, operating income and enterprise value using company published financial information.

Source: Montaka, Bloomberg, Tegus, Company Filings

[1] Based on Tencent’s 4Q25 results. EBITA represented by Montaka’s assessment of earnings before interest, tax, and amortization.

Andrew Macken is the Chief Investment Officer at Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100 or leave us a line at montaka.com/contact-us

Podcast: Join the Montaka Global Investments team on Spotify as they chat about the market dynamics that shape their investing decisions in Spotlight Series Podcast. Follow along as we share real-time examples and investing tips that govern our stock picks. Click below to listen. Alternatively, click on this link: https://podcasters.spotify.com/pod/show/montaka

Price vs Value: The Best Companies in the World Are on Sale

By Andrew Macken

As Warren Buffett rightly pointed out: “Price is what you pay, while value is what you get.”

The distinction between value and price is one of the most important for an investor to keep in mind. This is particularly true when stock prices – or even unit prices of managed funds – fall.

Montaka’s funds are no exception – unit prices have fallen, driven most substantively by declines in many of the stocks we own, as well as a significant rally in the AUD, which hurts the translation of our global returns in local-currency terms.

But do these price falls reflect declines in the underlying business value of our holdings?

We don’t think so.

As you’ll see in the analysis below, when it comes to revenues and earnings, Montaka’s holdings continue to perform very well fundamentally.

The only change is that in recent months their valuation multiples have significantly derated.

That disconnect – between price (what investors are paying) and performance (what investors are getting) – means that companies with strong competitive advantages are ‘on sale’ today.

Revenues continue to grow strongly

When we calculate a measure of weighted look-through revenues (aggregate revenue adjusted for the size of each investment) of Montaka’s indicative portfolio over time, we see consistent double-digit percentage annual growth, up to and including the most recent quarter.

This was underpinned by consistently strong revenue growth from the likes of Meta, Microsoft, Amazon, Alphabet, ServiceNow, and S&P Global, to name just a few.

Earnings also continue to grow strongly

Similarly, Montaka’s indicative portfolio weighted look-through earnings shows even faster growth.

This relatively faster earnings growth is driven by highly favorable incremental economics.

Incremental profit margins, for example, are the profit margins on the growth in revenues (or how much extra profit the company makes when it sells more), rather than the margin on the company’s existing base of recurring revenues.

When a company’s incremental profit margins hold, the overall operating profit margin will gradually approach this level. The incremental margin works like a ‘magnet’, slowly attracting the average margin towards it over time.

Tencent provides a wonderful case study in incremental economics. In its most recent quarter, which was handed down a couple of weeks ago, the company reported the following:

Tencent has demonstrated it can grow revenues at higher profit margins than its existing revenues.

That’s because most of the incremental revenues have been built on top of the existing (mostly fixed cost) technology platform. So the incremental variable costs required to earn these new revenues are much lower.

This is why profit margins have been expanding. And this is why, with only 13% per annum revenue growth, Tencent was able to grow its operating profits by nearly 40% per annum!

A unique opportunity

Montaka’s holdings, including the likes of Tencent, Meta, Microsoft and S&P Global can maintain strong earnings and revenue growth because they have strong competitive advantages.

Yet despite their sustained growth in revenues and earnings, the share prices of many of these companies have declined sharply in recent months.

This is because the market is valuing these earnings at a lower level today, forecasting a decrease in future earnings, or both.

As a result, the unit prices of Montaka’s funds have also declined over the last twelve months.

Because earnings of our holdings have grown strongly, whilst their share prices have fallen, the valuation multiple of Montaka’s indicative portfolio weighted look-through earnings has declined by approximately 17%.

This disconnect between value and price represents a unique opportunity.

Competitive advantages on sale

The distinction between price (what you pay) and value (what you get) is at the heart of value investing.

Buying competitively advantaged earnings power at discount prices has long been the name of Warren Buffett’s game.

And Montaka’s too.

Today, when you buy a unit in Montaka’s funds, you are buying what we believe to be some of the world’s most attractive and durable competitive advantages.

But you’re now buying those competitive advantages on sale.

Methodology Note

Analysis based on portfolio weightings of 11% Amazon, 11% Microsoft, 9.5% Meta Platforms, 8.5% Alphabet, 8% KKR, 6% ServiceNow, 6% Tencent, 5.5% Salesforce, 5% Floor & Decor, 4.5% Spotify, 4% Blackstone, 4% S&P Global, 4% Mastercard, 4% MongoDB, 4% DoorDash, 3% Visa, 2% Unity Software

The portfolio weightings have been developed by Montaka to provide an indicative portfolio based on companies held at Jan 2026 publishing quarterly earnings data. The indicative portfolio does not represent actual Montaka portfolio weightings at any point in time during the analysis period. The analysis uses constant portfolio weightings throughout the period. Analysis based on Montaka’s adjusted analysis of each company’s revenue, operating income and enterprise value using company published financial information.

Source: Montaka, Bloomberg, Tegus, Company Filings

[1] Based on Tencent’s 4Q25 results. EBITA represented by Montaka’s assessment of earnings before interest, tax, and amortization.

Podcast: Join the Montaka Global Investments team on Spotify as they chat about the market dynamics that shape their investing decisions in Spotlight Series Podcast. Follow along as we share real-time examples and investing tips that govern our stock picks. Click below to listen. Alternatively, click on this link: https://podcasters.spotify.com/pod/show/montaka

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.