|

Getting your Trinity Audio player ready...

|

In February this year, Daniel Wu wrote an insightful piece about Apple’s transformation from a company that has historically been driven exclusively by hardware to one which is today focussed on driving value through the growth of its services offering. One calendar quarter and a set of financial results later, Apple is demonstrating impressive growth and a long run way for the services it sells. And we think this is underappreciated in the stock price today.

Apple’s second fiscal quarter financial result was pleasing by all accounts. Sales of $61 billion in the quarter were 16% higher than a year ago; operating earnings of $16 billion, representing 26% earnings margin, grew 13%; and earnings-per-share were up 30% to $2.73. As one would imagine the iPhone drove a material amount of this strength. Apple sold 52 million iPhone in the quarter which translated into $38 billion in sales – over 60% of total company sales. But the outperformance of the Services business was most interesting to us. In fact, Services had its best quarter ever.

For the quarter Apple sold $9 billion worth of services (like Apple Music, app Store purchases and iCloud subscriptions) to its installed base of 1.3 billion devices that reside in the hands of around 600 million consumers. This was $2 billion or 31% more than it sold in the same period last year, representing an acceleration of the business from already high growth rate, and driving more than a quarter of Apple’s overall gain in sales. But as Daniel points out, services are much more profitable than hardware. So it is likely the Services division fuelled more than a third of Apple’s earnings growth.

Behind the high growth in Services was a rise in the number of subscribers that are paying Apple on a regular basis. Management revealed that these “paid subs” now total 270 million, up 100 million from a year ago and 30 million more than last calendar quarter. But this still represents less than half of Apple’s installed customer base. Said another way, on average not even one in two Apple device owners pay Apple or their providers for anything at all. This is one reason we believe the Services story still has a long way to go.

