|

Getting your Trinity Audio player ready...

|

– Andrew Macken & Chris Demasi

We are now three-quarters through an astonishing year. The US recession that many expected has remained elusive thus far. Year-to-date in 2023, the median stock in the S&P 500 is up just 3%, while the median stock in the Russell 2000 is down by 5%. And yet, a small fraction of stocks (around 9% of the S&P 500) are up a lot – by more than 30%. (Montaka has been fortunate to own 11 of these).

We’ve raised the possibility that markets may well have entered a period of higher dispersion. That is, a period characterized by more extreme winners and losers in the stock market. A period we have not seen for decades. And, if so, a period that would demand greater active management and adherence to the investing principles that have been proven to work well, including high portfolio concentration, patience in ownership, and with the structure to withstand periods of drawdown. We assemble the important academic research on these topics in Montaka’s recent whitepaper which we encourage readers to review.

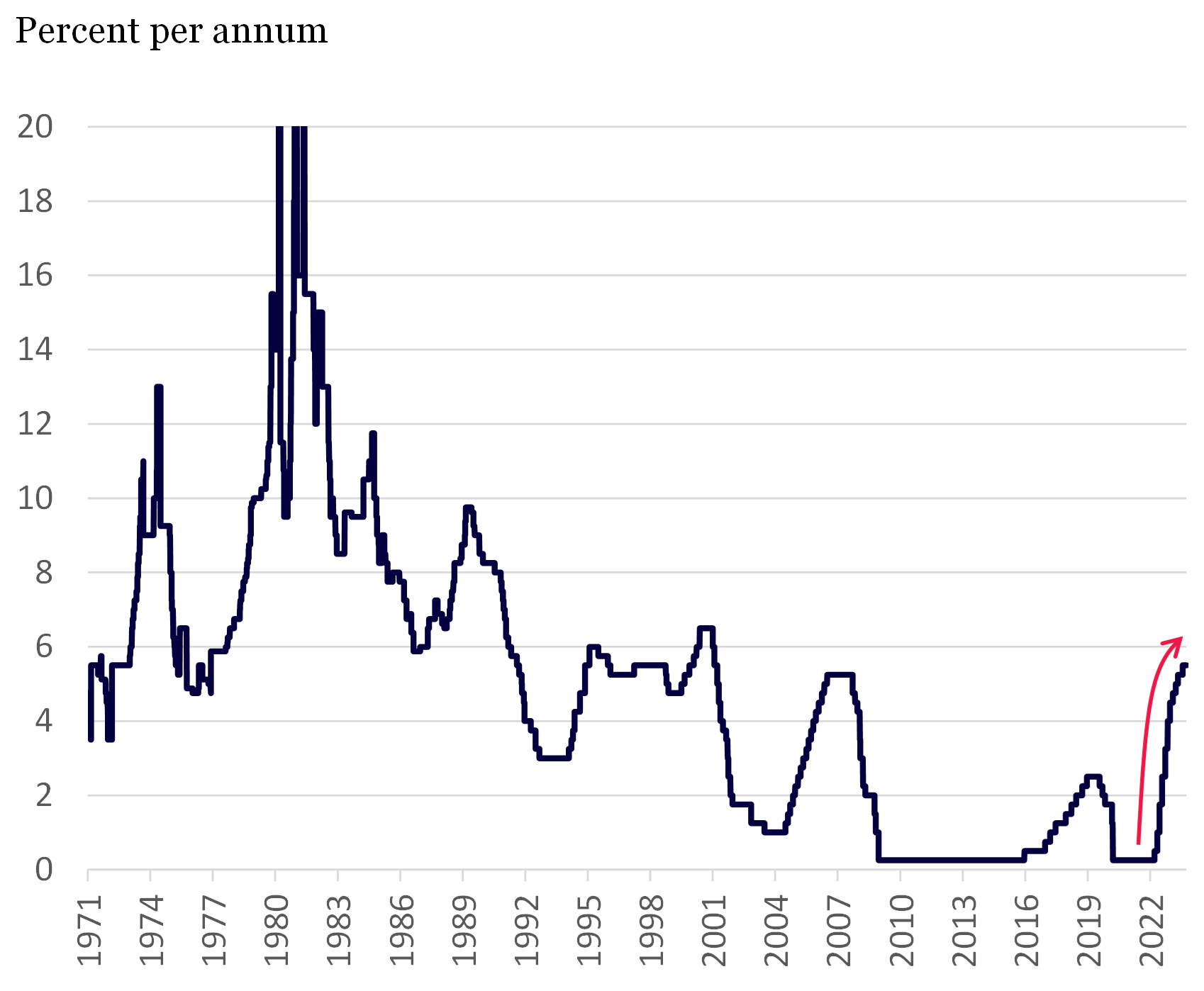

The price of money has increased materially and at a rapid rate since early 2022. Of course, no one really knows where interest rates will go from here, but certainly several high-profile financiers, including JPMorgan’s CEO, Jamie Dimon, are advising clients to prepare for possible scenarios of rates as high as 7% per annum.

