|

Getting your Trinity Audio player ready...

|

Last week, 51job (Nasdaq: JOBS), the Chinese online job ad platform, reported its third quarter 2018 earnings result. The result was very strong, and given that the stock has been beaten up by the market over the last few months, one would expect that the stock would rally as a result. However, somewhat surprisingly, 51job stock ended the post-result trading session down 1%. We will dissect the result and attempt to make sense of the puzzling market reaction.

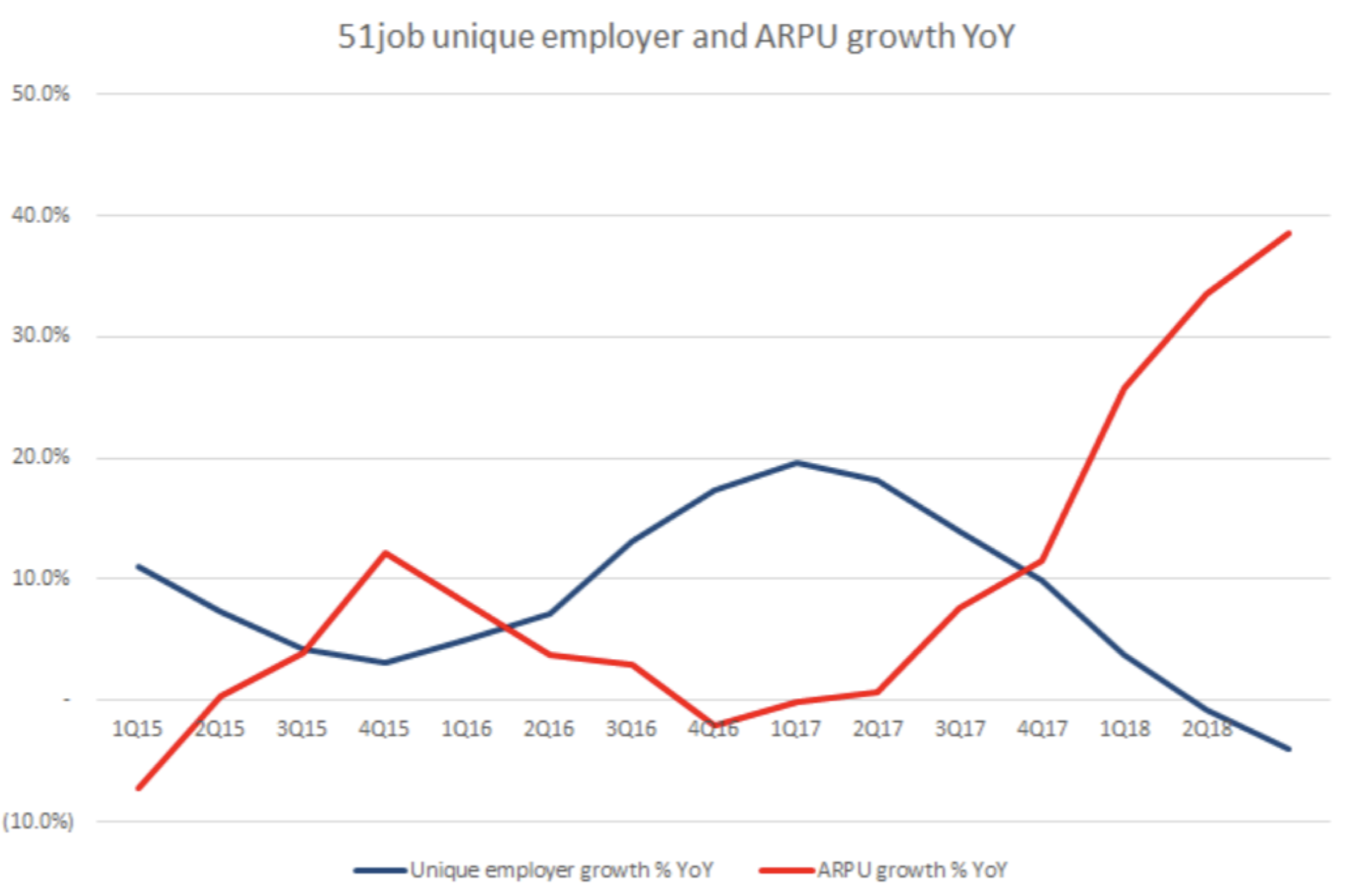

JOBS managed to grow revenues by an impressive 31% year-over-year (YoY) in Q3, with the company’s online recruitment revenues –that is, the portion of revenues that come from online job ads and related online products and services –growing by 33% YoY. Online recruitment revenues were driven by a very impressive 38.6% YoY increase in the average revenue per employer, with the growth rate accelerating compared to preceding quarters.

