|

Getting your Trinity Audio player ready...

|

– Daniel Wu

Chinese regulators have been busy in recent weeks. On the back of scuttling the Ant Group IPO at the 11th hour with draft regulations targeting online microlending practices, Chinese regulators hit the booming tech industry again this week with draft rules intended to curb monopolistic practices at China’s internet companies, sparking a $290 billion selloff across names like Alibaba, Tencent and Meituan. The draft rules, being characteristically vague, appear to target dominant internet companies, with a particular focus on e-commerce and local consumer services, and without specifying the scope or severity of potential penalties.

Regulatory intent to reign in the power of big internet companies is not unique to China. Tech antitrust has also gathered momentum in the US in recent years and culminated in the Department of Justice’s antitrust suit against Google’s dominant search business, with the FTC also expected to bring a case against Facebook. Meanwhile in Europe, the European Commission has just filed antitrust charges against Amazon’s e-commerce business and is also investigating Apple’s App Store practices. The difference in China, however, is the lack of an existing antitrust framework in a jurisdiction that is largely rule by law. For two decades, China kept western competitors out to foster national champions; now, these national champions have seemingly amassed too much power domestically.

Language of the antitrust proposal targets marketplace operators that leverage data, technology, algorithms or platform rules to unfairly limit competition or discriminate against consumers (mainly through pricing), the practice of forcing merchant exclusivity, the excessive use of subsidies, and the collusive sharing of sensitive consumer data. Given the focus on online commerce, Alibaba appears to be particularly vulnerable to an enforcement of the draft rules. While it is difficult to determine with a high degree of conviction what the impact of these rules may be, we believe there are several mitigating factors that could limit any adverse impact.

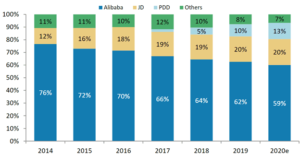

Firstly, it must be noted that Alibaba’s dominant position in e-commerce has been eroded in recent years as competition in the industry has intensified. There is clear evidence of existing competitors (JD) and new entrants (Pinduoduo, now Bytedance and other social media platforms with the rise of social commerce) successfully competing against Alibaba. These are all internet companies, so any regulations that target e-commerce platforms will likely impact all the leading players. Other competitors, particularly Pindoudou, make more prominent use of subsidies than Alibaba. And the issue of merchant exclusivity has also lessened in recent years as competition increased.

Chart: China e-commerce market share

Source: Morgan Stanley

Secondly, the draft rules appear to focus more on anticompetitive pricing than other behaviours – that is, using a dominant position to charge unfairly high prices, or pricing below cost to force out competitors. Alibaba does not abuse its immense trove of consumer data by engaging in widespread discriminatory pricing, nor is a below-cost pricing strategy sustainable in the long run considering its key competitors are now well established. Most importantly, the rules do not explicitly limit the use sensitive consumer data and/or algorithms for recommendation feeds, as this type of personalized targeting does not constitute discriminatory pricing but rather displaying more relevant products to consumers based on their personal preferences. And this use of data is where Alibaba’s platform value lies.

Ultimately, the Chinese regulators have made their intentions clear, even if details of the framework are still hazy. The goal appears to be the setting of guiderails for the healthy development of China’s internet economy, and that is a good outcome for all internet businesses, consumers and investors in the long term notwithstanding any short term stock price volatility.

Montaka owns shares in Alibaba Group.

Daniel Wu is a Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.