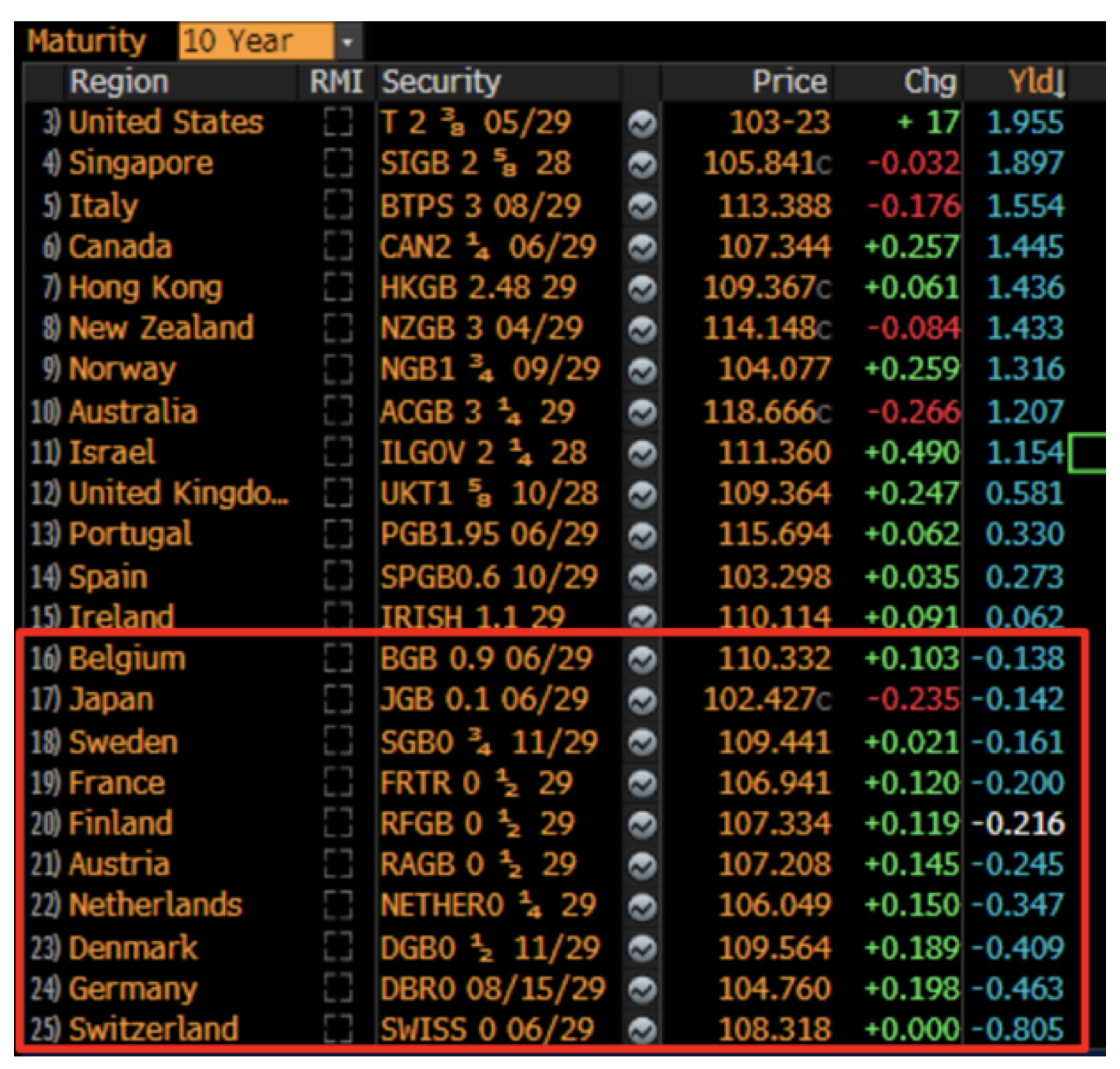

It is well known that interest rates and bond yields are extremely low, so-low in fact that some of the world’s largest countries (Germany, France, Japan) and companies (Apple, Merck, McDonald’s) have NEGATIVE yielding bond. In other words, if you were to lend the German government money for 10 years (i.e. purchase a 10-year Bund) YOU would end up paying ~4.5% for the privilege (Bunds currently yield -0.46%). Furthermore, this is not a unique situation in financial markets at the moment, with 25% of the total $55 trillion worth global debt (sovereign, municipal, corporate, etc.) currently trading with a negative yield, that’s over $14 trillion, it is truly an unprecedented environment in which we find ourselves.