Source: Company data; MGI

This strong top-line growth translated into solid earnings growth, with operating income increasing by 34.6% YoY, and fully diluted adjusted EPS rising by 53% YoY. There are few businesses out there that are capable of even achieving this level of growth. So what’s driving the persistently weak stock price? We believe the reasons for the weakness in JOBS’s share price can be segmented into two categories: fundamental factors, and non-fundamental factors.

Fundamental factors relate to developments in the underlying business, and in the case of JOBS, investor concern over potential fallout from the U.S. and China trade tensions is likely to be contributing to recent stock price negativity. The mechanics behind how this trade dispute impacts 51job are as follows: (i) trade tensions have led to tariffs, which reduce trade flows between China and the U.S.; (ii) as certain products imported into the U.S. from China are now more expensive under this tariff regime, this leads to lower aggregate demand for Chinese goods; (iii) this can potentially translate into reduced hiring activity if less workers are needed to support this lower level of aggregate demand; and (iv) any reduction in hiring activity would mean a lower volume of job ads are posted on 51job’s platform, reducing the company’s revenues.

Concerns about fallout from the U.S./China trade spat are valid, and we share these same concerns. However, with any equity security you are paying a price; and embedded in that price are a set of assumptions for growth and margins. When 51job reached its nadir of $52/sh in late October, what were the set of assumptions we needed to believe to justify that share price?

- Revenues

- The $52/sh price implied revenues would need to grow at around 5% going forward. This is wildly conservative, given the secular tailwinds that are observable in the Chinese online job ad market: (i) only 6% of small and medium enterprises (SMEs) in China recruit online, with a long runway for 51job to capture a greater share of recruitment budgets; (ii) rising internet penetration on China; (iii) continued strong economic growth in China of around 6.5%; and (iv) a white-collar worker shortage, which plays into 51job’s strengths of alleviating labour market frictions.

- Given 51job is one of the leading recruitment platforms in China, and that we view it as highly unlikely that the above structural factors will abate in the short to medium-term, it seems implausible that 51job should be expected to grow below Chinese GDP growth going forward.

- Gross margins

- One needed to believe gross margins would remain flat at 73% for the rest of time. With the potential to raise prices over time, and our expectation for much higher rates of revenue growth than are being implied by the market, we believe that there is room for gross margin expansion. In other words, the expectation for gross margins to remain flat was too conservative.

- Operating earnings

- At $52/sh, the market was expecting earnings growth of less than 5%. We view this as unhinged from reality. For some context, 51job managed to grow earnings by 42% YoY in FY17. With our view that revenues should grow strongly in the future, we believe it is highly likely that 51job will be able to achieve operating leverage, particularly on its general and administrative expenses which are unlikely to grow as fast as revenues.

On a view that considers purely the fundamentals, 51job is demonstrably cheap. However, as was alluded to above, there are non-fundamental factors that can whipsaw a share price, and these can be especially difficult to identify before they are set in motion. The Montaka team is of the belief that non-fundamental factors are playing a prominent role in depressing 51job’s share price.

We have witnessed outflows from many exchange-traded funds (ETFs) that hold JOBS, precipitating indiscriminate selling of JOBS as these ETFs have to sell to meet redemptions. Said another way, there is selling activity occurring that is decoupled from, and ignorant of the fundamentals of 51job. Exacerbating this is the relative illiquidity of JOBS, and the difficulty in absorbing sell orders arising from these ETF outflows, putting downward pressure on the share price. My colleague Chris Demasi has previously written on this topic.

Over time, non-fundamental trading activity should wash out, and we invest on the premise that longer term the growth in a company’s stock price should mirror the fundamentals of the underlying business. We took the opportunity to add to our 51job position significantly before the Q3 2018 earnings result. The stock is currently up around 9% from its post-result stock price close, and is now up over 30% from its 52-week low in late October. We continue to believe 51job is very cheap, and we await an environment where fundamentals take over, and once again become the key driver of stock prices.

Montaka owns shares in 51job (Nasdaq: JOBS)

![]()

George Hadjia is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.