|

Getting your Trinity Audio player ready...

|

As Benjamin Graham, widely known as “the father of value investing”, understood well, stock prices can bounce around for a range of different reasons, and any of them may have very little to do with the fundamental prospects, earnings and cash flows that the underlying business will ultimately generate for its owners (shareholders) over time. In the longer term, however, share prices tend to converge towards a path crafted by the intrinsic value of the business. In the meantime, emotion, sentiment, second-guessing, and poor understanding often cause share prices to deviate from this course, creating opportunities for outsized profits for the patient, value-oriented investor.

“In the short run, the market is a voting machine but in the long run, it is a weighing machine” Benjamin Graham

Over the past few months, we believe we have observed this dynamic at play with the stock of 51job (NYSE: JOBS). 51job is the leading online job search portal in China, performing a similar role in the world’s most populous nation as seek.com.au does here in Australia. 51job is benefitting from the secular shift from offline to online advertising, which has driven annual revenue growth from the teens two years ago, to more than 30% recently. Over this period, the stock price had performed similarly impressively, until a couple months ago.

Share price performance over the last two years for 51job

In roughly 21 months to the beginning of June this year the 51job share price had more than tripled. But since then the stock has seen constant selling pressure and has pulled back by 37% from its peak. At the same time, we believe the potential for 51job to grow its sales, expand margins, and generate increasing levels of cash flow for the benefit of its shareholders is unchanged. In other words, the intrinsic value of the business has not changed. So, what could be pulling the stock price down when the business is doing so well? We’ve made a few observations that I will share in the article, none of which impair the ability of 51job to earn profits over time, but which may impress on the market price of the stock in the meantime.

ETF Flows

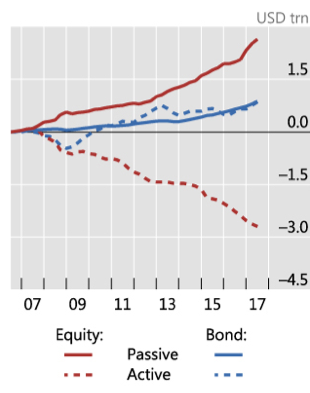

The rise of passive investing has been well documented across the globe and across asset classes. The Bank for International Settlements estimates that passive funds now account for around one dollar in every three dollars invested in equities globally. In the US, this share is closer to 45%.

Cumulative fund flows for equities and bonds worldwide

Source: Bank for International Settlements

Broadly speaking, passive funds including exchange-traded funds (ETFs) are price-indiscriminate buyers and sellers of securities. As money flows in they allocate funds to securities in proportion to their weighting in the relevant index and buy accordingly. The inverse is true when money flows out and funds sell regardless of the prospects of the businesses and the value of the stocks held in the portfolio.

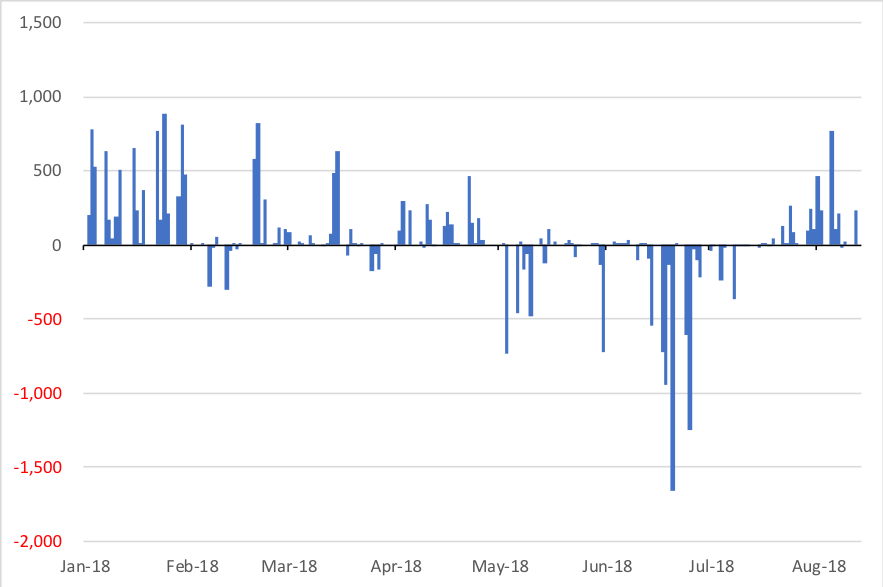

Interestingly, when it comes to 51job this later scenario may be playing out. We analysed fund flows into and out of the top ETF shareholders of the 51job stock for the current year to date and found that the start of the share price retracement coincided with the start of a several-month period of constant and increasing outflows for these ETFs. From the end of May this group of ETFs began to see net redemptions, which increased in size through to mid-July and remained negative up until a few weeks ago.

Fund flows into and out of the top 10 ETF shareholders of 51job in 2018

Source: Montaka

While stock markets are complex beasts with numerous drivers intertwined and at play, we would not dismiss the link between the share price and fund flows as simply coincidental.

