|

Getting your Trinity Audio player ready...

|

The affordability of U.S. healthcare frequently makes headlines in the news, and for a good reason. In 2013, the U.S. spent an incredible 17.4% of GDP on healthcare, the highest among high income nations. The issues for many Americans requiring healthcare are two-fold: affordability and access.

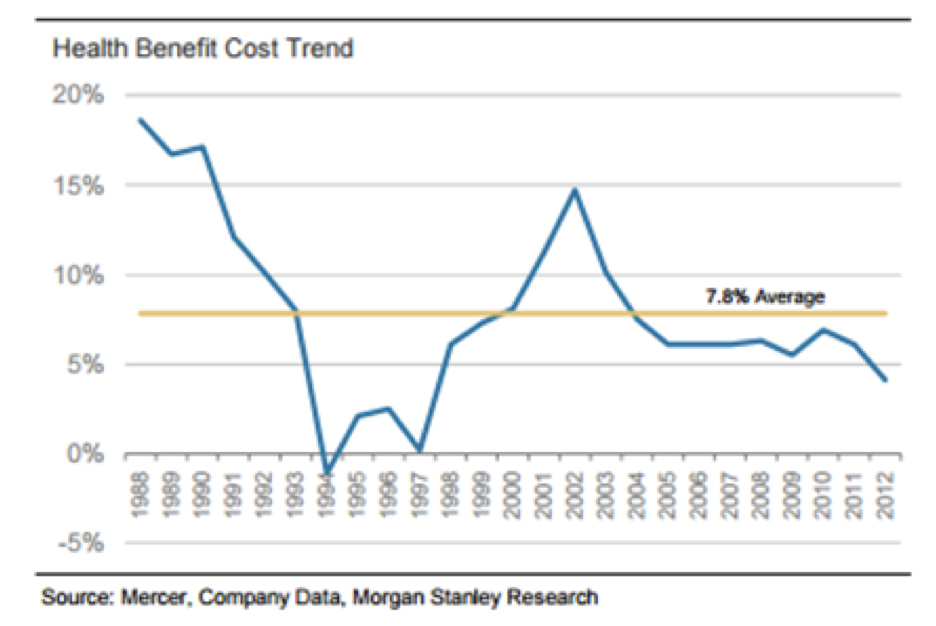

Healthcare costs in the U.S. have become unaffordable for a large number of Americans, driven in large part by the circa 8% average annual growth rate of medical costs over the last 25 years.

