|

Getting your Trinity Audio player ready...

|

Would you like to own a business that owns little else but 41,000 kiosks that distribute rental DVDs from over 33,000 locations across the United States? While this business model may have made sense in the past, it makes little sense these days. It is so cheap and convenient these days for consumers to stream Netflix or a movie on Apple TV, that consumer demand for DVDs is in structural decline.

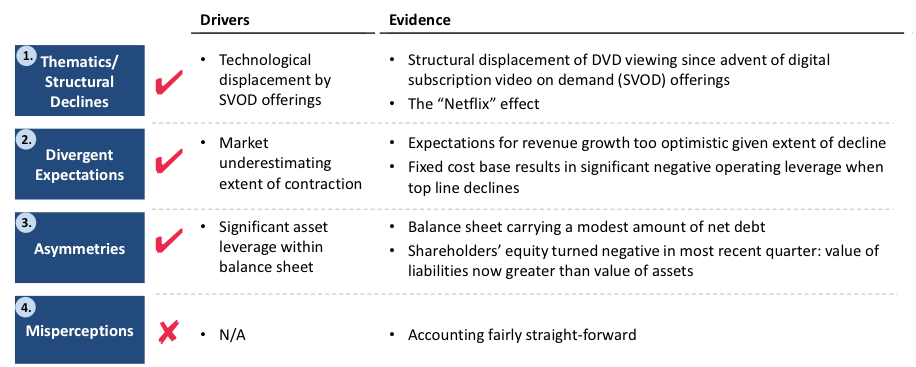

The business is called Outerwall (NASDAQ: OUTR), and we have been negative on its prospects since Montaka’s inception on July 1. As illustrated below, Outerwall ticks three of the four categories that we look for in attractive shorts.

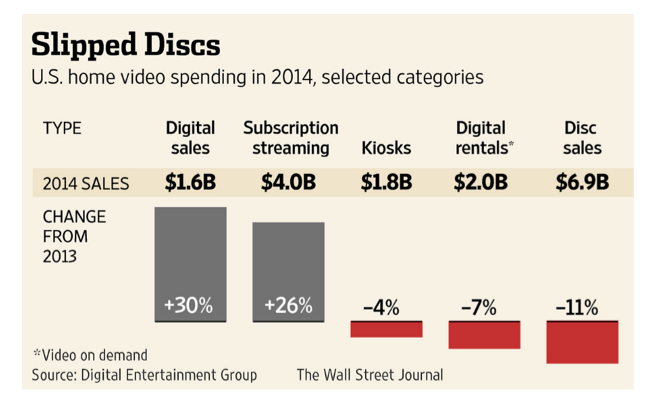

As illustrated in a Wall Street Journal article this year[1], demand for kiosks and discs declined in 2014. Growth in subscription streaming and digitals sales, on the other hand, was off the chart! These outcomes reflect a structural change in consumer behaviour – a trend which is unlikely to change any time soon.

In addition to the structural decline in demand for DVDs described above, market expectations for Outerwall’s revenue has remained at levels that we believe are far too optimistic given the reality of the situation.

Throughout this year, revenue growth expectations have remained at approximately zero for 2015 and 2016. That is, revenues will remain flat, rather than decline. Consider, therefore, the company’s reported third quarter revenue growth of negative 7 percent year-on-year. This was clearly below expectations – but the situation was actually far worse.

You see, in late 2014, Outerwall announced significant price increases to its DVD rentals in the order of +25% percent. (Of course, a few weeks later, the CEO quit, the company’s board declared its first dividend and announced a $400 million share buyback. These are all red flags that suggest all is not well inside the business). So if third quarter revenue is down 7 percent year-on-year, but the prior period comparison does not include the massive price increase, then underlying sales growth (excluding the price rise) could be down as much as 30 percent!

Outerwall is a largely fixed cost business by its nature. This creates an operating leverage effect that results in expanding profit margins when revenue is growing; and contracting profit margins when revenues are declining. In light of what we now know about Outerwall’s current top line growth, we can expect the business’ earnings to fall off a cliff.

Falling revenues and falling earnings will naturally result in pain for the company’s shareholders. It’s actually made worse by the significant asset leverage with Outerwall’s capital structure. Not only does Outerwall carry around $680 million in net debt – an amount approximately equal to its current market capitalization – but the book value of shareholders’ equity has now turned negative. That is: the book value of Outerwall’s liabilities is now greater than the book value of its assets.

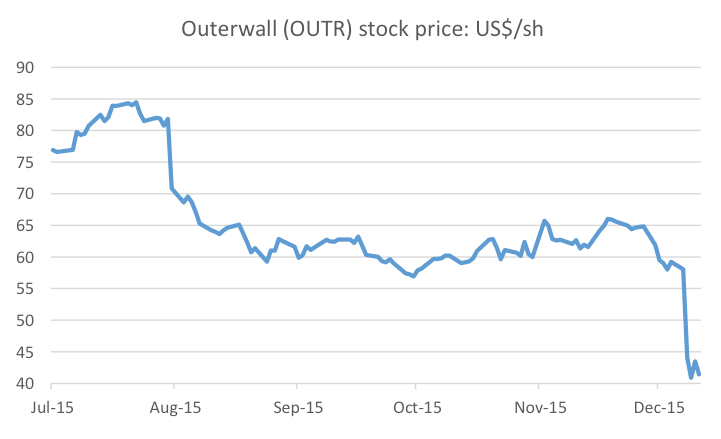

The wheels have started to fall off for Outerwall. Last week the company significantly revised the financial guidance it had provided the market just five weeks prior. Long story short, fourth quarter earnings are now guided to be down by more than 30 percent. The stock fell by 24 percent on this news, as illustrated below.

Given what we have described, shorting Outerall may now seem obvious – and in a sense, the application of our unique short portfolio framework is nothing more than the application of a logical process in an unbiased fashion. So you might be wondering who has been owning the stock throughout this year? Well, it has been a favourite of value investors that were enamoured with the stock’s low P/E ratio, of around 6.5x (currently it is just 5x). Surely this business was cheap, right?

We hope this example has illustrated both the efficacy of Montaka’s unique short portfolio framework and the perils of buying low P/E stocks without truly appreciating the trajectory of the business’ future earnings. This is known in the business as a “value trap” and something all value investors need to continually avoid.

Montaka has been short the shares of Outerwall since its inception.

![]() Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

[1] (WSJ) Home-Entertainment Revenue Fell in 2014, January 2015