US Federal Reserve – Policy Rate

Source: Bloomberg

The geopolitical equilibrium has changed almost as rapidly as interest rates. In recent weeks, US Secretary of State, Antony Blinken, stated categorically that the post-Cold War era has now come to an end and that there is “intense competition” for what comes next. From the war in Ukraine, to an expanding NATO, to Russia’s new partnership with North Korea, to an expanding BRICS, and four coups in Africa so far this year alone.

The competition for what comes next is clearly intensifying. And this could have significant implications for large western businesses – including even some of the ‘safest’ household names – that (i) sell into the Chinese market, (ii) are supplied via the Chinese market, (iii) compete directly with Chinese products, or even (iv) rely on advanced semiconductors – substantially all of which are fabricated by a single company, and in Taiwan.

And speaking of rapid change, recent advances in the AI revolution – while still in its infancy – are perhaps moving at the fastest pace of all. ChatGPT can now see, hear and talk. Microsoft is releasing its Copilot in the coming days. Meta AI is your own personal assistant being infused into Meta’s properties and hardware. Spotify is using AI to translate your podcast into your choice of language. And ServiceNow is using generative AI to dramatically increase the productivity of internal and external service assistants.

This is why we believe the future will look different to the past. Why there will be more divergence between winners and losers. And why we believe Montaka’s analysis of evolving global dynamics will continue to be of service to clients.

We remind investors that, over the very long term, great shareholder returns are overwhelmingly driven by compounding earnings power, and not by changes in valuation multiples – which interest rates and other top-down factors are affecting today. This is why most of the analysis undertaken by Montaka’s investment team would be classified in the ‘microeconomic’ bucket, not ‘macroeconomic’. That is, the competitive positions of individual companies, their adjacent opportunities, and the decisions made by their management teams to sustainably grow earnings over time. And these microeconomic attributes of a company are always considered carefully in the context of the market-implied expectations for revenues and earnings embedded in its current stock price.

