|

Getting your Trinity Audio player ready...

|

Teradata is a pioneer and global leader in providing high end data warehouse and analytics technology solutions to large enterprises. But the industry landscape has been changing and Teradata has failed to keep pace. The likely outcome is that Teradata’s future earnings will be pressured beyond current expectations. Consequently, the Montaka Global Fund maintains a short position in the shares of Teradata.

No doubt many readers will be interested to find out why we have arrived at a pessimistic view of Teradata’s shares and how the position fits within the unique short framework we implement at Montaka. Rest assured this follows in short order and forms the first part of this article. At the same time, we feel that readers may also be interested to learn more about how Teradata came to us in the first place. So the second part of this article will be dedicated to walking through the idea generation process specifically as it relates to Teradata.

Why we are short Teradata

Let’s begin with a bit of background. The concept of Teradata and its flagship data warehouse grew out of research at California Institute of Technology, or CalTech, in the late 1970s. As with many other ground-breaking technology businesses Teradata’s founders worked from a garage in Burbank California and by 1979 they had developed a revolutionary database management system that allowed quick and powerful processing of vast amounts of data in order to support analytical decision making. In fact, Teradata was named for its ability to one day manage terabytes (trillions of bytes) of data which came a reality in 1992 when Wal-Mart went live with a Teradata system.

Over the next couple decades Teradata developed ever larger and more advanced data warehouses and analytic platforms consisting of software optimized on proprietary hardware (think of big boxes full of servers and storage). By the 2000s Teradata was “the” place to go for the largest companies looking to extract insights quickly from the vast, growing and increasingly complex data sets distributed throughout their organizations. But things began to change.

