“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.” – Bill Gates

This pithy quote by Gates touches on an important shortcoming many of us face, either knowingly or unknowingly: our brains are not very good at accounting for the effects of compounding and exponential growth. Take, for example, the classic tale of a con man who presented the king with an offer.

The con man made chessboards, and knew the king loved chess. He devised a plan to trick the king into handing over a large fortune. The con man said that for his beautifully crafted chessboard he was not interested in money or jewels. Rather, all he wanted was a little rice.

“All I want,” said the con man, “is for you to place a single grain of rice on the first square, two grains of rice on the second, four on the third, eight on the fourth, and so on and so forth, for the entire 64 squares”. The king thought that for such a high-end chessboard this was a small price to pay. He agreed to the con man’s terms.

So a single grain of rice was placed on the first square, two on the second, until there were 128 grains of rice in the first row. However, the second row started to present problems for the king – by the 21st square the king owed over a million grains of rice. By the 41st square, the king owed over a trillion grains of rice. The effects of compounding had taken over, and the king obviously hadn’t factored this in.

There are countless examples of problems that involve compound growth that fool our brains (e.g., you only need to fold a piece of paper in half 45 times to produce a stack of paper tall enough to reach the moon). Our brains just aren’t wired to grasp the power of compounding. This has important implications in the realm of investing, and the effects of compounding can present challenges when valuing high growth companies.

My colleague Andy Macken recently wrote a whitepaper on the businesses of the future, discussing high growth companies such as Tencent and Alibaba. These Chinese tech giants are growing revenues at 50%+ rates per year. In light of such growth, a pertinent question to ask is: what are the appropriate revenue growth rates to use when valuing these businesses?

A hypothetical example can help illustrate the wide divergence that can result over time from relatively small differences in growth rates, particularly when those growth rates are large and have a more prominent compounding effect. The following table presents three growth scenarios for a $1,000 revenue stream over a three year period.

It might seem sensible to taper down the high growth rates for companies such as Tencent and Alibaba when making valuation forecasts. One might take the view that continuing to grow revenues at such a heady rate, particularly given the already enormous revenue base, will encounter constraints due to the law of large numbers. It’s possible, however, that these businesses might grow in an entirely different fashion, despite their already monumental size.