Many Major Economies Have Negative Bond Yields

Given the level of negative yielding bonds in the world one could be forgiven for thinking that investors would be falling over themselves to buy debt with positive yields, particularly if that debt was backed by the largest economy in the world, namely the United States. As we can see from the table above, U.S. 10 year bonds are currently yielding +1.96%, which means over 10 years you’ll be paid an additional ~20% plus 100% of your initial principal versus 0% and 95% of your principal in Germany, sounds like a great deal so why doesn’t every German U.S. treasuries? As the old adage goes, “all that glitters is not gold”. In fact, despite the U.S. having the highest advanced country yields in the world, overseas buyers have dried up and have largely not participated in U.S. treasury auctions in recent times.

Clearly this is a confusing, however it makes more sense when one looks at the source of capital. Specifically, European investors need to invest Euros, Japanese investors Yen, British investors Pounds and Australian investors Australian dollars, etc., etc. When these investors buy foreign bonds they usually need to hedge the currency or any yield advantage may be lost by an unfavourable FX swing and they may have been better off buying their own country’s bonds.

For most of the last decade U.S. treasuries have been extremely attractive for overseas investors, offering positive FX hedged yields across the board (Euro, Yen, Pound, Aussie) which were usually higher than what was on offer domestically, a perfect situation for the U.S. (lots of buyers of its debt). However, starting in December 2016, after prolonged period of ultra-low interest rates, the U.S. Federal reserve started hiking rates aggressively, lifting them by 200 basis points through to December 2018 and flattening the yield curve in the process (the difference between short term and long-term rates). This in turn raised hedging costs and made US treasuries unattractive on a FX hedged basis.

The situation is much clearer if we look at the evolution of FX hedged U.S. treasury yields from the perspective of different investors in different countries. The consistent theme across the world however is that all major currencies and local investor bases (Germany, Japan, Britain, Australia) are better off buying their own government’s debt than that of the U.S. despite having lower yields at home (and in the case of Germany and Japan, negative yields at home are better than the positive yields on offer in the U.S.).

