|

Getting your Trinity Audio player ready...

|

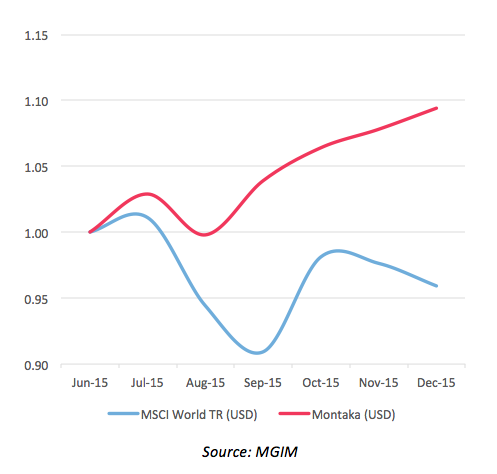

At Montaka, we are delighted to have delivered our early investors a great start. Since we launched on July 1, 2015, Montaka has delivered substantial positive returns against a global market which turned negative over the same period.

This is illustrated in the chart below which shows Montaka’s returns over the six month period to December 31, 2015, relative to the global market. We illustrate the returns here in US dollar terms. (Australian investors will be used to seeing Montaka’s returns in Australian dollar terms, so the numbers will not match).

As shown, over the initial six month period of the Fund’s life, Montaka added +9.4 percent against a market that fell by 4.1 percent. This equates to +13.5 percent outperformance over the six month period.

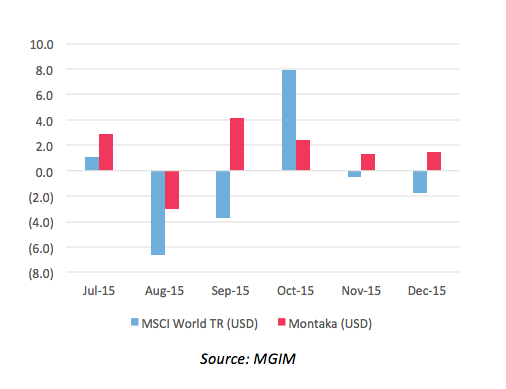

In addition to headline returns, investors should seek to understand the nature of their return profile as well as the attributions of their returns.

Consider the chart below which illustrates the monthly returns delivered by Montaka over its initial six month period, versus the global market. The key point here is that returns are not very correlated with the market. Indeed, over this six month period, the correlation between Montaka’s returns and the market was less than 50 percent. (Interestingly, Montaka’s returns with its global hedge fund peer group was also less than 50 percent). In this business, it is good to be different – only then will meaningful diversification benefits accrue to our clients’ portfolios.

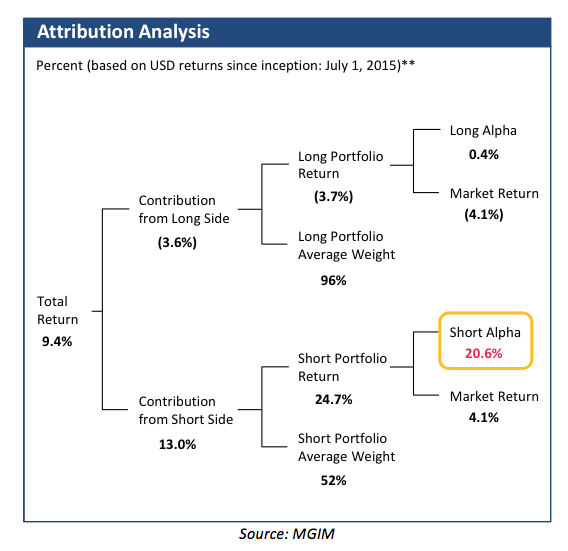

Finally, it is important to understand where and how your Investment Manager is adding value. Consider the tree-diagram below which dissects Montaka’s 9.4 percent return into its components. Investors should ultimately be interested in the level of “value-add” over and above the market return, or “alpha”, generated by the manager in both the long and the short portfolios; as well as the relative sizes of those portfolios.

As the chart below illustrates, substantially all of the “value-add” generated by the Montaka portfolio has stemmed from the short portfolio. This is an extremely scarce characteristic in the market place; and one that is highly valuable in the current market environment.

The above attribution analysis reiterates a key aspect of Montaka’s value proposition. Montaka’s short portfolio is not just an “insurance policy” for the long portfolio should markets turn down. It is its own value-generator which stems from the disciplined application of Montaka’s unique short-side research process.

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.