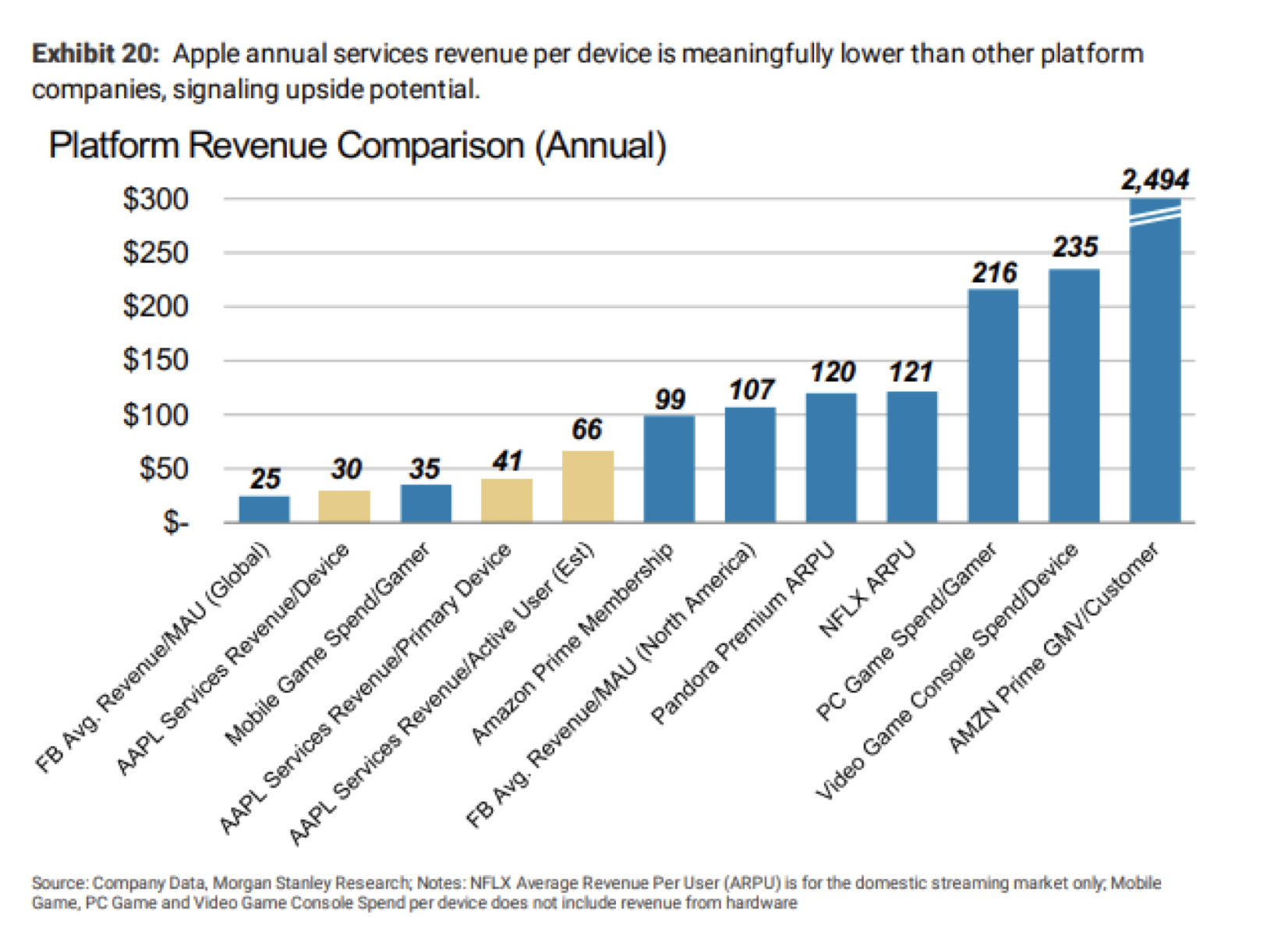

At the same time, those users still don’t pay a whole lot to Apple today. In fact, the average revenue per subscriber is around $136 per year. That’s clearly a very small amount compared to not only the income of an average Apple user (they are among the most affluent in the world), but also compared to the amount that subscribers pay to other platform companies. For example, today in United States subscribers to Amazon’s Prime service pay $99 each year; Pandora music streaming listeners pay $120 per year; and Netflix customers also pay about $120 per year. At the higher end of the spectrum there are video gamers spending well in excess of $200 per year. Yet Apple arguably offers a whole lot more.

Platform Company Revenue per User

Note: Apple’s metrics shown are different to the $136 quoted above due to the definition of the user in the denominator of the calculation of revenue per user.

Note: Apple’s metrics shown are different to the $136 quoted above due to the definition of the user in the denominator of the calculation of revenue per user.

Apple’s services suite includes Apple Music, a competitor to Pandora and the larger Spotify; iCloud Storage, a cloud computing storage offering; Apple Care insurance; the iTunes store for digital music downloads; iBooks book store; and the App Store, where Apple takes around a 30% cut (we call it the “Apple tax” of all app and in-app purchases. Still the overall Apple user base pays the company on average $5 per month per person. This is a second reason we believe the Apple services narrative is far from played out.

In the second quarter results call management gave us clear indications that its services offerings are performing strongly. In fact, the quarter was a record for many services. The App Store set a new all-time revenue record. Apple Music also scored a record for both revenue and paid subscribers, the number now surpassing 40 million. iCloud Storage revenue was up 50% to a new all-time record. And AppleCare set a new March quarter revenue record. The investment opportunity lies in the fact that today’s strong Services performance, and tomorrow’s long runway, is not being fully reflected in the current stock price.

Reverse engineering the expectations for Services metrics embedded in the current Apple share price of around $187 reveals an important insight. The market today is expecting revenue per subscriber has plateaued. That is to say that buying Apple stock today requires an investor to believe that Apple customers spend no more with Apple in 20 or 30 years’ time than they already spend with Apple today. That seems like an unreasonably conservative assumption to have to make. Or, more simply, Apple’s stock is cheap!

In our view, as more Apple device owners pay more for their Apple services the sales and earnings of Apple will continue to grow strongly – more strongly than the market is expecting – and that will drive Apple’s shares to new highs.

Montaka owns shares in Apple (NASDAQ:AAPL)

![]() Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.