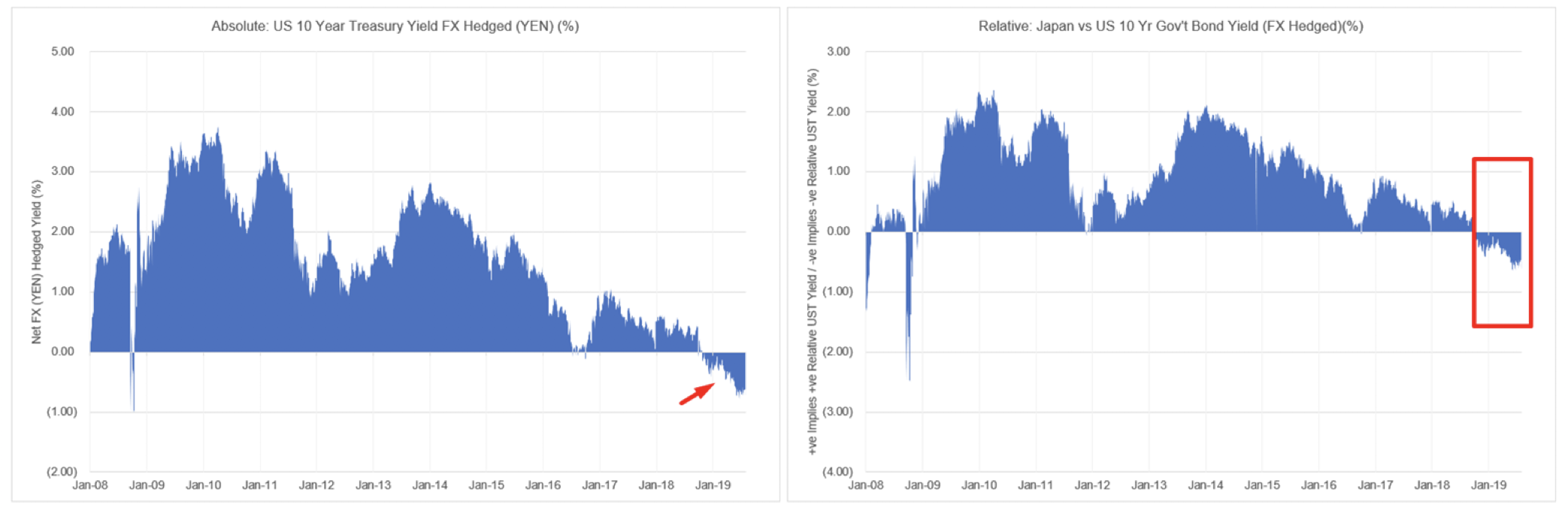

Euro and German Bunds

- European investors have had negative absolute yields on 10 year U.S. Treasuries on an FX adjusted basis since the middle of 2018 (left chart). In fact, despite the Bund being negative, on a relative basis, Europeans have been better off buying 10 year Bunds since early 2017 (right chart), with even better terms on the periphery debt like Portugal, Spain, Ireland, etc. where yields are positive.

Source: Bloomberg, Montaka

Japanese YEN

- Japanese investors have seen negative, absolute US. Treasury yields on an FX hedged basis since the start of October 2018 (left chart), and have been able to get better relative yields domestically ever since (right chart), despite negative yields at home.

Source: Bloomberg, Montaka

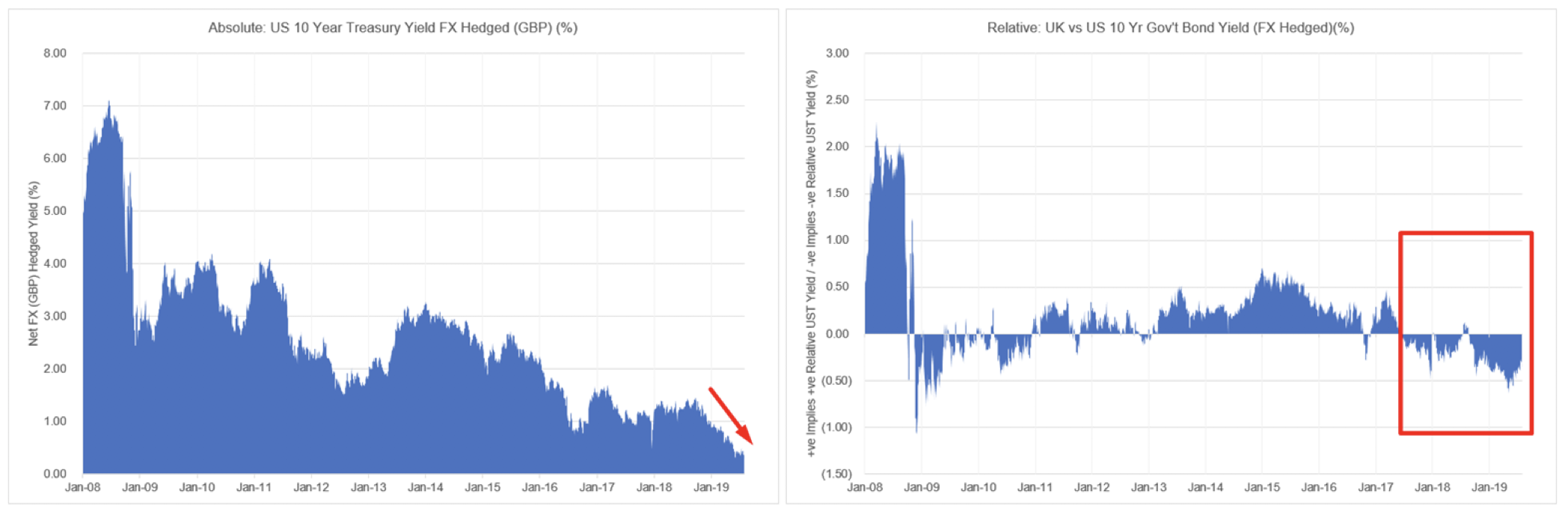

British Pound (GBP)

- While British investors have been able to obtain positive absolute yields on 10 year U.S. Treasuries for the last decade, it has been sharply contracting (left chart) and similar to Europeans, British investors have been getting better yields domestically since mid 2017 (right chart).

