|

Getting your Trinity Audio player ready...

|

-Daniel Wu

The past 15 months have been a roller coaster ride for public market investors. From the violent crash in March 2020 and the precipice of the next great depression to the fastest stimulus-fueled recovery in living memory, the pandemic era can be characterized by the extremes of fear and greed. When faced with great uncertainty, investors often lose sight of the long-term and struggle to see beyond what’s next. Narratives accelerate – often much faster than underlying business fundamentals – dragging asset prices along for a wild ride.

This myopic instinct to focus on what’s next instead of what it’s worth can be seen all across the investment landscape, from airlines and travel-related stocks to unprofitable hypergrowth software businesses. One pertinent example of this default to first-order thinking can be seen in the retail sector. The share prices of discretionary retailers with low online penetration or bloated store bases were crushed during the March 2020 crash – perhaps rightly so given the existential threat of lockdowns and store closures of unknown duration on top of already-weak fundamentals. But many of these stocks have seen huge upward re-ratings since the November vaccine announcements on the reopening narrative.

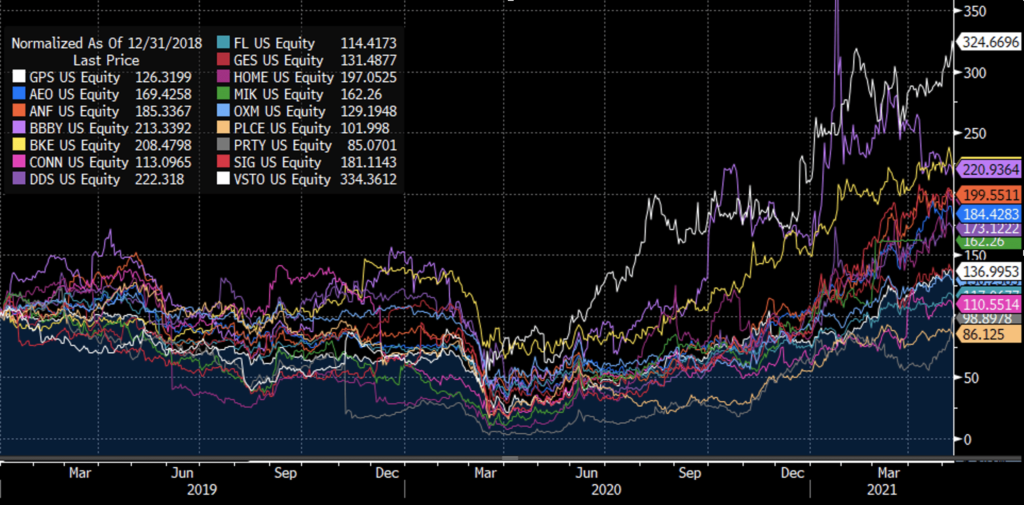

Chart: Share price performance of selected retailers (31/12/2018 = 100)

Source: Bloomberg

What is interesting about the chart above is that these retailers were collectively struggling pre-COVID against a myriad of secular headwinds – chief among them the structural shift to e-commerce at the great expense of mall traffic and the overcapacity of physical stores in a rapidly digitizing world. These retailers faced the challenge of declining store traffic and deleverage of store costs as lower margin e-commerce sales cannibalized high margin in-store sales (since rent is fixed). If we consider the changes brought about by COVID-19, none of them appear to be positive catalysts for this subset of retailers. E-commerce adoption and penetration has sharply accelerated, brands have increasingly shifted into direct-to-consumer channels and malls remain irrelevant as ever. Additionally, the cost of logistics and last-mile delivery has increased due to the step-change in demand and any rent savings from lease renegotiations or store closures may need to be reinvested into performance marketing, which can be considered the “online rent”.

Yet the share prices of these retailers are well above their pre-COVID levels – particularly for those retailers that raised capital during the pandemic – driven by the reopening narrative and pent-up consumer demand after more than a year of restrictions. But what happens after the reopening surge? Are these businesses worth more today than they were pre-COVID once the stimulus cheques and excess savings have been spent (which we believe will flow disproportionately into travel and experiences vs physical retail)?

We believe the answer is a firm “no”. These businesses may report several quarters of strong earnings on the back of easy comps and the reopening surge but will then have to lap this strong performance in an operating environment that hasn’t improved nearly as much as their share prices have. We believe this predisposition of the market to overvalue what’s next may lead to some interesting mispricings in the near term, and the Montaka team will be keeping an eye out for any opportunities on the short side.

Daniel Wu is a Senior Research Analyst with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.