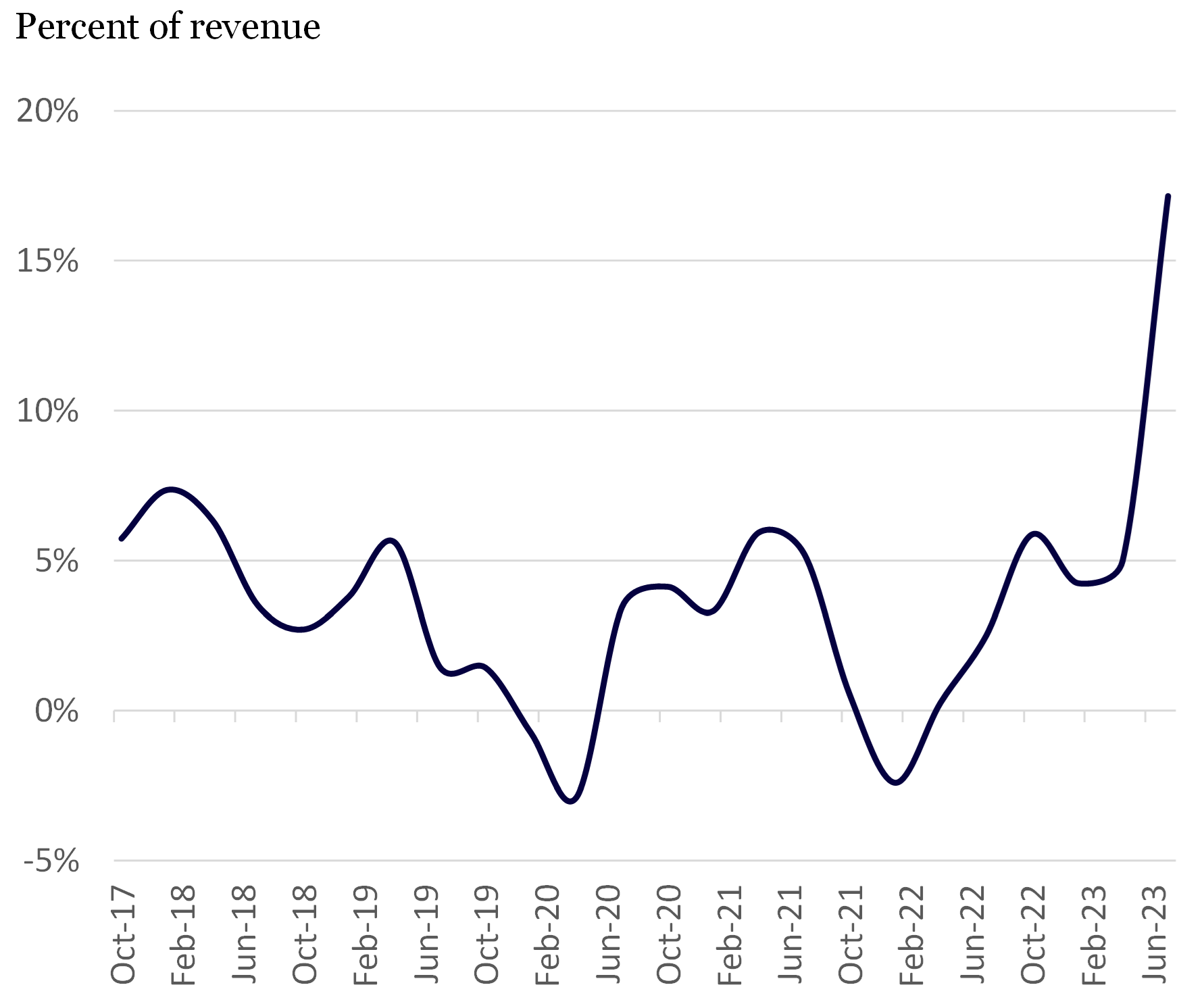

We remain very happy with Montaka’s major investee companies. These are businesses that have tremendous advantages that we believe remain underappreciated. Furthermore, we have been particularly pleased and impressed by the significant cost controls effected by these businesses of late. Salesforce’s recent result included the most recent demonstration of this. In its most recent quarter, the company’s operating margin was more than 10 percentage points higher than a year ago!

Salesforce Operating Profit Margin

Source: Bloomberg

Speaking of cost controls, this is one of the reasons we remain so interested in Spotify as an investment opportunity. Of course, it has a wide lead in global audio streaming and tremendous data advantages that we believe will result in further monetisation opportunities. But it is good old-fashioned cost-base rationalization that will be the primary driver of substantial profit growth over the next 1-2 years. And we believe this remains underappreciated by the stock market today, as Lachlan describes in the case study linked here.

Indeed, our very low portfolio turnover is a direct consequence of the quality and upside potential of Montaka’s existing investments. This is not to say these are the only opportunities out there today. Over recent weeks and months, Montaka’s investment team has identified several great businesses that are growing into attractive adjacencies and, yet, find themselves to be undervalued today, in our assessment. But we cannot justify buying them because we would need to sell something we already own that we believe is an even better investment opportunity.

That said, there were two small changes to the tail-end of Montaka’s portfolio during the quarter. We exited St James’s Place and Bank of America. In the case of the former, we did not make money on this investment, though had risk-managed the position over time into one of Montaka’s smallest. While the stock is probably undervalued today, we have not been happy with management’s decision-making over time, and we see better opportunities elsewhere. In the case of Bank of America, this was always intended as one of our few tactical (and, therefore, typically shorter-term) investments. We made money on this quickly as bank stocks rebounded following the collapse of Silicon Valley Bank earlier in the year. Longer term, we see better opportunities elsewhere for this capital.

