|

Getting your Trinity Audio player ready...

|

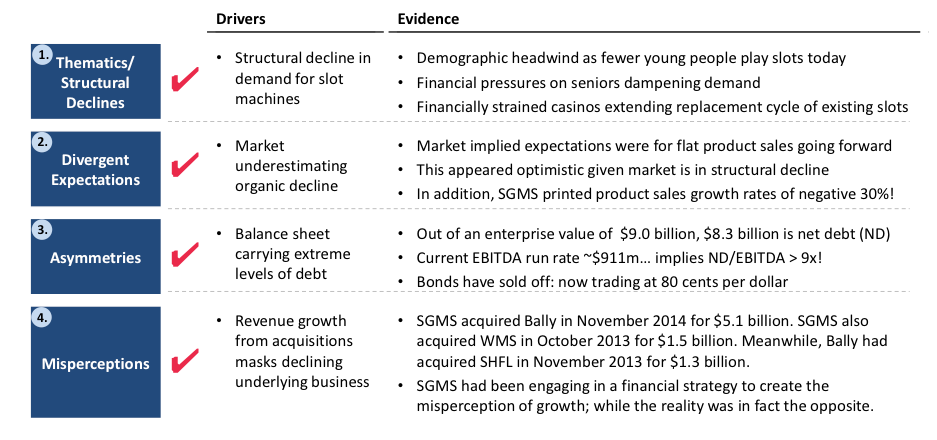

Many readers will by now be aware of Montaka’s short portfolio research framework that was developed over the years by your author. (For a detailed introduction to our research process, click here). There are four specific characteristics of a short that we seek to identify in our research of new potential ideas. These are: (i) long term thematic structural changes; (ii) divergent expectations; (iii) asymmetries; and (iv) misperceptions.

Every stock in Montaka’s short portfolio must exhibit at least one of these four characteristics. Most stocks in Montaka’s short portfolio exhibit two or three of the four characteristics – making them more attractive shorts. Occasionally, we identify an opportunity that ticks all four boxes; and these are the shorts we love the most.

Scientific Games Corporation (NASDAQ: SGMS), the US-based manufacturer of slot machines and other gaming products, has been just this type of short. And in the interests of ongoing investor education, which we care about deeply, we will now illustrate the application of Montaka’s short framework in action on what has been a live portfolio example.

Long term structural decline in demand for slot machines

There is no question demand for slots is in structural decline. This stems primarily from a demographic headwind in the sense that far fewer younger people play slots today than in the past; and the financial pressures on seniors are only increasing.

In a press article last year, US casino owner, Jeff Gural, surmised just this: “Gural said there might be an underlying change in demographics. Saratoga’s racetrack casino was the first in New York, which opened in January 2004. During the past decade, many casino patrons have been retired seniors with good pensions who had the money to wager with. Now many Baby Boomers are retiring without strong pensions, giving them less disposable income than their parents, he said. Also, Gural said people today are more health conscious.”[1]

We can also observe this structural change is the data. Consider that:

- Upon aggregating slot revenue data from Nevada, Atlantic City, Connecticut and Pennsylvania, slot revenue has been in decline since 2007.[2]

- Casinos – as they become more financially strained in the face of intensifying competition across the US – are extending the replacement cycles of slots. This results in lower demand.

Divergent expectations

Following the release of the company’s second quarter results in August, we performed a detailed analysis of the expectations that the market had embedded into the stock’s valuation. On the key value driver of slot machine product sales (which accounted for approximately one third of total sales), the market was implying flat revenues (or zero growth) going forward for the next three years.

Was this a reasonable expectation in light of a market that was in structural decline? We suspected not. This hypothesis was only strengthened in light of the pro-forma slot product sales growth that Scientific Games had just printed in their second quarter results of negative 30 percent! (Yes, not only was the market shrinking, but SGMS was losing market share).

To put this another way, if the current rate of decline continued, market expectations for future revenues were way too optimistic and the company would surely disappoint at subsequent earnings releases. That is, there was a divergence between market expectations and the current reality.

(For what it’s worth, the rate of decline of product sales actually accelerated to negative 33 percent in the company’s third quarter of 2015, released in November; and sales were well below consensus expectations).

Asymmetries

The financial leverage on Scientific Games’ balance sheet can only be described as extreme. Out of an enterprise value of $9.0 billion, $8.3 billion is net debt (with the remaining $0.7 billion the market value of equity). Interestingly, the book value of the company’s equity has been negative for the last three quarters.

Too much debt in a structurally declining business is a nasty combination for a company’s shareholders. The presence of the debt essentially accelerates the rate of decline in value for owners of the business’ equity.

Too much leverage also constrains management’s ability to reinvest in the business at a time it needs it most. The presence of restricting debt covenants and the threat of a tightening credit environment in the US creates an asymmetric risk within Scientific Games’ capital structure.

Misperceptions

It might surprise readers that, for the last eight consecutive quarters, revenue growth at Scientific Games has been north of 40 percent! How can this be if the industry is in structural decline and the company is losing market share? Well, the company has been acquiring competitors to create the illusion of growth.

Of course, acquiring a new business will boost year-on-year growth for the subsequent four quarters; but this growth will revert to underlying organic levels beyond the one year anniversary. So to keep this game going, one needs to keep acquiring new businesses every year. This was the playbook being followed by SGMS (and others in the gaming industry). This charade can continue until excessive financial leverage on the balance sheet prevents additional acquisitions.

Consider that SGMS acquired Bally in November 2014 for $5.1 billion. SGMS also acquired WMS in October 2013 for $1.5 billion. Meanwhile, Bally had acquired SHFL in November 2013 for $1.3 billion.

This is why, in the third quarter of 2015, Scientific Games reported revenue growth of 62 percent, but underlying pro-forma revenue growth (excluding impact of acquisitions) of negative 9 percent. In this sense, the company had been engaging in a financial strategy to create the misperception of growth; while the reality was in fact the opposite.

* * *

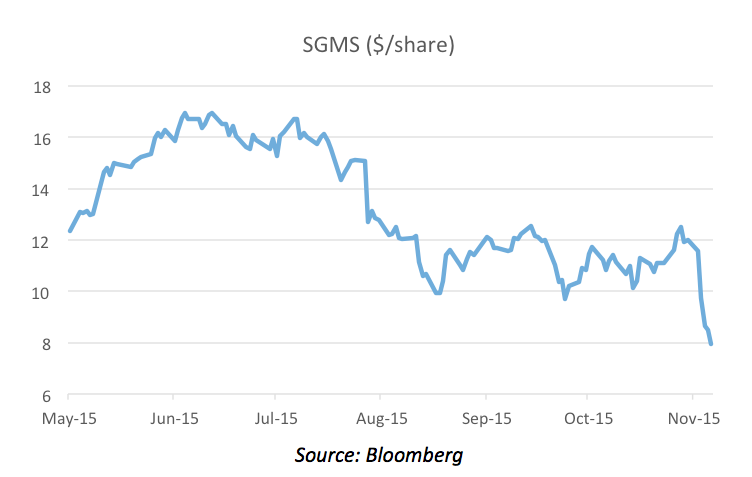

Montaka had been short SGMS since its inception on July 1, 2015. At the writing of this blog, the fund has covered the position given the market cap is now below the fund’s self-imposed size limit. The share price performance of SGMS is illustrated below.

[1] (Saratogian) Casino owner concerned about gaming decline, August 2014

[2] Source: UNLV Center for Gaming Research

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.