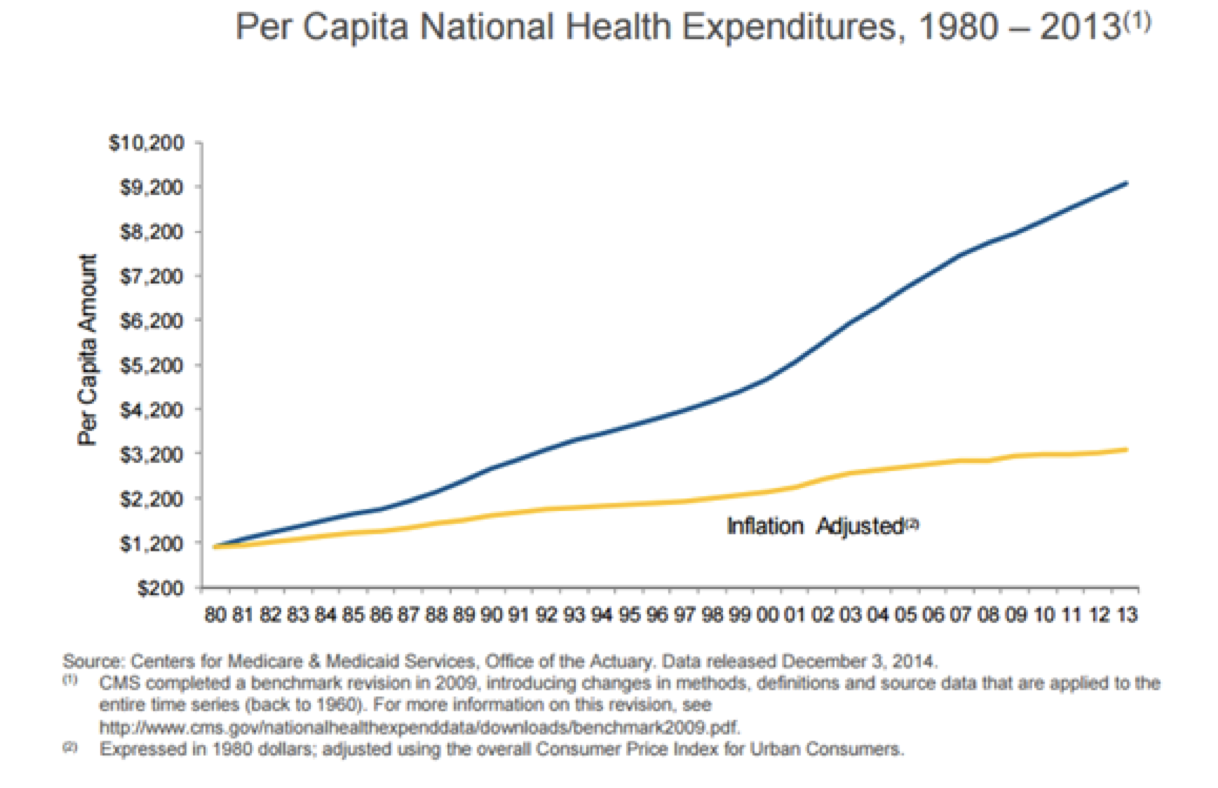

Per capita national healthcare expenditures have risen inexorably, significantly overshooting inflation. Wages growth has struggled to keep up with run-away medical cost inflation, exacerbating this issue of unaffordability.

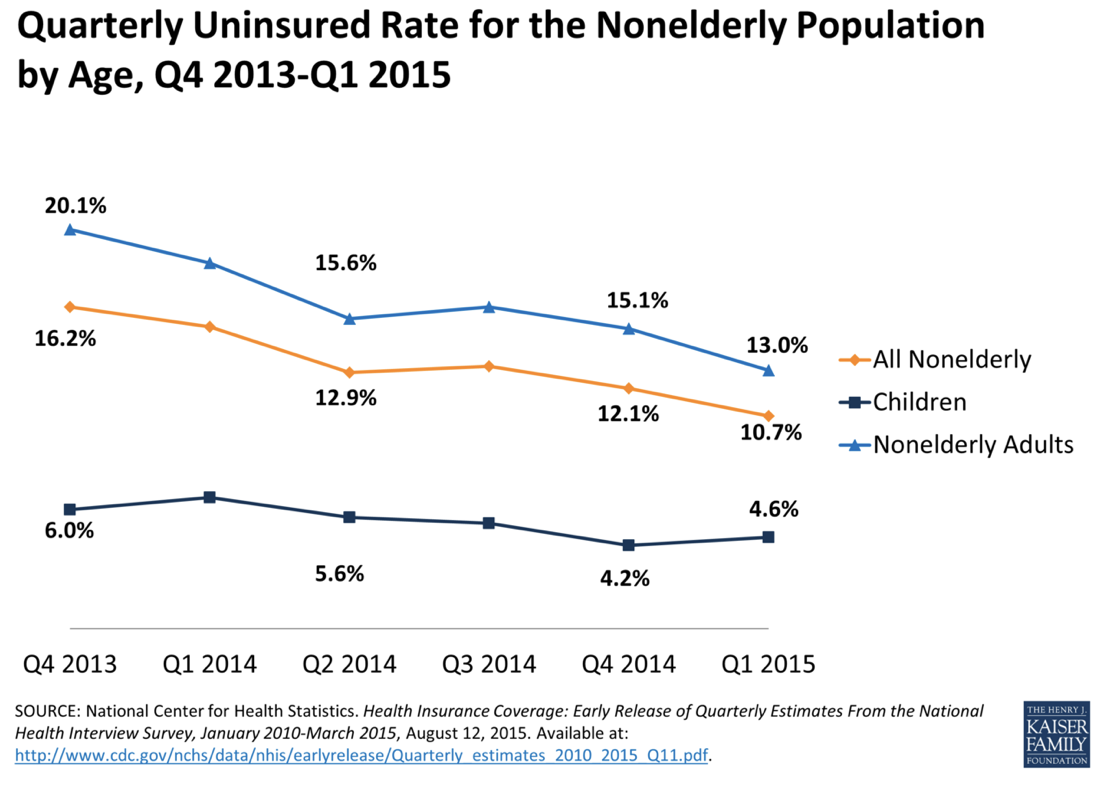

A 2014 Kaiser survey revealed that cost is a major barrier to coverage for the uninsured, with 48% of uninsured adults citing the main reason for no healthcare coverage was that it was too expensive. Furthermore, 12% of Americans cited eligibility as a barrier to gaining access to healthcare, whether due to being unemployed or not having an offer for healthcare through their employer.