Source: Bloomberg, Montaka

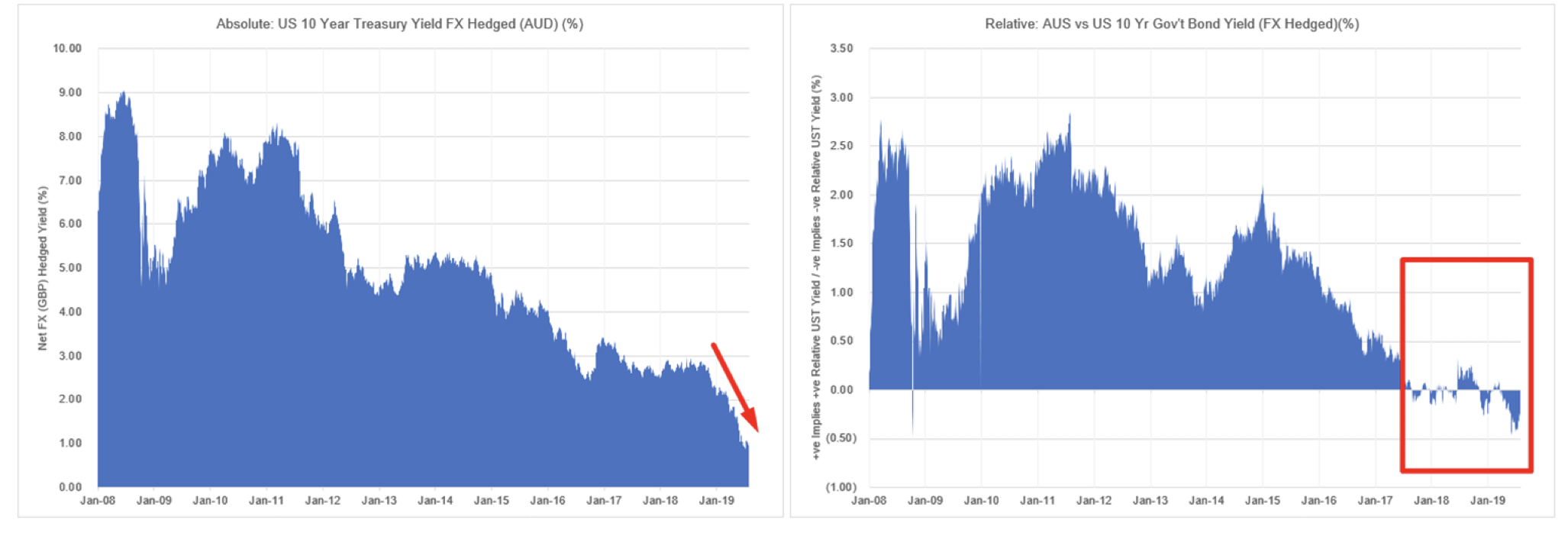

Australian Dollar (AUD)

- Similar to the U.S. Australian investors are able to obtain a positive FX hedged yield in the U.S. over the last decade but again yields have sharply contracted in 2019 (left chart). While Australian government paper currently offers better relative yields on an FX hedged basis, this situation has gyrated back-and-forth over the last couple of years (right chart).

Source: Bloomberg, Montaka

Given it makes little economic sense for most foreign investors to buy U.S. treasuries currently, some still do in order satisfy investment mandates, cross-border trade, hedging activities or simply to place a bet on the U.S. dollar. That said however, the European Central Bank (ECB) and official U.S. data show that since 2017, Eurozone investors have been consistent net sellers of U.S. Treasuries, which has removed an important buyer for U.S. government debt. Given the U.S. government needs ~$1 trillion per year of new buyers to fund its deficits, beyond the existing $22 trillion that is steadily maturing and needing to be refinanced, naturally the question is who buys all of this new debt the U.S. is issuing?

