|

Getting your Trinity Audio player ready...

|

Don’t worry, this is not a discussion about hedge fund fees. This is a discussion about management incentives. We were recently asked an astute question by an allocator around the extent to which we examine management’s economic incentives in the businesses we buy and sell. The answer is that they matter a great deal and we examine these closely as part of our research process.

Economic incentives really do drive human behaviour – and if management’s incentives are not aligned with those of shareholders, then shareholders should not really be surprised if management does not behave in a shareholder-friendly way. One current example that highlights precisely this dynamic relates to Hanesbrands (NYSE: HBI), which resides in Montaka’s short portfolio.

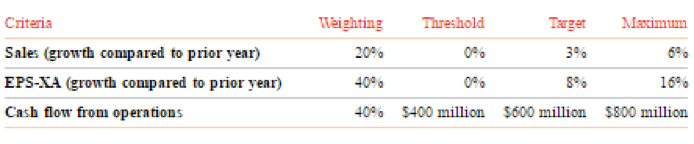

Consider the following table which details the key criteria which drives the awarding of management’s long-term incentive awards. What do you notice? Management will be rewarded for growth in sales, growth in earnings-per-share and growth in cash flow from operations. Is this a sensible incentive structure?

Source: Hanesbrands 2016 Proxy Statement filed with SEC

What ultimately drives value in a business is its ability to earn high returns on incremental invested capital. Note that this is a ratio: it is not about just growing sales or earnings; it is about growing earnings at a faster rate than invested capital. But the criteria in the table above provide no rewards or penalties for the management (or mismanagement) of the denominator: capital.

So as you might now expect, Hanesbrand’s management has been on an acquisition spree for many years. The following highlights some of the major recent acquisitions which have created the perception of growth in the business:

- October 2013: Maidenform Brands Inc for $581m;

- August 2014: DBA Lux Holding S.A. for $392m;

- April 2015: Knights Holdco, Inc for $193m;

- June 2016: Champion Europe S.p.A. for $245m; and, most recently

- July 2016: Pacific Brands for approximately $800m.

It is, therefore, no surprise that, on the company’s most recent conference call, CEO Gerald Evans touted the company’s: “11% increase in revenue, a 12% increase in earnings per share and a record level of cash flow from operations…” After all, to him, what else matters?

For shareholders, on the other hand, they ultimately have to pay for these acquisitions via reduced dividends and company share repurchases. So while cash from operations (CFFO) might be growing strongly, free cash flow – after capex and acquisitions – has been suffering recently. This is illustrated by the table below (amounts are in $000s).

Source: Company Filings; MGIM

Furthermore, we believe investors have been blindsided by the growth that has been created by acquisitions; and are failing to appreciate the decline in the underlying core business, as illustrated below.

Source: Company Filings; MGIM

So while management are delivering well on their targets, these targets are not delivering well for shareholders. This is evident by the recent performance of Hanesbrands’ stock price. And this is precisely why management incentives matter.

Montaka is short the shares of Hanesbrands (NYSE: HBI).

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.