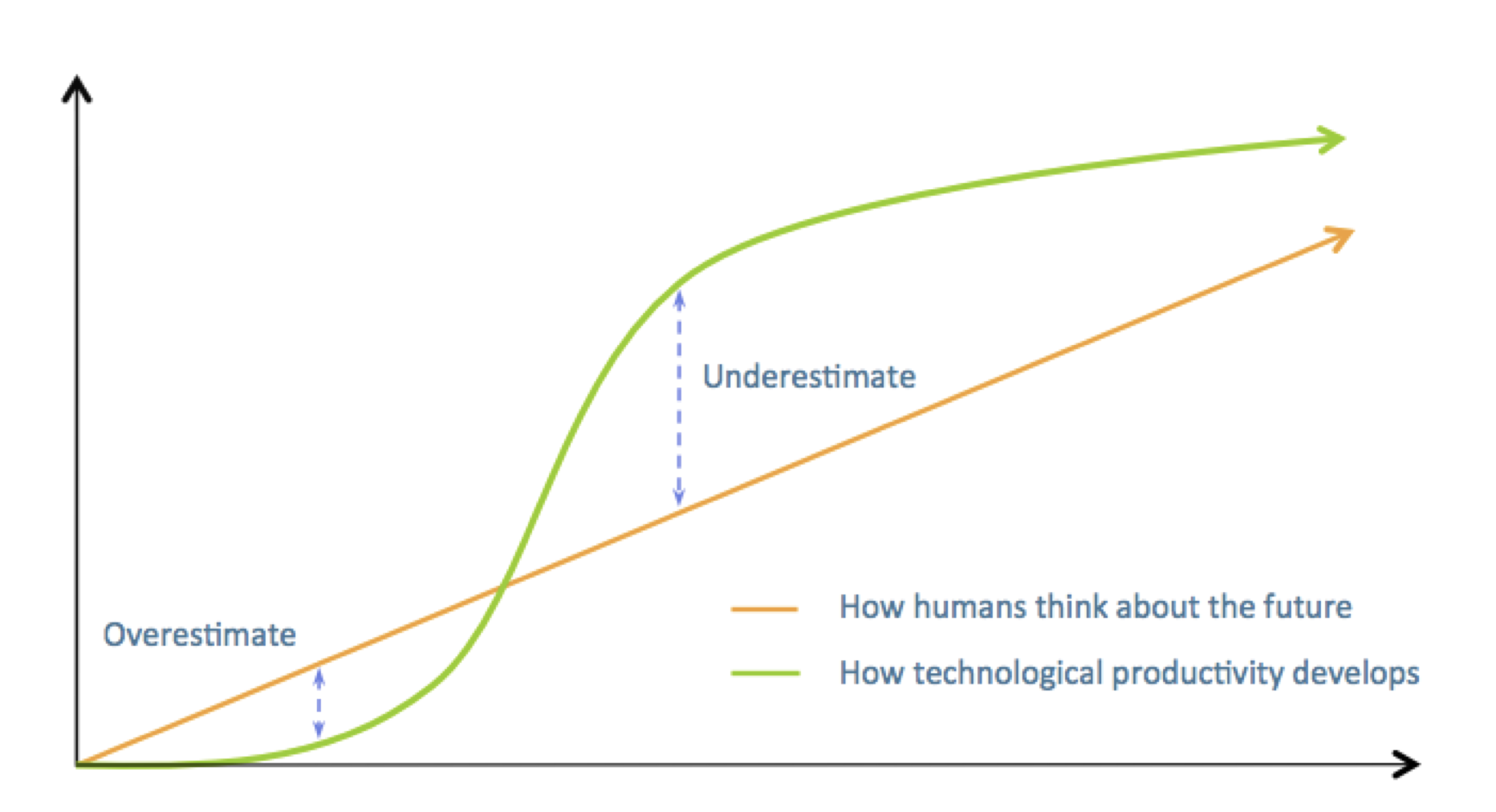

These platform companies can sometimes follow S-curve growth patterns that are very difficult to predict. The graph below provides an interesting visual representation of the cognitive errors we can make when trying to forecast these businesses.

Source: Rocrastination

Part of the reason why these platform companies can experience an unexpected acceleration in growth is because they are really an aggregation of individual S-curves.

So what does this mean? Essentially businesses like Tencent and Alibaba have their fingers in many pies; they have early-stage businesses and venture capital-style investments, in addition to their core businesses. These early-stage businesses are each at different stages of growth, typically characterized by a period of investment, followed by mass adoption and the gaining of critical scale.

Due to the huge base of users for Tencent and Alibaba, these early stage businesses can reach scale very rapidly and the growth rates can be enormous. For example, in Q1 of 2017 Tencent’s video subscription revenues more than tripled year-over-year. When you aggregate many of these non-core businesses – for Tencent they include businesses in cloud computing, online payments, literature, and many others – the growth contribution can become meaningful over time. In Tencent’s case, its “Others” segment grew revenue by 263% in FY16, comprising a quarter of the company’s total revenue growth.

Investors should always be wary of the difficulty of the human mind in appreciating the effects of compounding. Years from now companies like Alibaba and Tencent will have substantial businesses that investors either modeled too conservatively, or simply weren’t even aware of. Such is the result of high growth online tech platform businesses combined with the failure of many to intuitively grasp exponential growth patterns.

Montaka owns shares in Alibaba (NYSE: BABA).

George Hadjia is a Research Analyst with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Underestimating the Power of Compounding

“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten.” – Bill Gates

This pithy quote by Gates touches on an important shortcoming many of us face, either knowingly or unknowingly: our brains are not very good at accounting for the effects of compounding and exponential growth. Take, for example, the classic tale of a con man who presented the king with an offer.