Part of this new buyer universe are U.S. based banks (aka primary dealers). There are 24 primary dealers including JP Morgan. Citigroup, Goldman Sachs, etc., etc. who are required by law to bid in U.S. Treasury auctions when the government is issuing bonds. In fact, the vast majority of U.S. Treasuries the government sells via its auctions (70-80%) end up with primary dealers who then quickly resell them to other investors / buyers through their distribution channels. Since early 2018 however, this trade has not been so straight forward for the primary dealers and increasingly, they have had to hold more and more U.S. Treasuries on their balance sheet (unable to find buyers), with their total holdings increasing four-fold to a whopping $258 billion over the last 12-18 months. The lack of foreign investor demand for U.S. Treasuries is highlighted by the extremely low Treasury auction bid-to-cover ratio, which has now hit its lowest levels in a decade. Since primary dealers are required to bid in the treasury auctions the paper is landing on their balance sheet (as we discussed earlier).

U.S. Primary Dealers Treasury Holdings

Source: Bloomberg

The fact that the U.S. banking system now holds so much more U.S. Treasury paper on its balance sheet, consumes bank capital and removes liquidity from the banking system, something the Federal reserve needs to manage very carefully to avoid tightening credit conditions in the economy unnecessarily (i.e. create a recession environment). So how can the Federal reserve cure this situation in order not to strain the banking system and sap liquidity from the economy? The simple answer would be to weaken the dollar in order to make U.S. Treasuries attractive to overseas buyers again on a FX hedged basis, which would require interest rate cuts (among other things). In fact, the Fed actually cut interest rates for the first time in a decade shortly before this article was written with a 25 basis points reduction on July 31, 2019. Another lever the Fed pulled with its rate cut, was stopping it’s Quantitative Tightening (QT) policy early, which saw $50 billion per month of U.S. Treasuries roll off its balance sheet. This required the market to find a new home for these bonds which given the lack of foreign buyer demand, was placing additional strain on the U.S. banking system (primary dealers), hence the Fed decided to reinvest the proceeds from these $50 billion per month of maturities back into U.S. treasuries, becoming the buyer of these bonds again instead of U.S. banks.

Hopefully we were able to unleaf one of the myriad of complexities that investors find themselves confronted with today by exploring the “yield paradox”, a phenomenon that lays somewhat hidden from general market view.

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Amit Nath is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

The Yield Paradox

It is well known that interest rates and bond yields are extremely low, so-low in fact that some of the world’s largest countries (Germany, France, Japan) and companies (Apple, Merck, McDonald’s) have NEGATIVE yielding bond. In other words, if you were to lend the German government money for 10 years (i.e. purchase a 10-year Bund) YOU would end up paying ~4.5% for the privilege (Bunds currently yield -0.46%). Furthermore, this is not a unique situation in financial markets at the moment, with 25% of the total $55 trillion worth global debt (sovereign, municipal, corporate, etc.) currently trading with a negative yield, that’s over $14 trillion, it is truly an unprecedented environment in which we find ourselves.

Many Major Economies Have Negative Bond Yields

Given the level of negative yielding bonds in the world one could be forgiven for thinking that investors would be falling over themselves to buy debt with positive yields, particularly if that debt was backed by the largest economy in the world, namely the United States. As we can see from the table above, U.S. 10 year bonds are currently yielding +1.96%, which means over 10 years you’ll be paid an additional ~20% plus 100% of your initial principal versus 0% and 95% of your principal in Germany, sounds like a great deal so why doesn’t every German U.S. treasuries? As the old adage goes, “all that glitters is not gold”. In fact, despite the U.S. having the highest advanced country yields in the world, overseas buyers have dried up and have largely not participated in U.S. treasury auctions in recent times.

Clearly this is a confusing, however it makes more sense when one looks at the source of capital. Specifically, European investors need to invest Euros, Japanese investors Yen, British investors Pounds and Australian investors Australian dollars, etc., etc. When these investors buy foreign bonds they usually need to hedge the currency or any yield advantage may be lost by an unfavourable FX swing and they may have been better off buying their own country’s bonds.