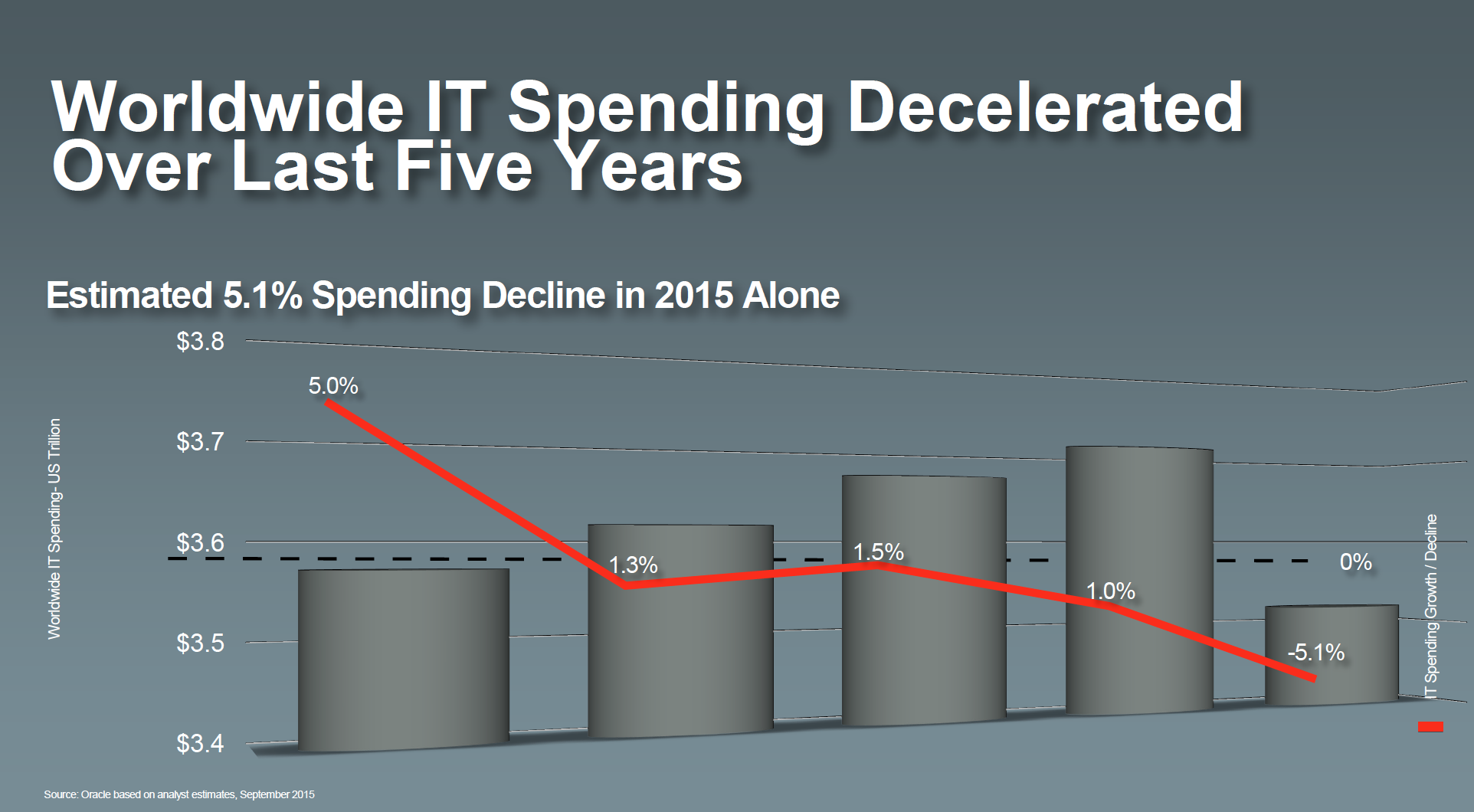

To begin with large corporates have experienced weak revenue growth amidst a slow and uneven economic rebound following the years of the global financial crisis. As a result, corporate IT managers have been in penny pinching mode. Worldwide spending in IT decelerated over the past 5 years and declined in 2015. To make matters worse for Teradata, IT spend has been reallocated away from the nice-to-haves – including data warehouses and analytics – and towards business critical categories like security, compliance and mobility.

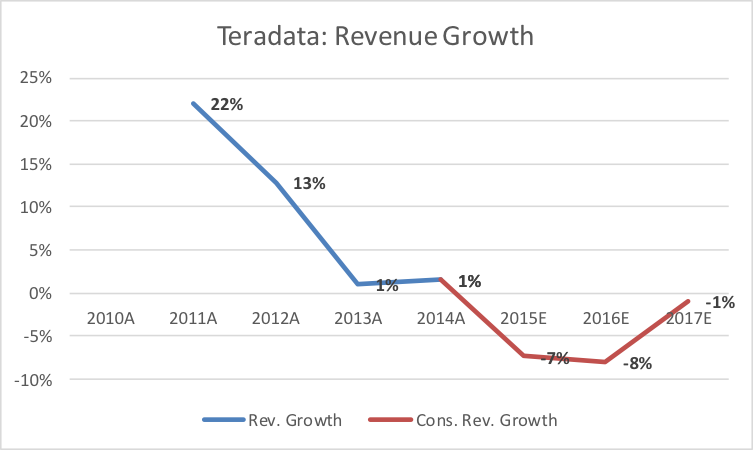

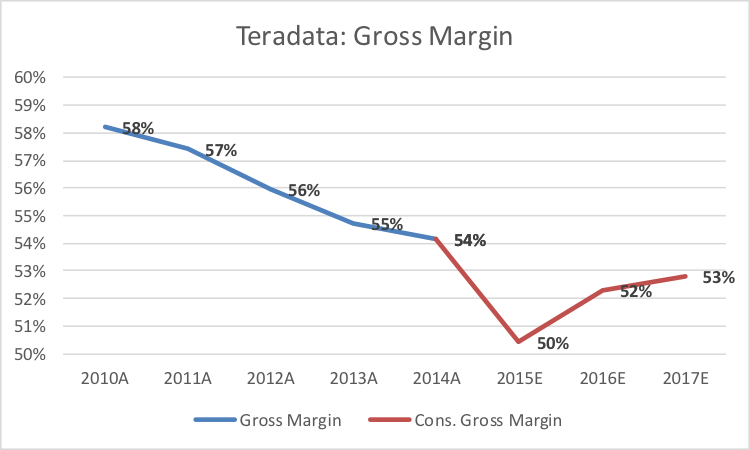

Spending on large, over-priced and often under-utilized hardware is also being replaced with spending on more efficient systems and value add software. Historically Teradata’s flagship integrated data warehouse (IDW) has been its core offering, driving the majority of revenue growth and profitability over decades as the largest corporations invested in building out platforms on their own premises. Yet according to the company itself, customers have over invested and future capacity requirements will be muted going forward. Said another way demand for the highest price IDW systems has not only matured but it has been stretched to breaking point.

The development of cloud computing delivery models has accelerated this trend away from large hardware purchases. With the ability to buy compute and storage capacity flexibly and cheaply, large corporates have turned to Amazon Web Services and Microsoft Azure cloud platforms rather than buying machines in bulk for their own in-house data centres. This all means Teradata’s customers are buying lower priced products in lower volume. The numbers indicate this. Revenues from Teradata’s top 50 customers have declined at mid-single digit percentage rates for each of the past 3 years.

Even as customers have changed their buying patterns over a multi-year period Teradata has seemed to be stuck in its ways. Finally, in 2015 management conceded to the industry trends and begun to develop and promote smaller data appliance systems, software-only versions and cloud-based offerings. Unfortunately for Teradata, many large and well-resourced enterprise technology companies had already started down this path.

Oracle, Microsoft, IBM and Cisco have all ramped up their data warehouse capabilities and met the market as corporate customers traded down from Teradata’s state-of-the-art systems to “good enough” substitutes which can be priced at 10% to 40% discounts. Even free data management and analytical software (open-source) is being supported. Cloud too has played a role in the disruption. Both Amazon and Microsoft offer a range of proprietary and third party data warehouse and analytics platforms that can be rented by the hour or the byte.