The introduction of the Patient Protection and Affordable Care Act in 2010, colloquially known as Obamacare, was the most significant healthcare reform since the passage of Medicare and Medicaid in 1965. The overarching goal of Obamacare is to improve the quality and affordability of healthcare in the U.S., as well as reduce the uninsured population of Americans; in effect the comprehensive reforms of Obamacare seek to specifically address many of the abovementioned affordability and access issues that plague the U.S. healthcare system.

Our belief is that a number of firms are well-positioned to benefit from the changes that will transpire from Obamacare, as well as broader trends that will impact the U.S. healthcare industry.

More Insured Americans

Obamacare has vastly improved access to healthcare and has increased the number of insured Americans, expanding the insurable universe of individuals for healthcare insurers such as Aetna. The creation of what are called Health Benefit Exchanges has led to previously uninsured Americans purchasing health insurance. Through these health insurance exchanges, Americans now have guaranteed access to health insurance, regardless of employment status or pre-existing medical conditions which may have caused insurers to deny them coverage under the previous system.

Despite difficulties with correctly pricing these health exchange plans in light of limited claims experience, these exchanges provide a new channel to add insured lives and are expected to contribute to the profitability of insurers so long as the risks are priced appropriately.

The Need for Greater Cost Control Amid Healthcare Utilization Increases

In the U.S., approximately 10,000 people turn 65 everyday, requiring greater utilization of healthcare services and prescription medication as they age. This is a great secular tailwind for a company such as a CVS which has retail and mail-order pharmacy businesses that sell prescription medication.

In light of this higher utilization of healthcare products and services from an aging population, it is crucial to limit the ability of drug manufacturers to pass through rampant drug price increases. CVS, in addition to its retail pharmacy business, has a pharmacy benefits manager (PBM) asset which seeks to address this issue. Acting on behalf of health plan clients (i.e., insurers and employers), the CVS/caremark PBM has sufficient scale to extract cost savings when purchasing drugs from pharmaceutical manufacturers.

CVS’s PBM also maintains a formulary, a schedule which specifies the drugs that insurers are willing to reimburse. A pharmaceutical company attempting to achieve egregious price increases on a drug risks the exclusion of that particular drug from the formulary, a disastrous outcome given that demand for most medications relies heavily on the cost being reimbursed by an insurer. It is clear that CVS acts as a shield for insurers against unrestrained medical cost trend and is a key part of the solution to improve the affordability of healthcare which the Affordable Care Act legislation seeks to achieve.

Shift to Value-Based Care

A key trend, and a vital component of Obamacare’s desire to improve the quality and affordability of healthcare, is the shift towards value-based care, whereby providers of healthcare (i.e., hospitals and physicians) are rewarded based on providing a quality outcome for the patient rather than on the quantity of services provided.

In order to effect the transition to a value-based system, health insurers need sufficient scale to pressure the providers into agreeing to value-based contracts. Aetna, a holding in the Montaka Global Fund, is merging with Humana, another large health insurer. Barring any regulatory holdups, the merger will create a health insurance behemoth that will have the scale to push for greater cost accountability amongst the healthcare providers.

The healthcare value chain is complex and not all participants will benefit equally from the changes that are underway. Despite outlining industry-level changes that will affect the U.S. healthcare system, the Montaka team will always select stocks using a bottom-up approach; for a stock to be included in the Montaka portfolio as a long position, it must have merit based on its track record of producing above-normal returns on invested capital, as well as having a strong and defensible industry position. We believe that Aetna and CVS both meet this standard. Nevertheless, even amid monumental changes to the U.S. healthcare industry, we gain comfort in knowing that both Aetna and CVS are well-positioned to benefit from these changes and continue to play an integral part in improving the quality and affordability of healthcare in the U.S.

Montaka owns shares in CVS and Aetna.

![]() George Hadjia is a Research Analyst with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

George Hadjia is a Research Analyst with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.