|

Getting your Trinity Audio player ready...

|

The Montaka funds have a long history on the short side of Campbell’s Soup. We’ve researched the company almost since the funds launched four years ago and initiated a short position in Campbell’s stock around three years ago. Over this period our position size has varied, but we have constantly been concerned about Campbell’s highly priced stock considering its ongoing fundamental deterioration. You can read and hear more about this in a previous article, and at the Sohn Hearts & Minds conference. In this article I want to use Campbell’s latest financial results as an opportunity to give an update on the business.

What’s in the can?

Following the completion of divestitures of fresh food businesses, Campbell’s is comprised of two key business segments: Meals and Beverages, and Global Biscuits and Snacks.

Meals and Beverages (MB) consists of the iconic Campbell’s Soup business, which includes ready-to-serve, condensed and broth; V8 shelf stable vegetable-based drinks; Prego pasta sauces and some other canned and bottled foods. At the end of the day, soup feeds this division and it accounts for around half the company’s sales and 60% of earnings.

Campbell’s Meals and Beverage products

Global Biscuits and Snacks (GBS) is the amalgamation of Campbell’s legacy Pepperidge Farm cookies and Goldfish crackers brands, and brands from the acquisition of Snyder’s-Lance that took place early last year. The newer labels added include Snyder’s of Hanover pretzels, Kettle and Cape Cod chips. In addition, this segment is home to international cookie and snack brands, like Arnott’s, Australia’s leading biscuit brand.

Campbell’s Global Biscuits and Snacks products

Campbell’s is actively looking to sell these international businesses but is yet to find a buyer. Negotiations with Mondelez, the owner of Oreo cookies, ended recently when price became a sticking point. As it stands today, Campbell’s snacking division represents half the company’s sales and 40% of its earnings. Without the international assets however, the earnings contribution will likely fall to about one third.

After years of acquisitions, and now a period of divestitures, Campbell’s has transformed itself from a soup company – with some biscuits and chips – into…a soup company – with some biscuits and chips.

Not what it says on the label

Given the strategic restocking that Campbell’s has undergone, it makes sense now more than ever for investors to be focussed on the important soup franchise, after all it will probably drive up to two-thirds of company profits very soon. It seemed to be turning the corner – until we scratched the surface (or the label).

In the most recent quarterly financial results, Campbell’s reported signs of life in soup which has been in chronic decline for years. The reported top line for the MB segment was just over $1 billion and less than one percent lower than the same period last year and demonstrated some stability for a business that was declining at mid-single-digit percentage rates the past few quarters. Unfortunately, the underlying performance isn’t as appetising.

On the earnings conference call, management gave some additional colour around the MB result that included one percentage point of growth related to an accounting change – so that 1% year-on-year decline was really a 2% decline on a comparable basis.

There was also a percentage point of growth that came from removing promotions from some soup products and increasing prices on others. Management explicitly commented that it does not believe the environment will allow this sort of price/promotion gain in future. Removing this unsustainable source of growth brings the run rate decline trend to negative 3%.

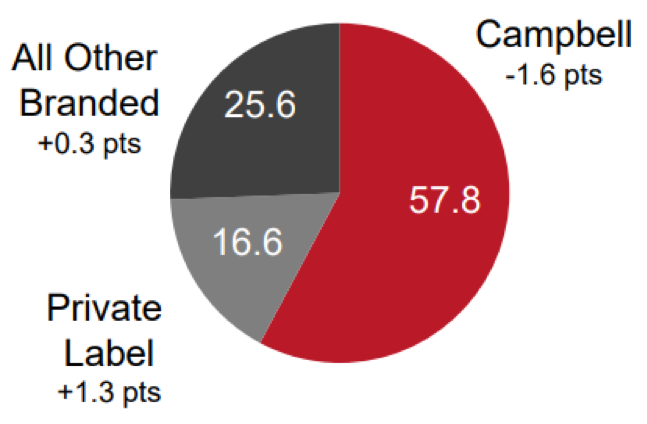

Not even the sale volumes were as they seemed. While Campbell’s management noted soup volumes for the company were flat during the quarter this seems to be more a reflection of the intra-year ebb and flow of grocery store stocking. Volumes of soup sold out to the consumer, distinct from those sold into the supermarkets like Walmart, declined almost 3% and Campbell’s market share of US retail soup sales fell again. Adjusting for this timing benefit means that MB sales trends could be down five to six percent.

US wet soup latest 52-week market share (and change)

Pressurized

Even with several temporary boosts to sales, Campbell’s failed to grow earnings in the MB segment in the most recent quarter. Operating earnings (before interest expense and taxes) declined 5% compared to the same period last year. True this was much better than the 10% decline from last quarter, or the 20%-plus declines in the quarters before that. But it should not be lost on investors that this business is still going backwards. Imagine what the result might be when the one-off sales supports don’t repeat in future periods.

Soup’s poor performance contributed to falling profits for the entire company. Excluding the sold divisions operating earnings fell by 2%. Worse still this result included a couple months sales from Snyder’s-Lance that weren’t included in the prior year’s period and benefited from the pull forward of cost saves.

Cost saves for the quarter outperformed management’s expectations by $30 million or around 10% of company earnings in the period. However, management’s total cost save target for its multi-year program, including synergies from the Snyder’s-Lance deal, remained unchanged. This reflects improved timing of the realisation of savings rather than a step-up in the amount of costs that could reasonably be taken out of the business. And if the timing had not have been so fortunate the earnings of the continuing business might have been down double digits.

At the same time as the underlying profits keep going in reverse, Campbell’s remains constrained by its indebtedness. Net debt at the company is still above $9 billion, which is more than seven times the annualized operating earnings of the continuing business and almost half of the total capitalization of the enterprise. Such elevated debt levels add another layer of downward pressure on the value of shareholders’ equity.

What’s left in the bowl

Today, we see Campbell’s as a declining soup business, with profit’s falling faster than sales; that is supplemented by a lower-margin snacks business, with some growth potential that may have been diluted by acquisition; weighed under by a heavy serve of debt.

Montaka is short Campbell Soup Co

![]()

Christopher Demasi is a Portfolio Manager with Montaka Global Investments.

To learn more about Montaka, please call +612 7202 0100.