Clearly the competitive landscape is dominated by behemoths. Combined Oracle, Microsoft, IBM, Cisco and Amazon have combined revenues approaching $400 billion and combined market capitalization of $1.1 trillion. By comparison Teradata generated $2.5 billion of revenue in 2015 and was most recently capitalized at $3.5 billion. Moreover, the real battle ground in technology is research and development capability and spend. Consider that Teradata spends just $200m annually on R&D, representing 8% of sales, compared to Oracle’s $5.5 billion annual R&D budget. Teradata is a sub-scale player coming from behind in a world of giants bounding ahead.

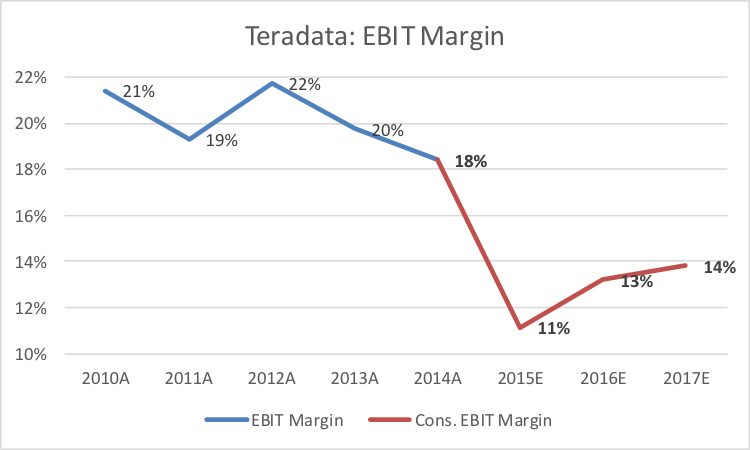

With such a depressing outlook it would be natural to conclude that Teradata should see continued revenue declines over time. And that pricing and therefore gross profit margins will be eroded. All on top of an increasing cost base as management 1) surely needs to keep hiring engineers (and paying them well) to design ever more competitive products, and 2) the sales force needs to be retooled, redirected and re-upped to keep front of customers minds. The “market” says otherwise.

Consensus forecasts have revenues stabilising after 2016. Gross margins are projected to rise. And leverage on operating costs gives way to expectations for increasing earnings margins.

Quite simply we think the odds are stacked against Teradata and the earnings expectations will prove to be too high. Until the outlook changes, or expectations (and the stock price) converge to reality we will likely remain short the shares of Teradata.

Where did the idea come from?

Avid readers and students of the Montaka research process will be aware that our approach to idea generation is a two-pronged approach.

On one hand we use a quantitative tool that implements a proprietary fundamental model in order to screen literally thousands of businesses listed on stock exchanges globally. The “quant tool” processes a large amount of data quickly and without human bias (fitting that we are talking about Teradata today), and ranks the stocks by decile. While Teradata did not screen as a terrible business, but it was definitely not at the top of the pile, finishing in decile 3.

On the other hand, we have a qualitative process to identify prospective investment opportunities. This process includes all the systematic and ad-hoc reading, research and analysis that the Montaka team does on a daily basis. Where we humans have an advantage over the machine is in our ability to recognise change and apply judgement around the true economics of the business. We give more credit to the qualitative process than its quantitative counterpart when it comes to Teradata’s genesis.

In the back half of last year, the Montaka team became fascinated by the disruption and change being caused by cloud computing and the resulting impacts on the enterprise technology industry. As a starting point we already held long positions in businesses that were benefitting from a shift to cloud subscriptions over traditional upfront transactional license or boxed software sales. Unfortunately, for these companies at the time, their current earnings were not yet representative of the true underlying economics of the new business model. Fortunately, for us and our clients, the share prices of these companies were not fairly representing the intrinsic value being accrued. We had a good understanding of the space, but we wondered what more we could learn about cloud? Who else was disrupting and being disrupted? Were there risks to our long positions? Were there opportunities for new short positions?

Our inquisitive nature led us to speaking with our network of contacts across the globe, and consuming industry articles, blogs and thought pieces. Moreover, we reached out to industry experts. Typically former senior employees and even founders of top technology companies like Amazon, Oracle, Microsoft and CSC, we were able to conduct in depth discussions about the opportunities and risks that were being created by enterprise adoption of cloud services and the related commoditization and improved utilization of computing resources.

It became clear to us (again) that predicting the winners of a next-gen technology paradigm is not an easy task, and determining the future economics of the winning businesses is even harder. Coincidentally it became relatively obvious which business models will be fundamentally challenged for the rest of time. We triangulated our insights with our knowledge and past experiences and a few names bubbled to the top. The most prospective of these was Teradata. So, as you can see from above, we decided to give it more of our time. a lot more of our time. And, we believe, deservedly so.

***

Montaka Global Fund holds a short position in Teradata.

![]() Christopher Demasi is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.

Christopher Demasi is a Portfolio Manager with Montgomery Global Investment Management. To learn more about Montaka, please call +612 7202 0100.