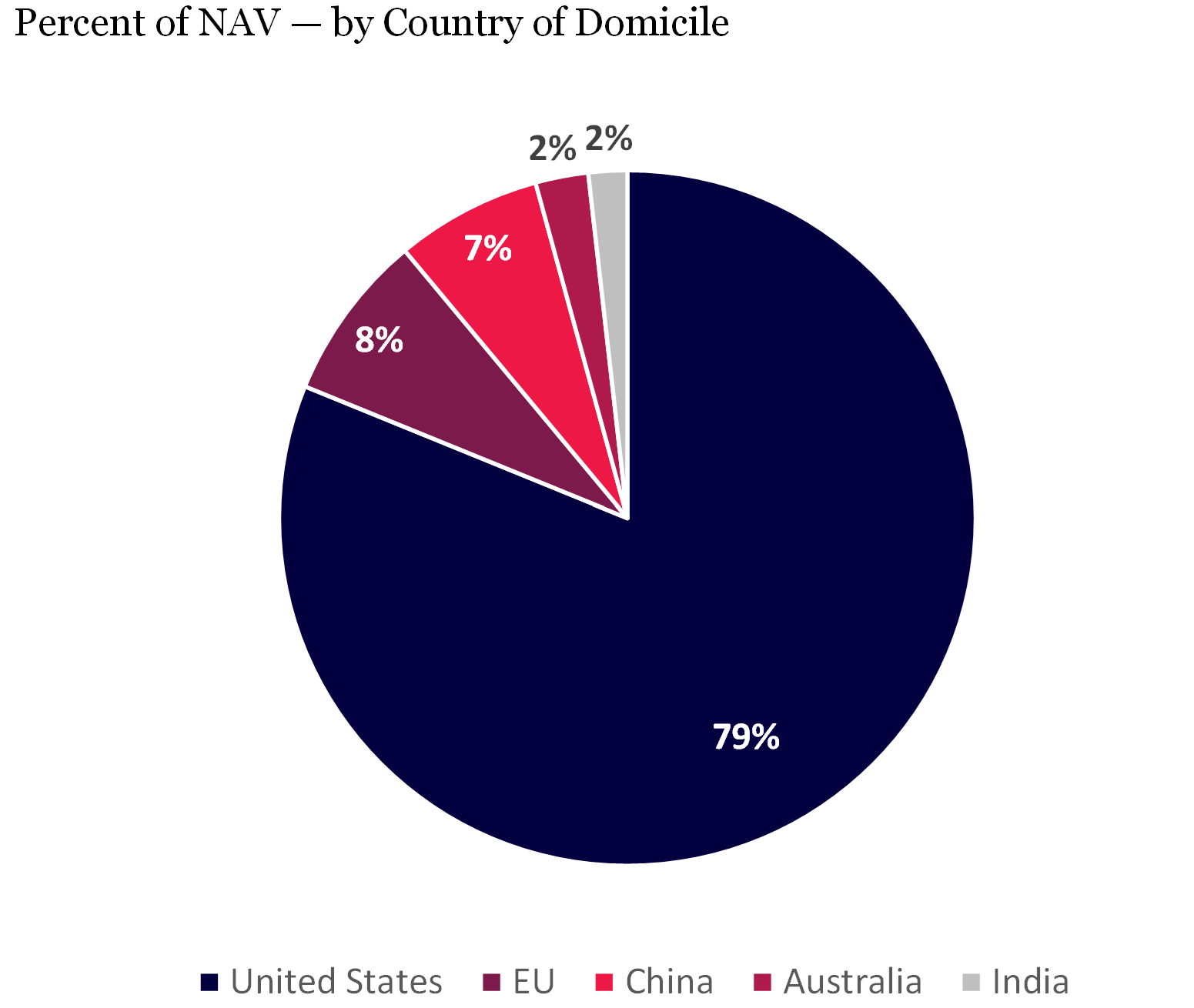

Overall, Montaka’s portfolio remains weighted heavily towards US-domiciled investments. While we do have some modest exposure to China, we have deliberately ensured there is minimal ownership of businesses with cross-Chinese-border exposure on both the revenue side, and the supply-chain side.

Montaka’s Long Exposure

Source: Montaka

We thank you for your ongoing partnership with Montaka. We continue to believe that our approach to investing – characterized by highly-concentrated investments, owned with patience, enabled by the right structure – will be an important factor driving meaningful long-term returns. And in a higher dispersion world that we may have recently entered, the importance of this formula will only increase.

Sincerely,

Andrew Macken & Chris Demasi

Podcast: Join the Montaka Global Investments team on Spotify as they chat about the market dynamics that shape their investing decisions in Spotlight Series Podcast. Follow along as we share real-time examples and investing tips that govern our stockpicks. Click below to listen. Alternatively, click on this link: https://podcasters.spotify.com/pod/show/montaka

To request a copy of our latest paper which explores the empirical research around the 3 pillars of active management outperformance, please share your details with us:

Note: Montaka is invested in Spotify, Meta, Microsoft, Salesforce & ServiceNow.