For most of the last decade U.S. treasuries have been extremely attractive for overseas investors, offering positive FX hedged yields across the board (Euro, Yen, Pound, Aussie) which were usually higher than what was on offer domestically, a perfect situation for the U.S. (lots of buyers of its debt). However, starting in December 2016, after prolonged period of ultra-low interest rates, the U.S. Federal reserve started hiking rates aggressively, lifting them by 200 basis points through to December 2018 and flattening the yield curve in the process (the difference between short term and long-term rates). This in turn raised hedging costs and made US treasuries unattractive on a FX hedged basis.

The situation is much clearer if we look at the evolution of FX hedged U.S. treasury yields from the perspective of different investors in different countries. The consistent theme across the world however is that all major currencies and local investor bases (Germany, Japan, Britain, Australia) are better off buying their own government’s debt than that of the U.S. despite having lower yields at home (and in the case of Germany and Japan, negative yields at home are better than the positive yields on offer in the U.S.).

Euro and German Bunds

Source: Bloomberg, Montaka

Japanese YEN

Source: Bloomberg, Montaka

British Pound (GBP)

Source: Bloomberg, Montaka

Australian Dollar (AUD)

Source: Bloomberg, Montaka

Given it makes little economic sense for most foreign investors to buy U.S. treasuries currently, some still do in order satisfy investment mandates, cross-border trade, hedging activities or simply to place a bet on the U.S. dollar. That said however, the European Central Bank (ECB) and official U.S. data show that since 2017, Eurozone investors have been consistent net sellers of U.S. Treasuries, which has removed an important buyer for U.S. government debt. Given the U.S. government needs ~$1 trillion per year of new buyers to fund its deficits, beyond the existing $22 trillion that is steadily maturing and needing to be refinanced, naturally the question is who buys all of this new debt the U.S. is issuing?

Part of this new buyer universe are U.S. based banks (aka primary dealers). There are 24 primary dealers including JP Morgan. Citigroup, Goldman Sachs, etc., etc. who are required by law to bid in U.S. Treasury auctions when the government is issuing bonds. In fact, the vast majority of U.S. Treasuries the government sells via its auctions (70-80%) end up with primary dealers who then quickly resell them to other investors / buyers through their distribution channels. Since early 2018 however, this trade has not been so straight forward for the primary dealers and increasingly, they have had to hold more and more U.S. Treasuries on their balance sheet (unable to find buyers), with their total holdings increasing four-fold to a whopping $258 billion over the last 12-18 months. The lack of foreign investor demand for U.S. Treasuries is highlighted by the extremely low Treasury auction bid-to-cover ratio, which has now hit its lowest levels in a decade. Since primary dealers are required to bid in the treasury auctions the paper is landing on their balance sheet (as we discussed earlier).

U.S. Primary Dealers Treasury Holdings

Source: Bloomberg

The fact that the U.S. banking system now holds so much more U.S. Treasury paper on its balance sheet, consumes bank capital and removes liquidity from the banking system, something the Federal reserve needs to manage very carefully to avoid tightening credit conditions in the economy unnecessarily (i.e. create a recession environment). So how can the Federal reserve cure this situation in order not to strain the banking system and sap liquidity from the economy? The simple answer would be to weaken the dollar in order to make U.S. Treasuries attractive to overseas buyers again on a FX hedged basis, which would require interest rate cuts (among other things). In fact, the Fed actually cut interest rates for the first time in a decade shortly before this article was written with a 25 basis points reduction on July 31, 2019. Another lever the Fed pulled with its rate cut, was stopping it’s Quantitative Tightening (QT) policy early, which saw $50 billion per month of U.S. Treasuries roll off its balance sheet. This required the market to find a new home for these bonds which given the lack of foreign buyer demand, was placing additional strain on the U.S. banking system (primary dealers), hence the Fed decided to reinvest the proceeds from these $50 billion per month of maturities back into U.S. treasuries, becoming the buyer of these bonds again instead of U.S. banks.

Hopefully we were able to unleaf one of the myriad of complexities that investors find themselves confronted with today by exploring the “yield paradox”, a phenomenon that lays somewhat hidden from general market view.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

The Yield Paradox

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.