Liquidity

For large companies that can see billions of dollars of stock change hands in a day (as a small aside Apple traded $4 billion of stock yesterday), the impact of ETF redemptions may be easily absorbed by the natural liquidity provide by buyers in the marketplace. For smaller or less liquid stocks this may not be the case.

51job has a market capitalisation of around US$4 billion (this was closer to US$7 billion at its peak share price in June), of which around half is available to be traded as free float, and trades about US$7 million of stock on average each day. By many standards these metrics represent a stock with relatively lower liquidity, especially when compared with the large companies of the S&P500 (or Apple!)

When stocks like 51job with less available liquidity meet outflows from price insensitive ETF sellers, it is easy to see that the share price will continue to be pressured as long as the selling persists. What we are saying is that lower liquidity means it is difficult in the near term to find new buyers for a stock as those buyers with outstanding orders are filled when a constant flow of sell orders occurs. The result is a falling (sometimes gapping) share price to draw in new buyers to pick up the stock and clear the market. And none of it depends on how much cash 51job will generate this year, next year or for the next decade.

Changing business model

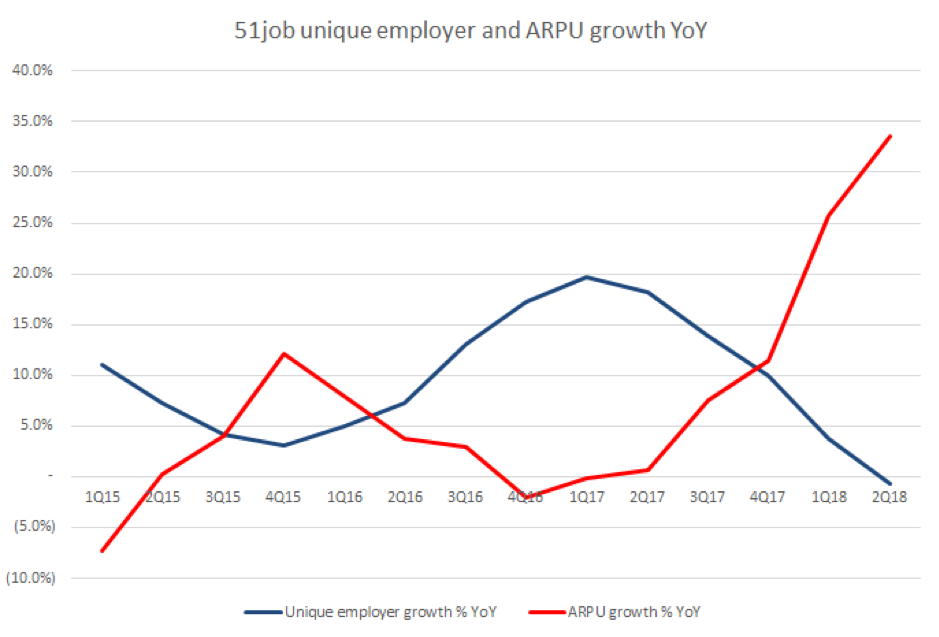

Unfortunately for the 51job stock, at the very time that flows into its shareholder funds reversed to positive numbers, management reported a quarterly result that reflected an augmentation of the business model that investors had become accustomed to.

At the beginning of August 51job reported financial results for its second fiscal quarter. Revenue growth was fantastic, up 33% compared to the year-ago period, and management guided to 24-28% growth in the next quarter – a moderation but still incredibly high. Expense growth, however, was also high. Specifically, costs related to sales and marketing (S&M) grew 46% and took a larger share of sales than ever before.

On a short-run view this increase in S&M costs would simply equate to lower profitability, and therefore a lower company valuation, which would in turn lead to a sell-off in the stock. Indeed, this is what has happened.

Taking a longer-term view of the development of the business, we view the S&M ramp as an investment rather than a cost. As such we expect a return for shareholders on the money spent to promote the 51job platform and products. Management intend to use the money to hire additional sales people ahead of the curve, reward top performers, penetrate existing accounts deeper and build the brand. As this occurs over time, 51job should reap benefits from higher value customers spending more on more 51job products and services, without the need to disproportionately increase costs to support this growth. This is already being reflected in an accelerating ARPU (average revenue per user) even as the number of employers using the portal remains resilient.

It is reasonable that 51job will make more money over the next five, ten, or more years than had been expected before. But of course, this is not how the market perceived the result, and therein lies the opportunity.

Buying more on weakness

Stock investments held by the Montaka funds are selected based on the quality of the business and discount to intrinsic value being offered by the market. If earnings power and cash flow generation potential over a multi-year horizon remain intact we would assess intrinsic value to be unchanged regardless of the reverberations or retracements the share price may experience in a short period of time.

Moreover, any downward pressure on the share price that could be caused by supply/demand imbalances from fund flows; low liquidity inherent to lower capitalised or tightly held companies; or, negative sentiment reflecting short term profit impacts of value-enhancing decisions made by management, is more likely to be viewed as an opportunity rather than a risk or a loss.

We believe the combination of these dynamics have presented us with an opportunity to increase the Montaka funds’ holding in 51job, the out-sized benefits of which will play out for our clients in time.

![]() Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.