The con man made chessboards, and knew the king loved chess. He devised a plan to trick the king into handing over a large fortune. The con man said that for his beautifully crafted chessboard he was not interested in money or jewels. Rather, all he wanted was a little rice.

“All I want,” said the con man, “is for you to place a single grain of rice on the first square, two grains of rice on the second, four on the third, eight on the fourth, and so on and so forth, for the entire 64 squares”. The king thought that for such a high-end chessboard this was a small price to pay. He agreed to the con man’s terms.

So a single grain of rice was placed on the first square, two on the second, until there were 128 grains of rice in the first row. However, the second row started to present problems for the king – by the 21st square the king owed over a million grains of rice. By the 41st square, the king owed over a trillion grains of rice. The effects of compounding had taken over, and the king obviously hadn’t factored this in.

There are countless examples of problems that involve compound growth that fool our brains (e.g., you only need to fold a piece of paper in half 45 times to produce a stack of paper tall enough to reach the moon). Our brains just aren’t wired to grasp the power of compounding. This has important implications in the realm of investing, and the effects of compounding can present challenges when valuing high growth companies.

My colleague Andy Macken recently wrote a whitepaper on the businesses of the future, discussing high growth companies such as Tencent and Alibaba. These Chinese tech giants are growing revenues at 50%+ rates per year. In light of such growth, a pertinent question to ask is: what are the appropriate revenue growth rates to use when valuing these businesses?

A hypothetical example can help illustrate the wide divergence that can result over time from relatively small differences in growth rates, particularly when those growth rates are large and have a more prominent compounding effect. The following table presents three growth scenarios for a $1,000 revenue stream over a three year period.

It might seem sensible to taper down the high growth rates for companies such as Tencent and Alibaba when making valuation forecasts. One might take the view that continuing to grow revenues at such a heady rate, particularly given the already enormous revenue base, will encounter constraints due to the law of large numbers. It’s possible, however, that these businesses might grow in an entirely different fashion, despite their already monumental size.

These platform companies can sometimes follow S-curve growth patterns that are very difficult to predict. The graph below provides an interesting visual representation of the cognitive errors we can make when trying to forecast these businesses.

Source: Rocrastination

Part of the reason why these platform companies can experience an unexpected acceleration in growth is because they are really an aggregation of individual S-curves.

So what does this mean? Essentially businesses like Tencent and Alibaba have their fingers in many pies; they have early-stage businesses and venture capital-style investments, in addition to their core businesses. These early-stage businesses are each at different stages of growth, typically characterized by a period of investment, followed by mass adoption and the gaining of critical scale.

Due to the huge base of users for Tencent and Alibaba, these early stage businesses can reach scale very rapidly and the growth rates can be enormous. For example, in Q1 of 2017 Tencent’s video subscription revenues more than tripled year-over-year. When you aggregate many of these non-core businesses – for Tencent they include businesses in cloud computing, online payments, literature, and many others – the growth contribution can become meaningful over time. In Tencent’s case, its “Others” segment grew revenue by 263% in FY16, comprising a quarter of the company’s total revenue growth.

Investors should always be wary of the difficulty of the human mind in appreciating the effects of compounding. Years from now companies like Alibaba and Tencent will have substantial businesses that investors either modeled too conservatively, or simply weren’t even aware of. Such is the result of high growth online tech platform businesses combined with the failure of many to intuitively grasp exponential growth patterns.

Montaka owns shares in Alibaba (NYSE: BABA).

George Hadjia is a Research Analyst with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Underestimating the Power of Compounding

This content was prepared by Montaka Global Pty Ltd (ACN 604 878 533, AFSL: 516 942). The information provided is general in nature and does not take into account your investment objectives, financial situation or particular needs. You should read the offer document and consider your own investment objectives, financial situation and particular needs before acting upon this information. All investments contain risk and may lose value. Consider seeking advice from a licensed financial advisor. Past performance is not a reliable indicator of future performance.

Related Insight

Share

Get insights delivered to your inbox including articles, podcasts and videos from the global equities world.