|

Getting your Trinity Audio player ready...

|

In Parts I and II of this four part blog, we went back to first principles of savings, investment and trade. We then gave consideration to the trajectories of savings and investment of the US to see if we could make any sensible assessments of the likely trajectory of its current account and the US dollar. We concluded that the significant fiscal stimulus recently effected by President Trump will likely increase the US the current account deficit and result in downward pressure on the US dollar in the near-term.

So who will import Trump’s demand?

We have established a reasonable hypothesis that the result of the US fiscal stimulus will be to widen its current account deficit. This is analogous to “exporting demand”. And, by definition, the increase in the US current account deficit must be matched by corresponding increases in current account surplus economies.

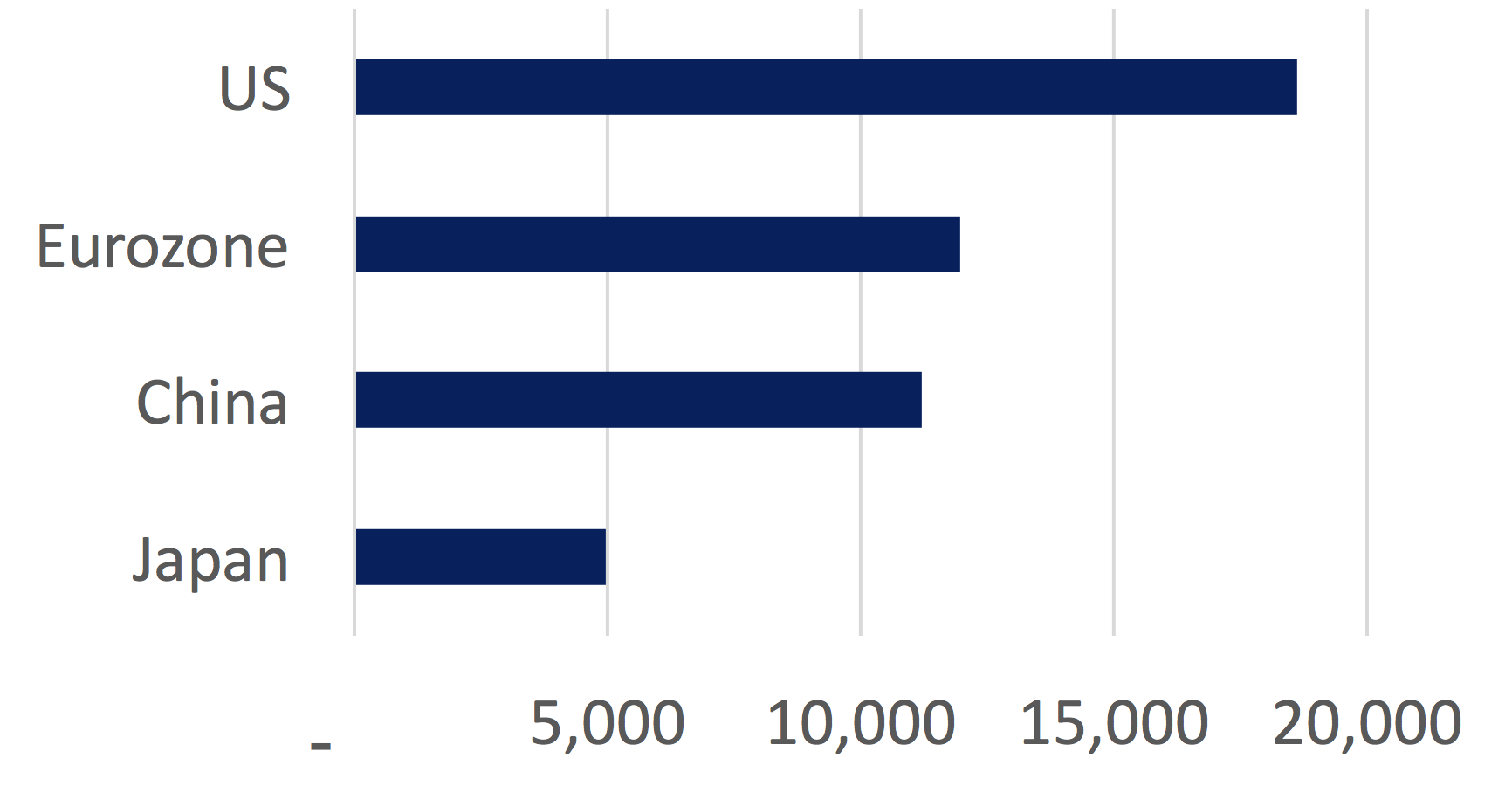

At this point it is worth recalling the approximate relativities in the size of the major economic blocs. Essentially, 1.0% of US GDP equates to approximately:

- 6% of Eurozone GDP;

- 7% of Chinese GDP; and

- 8% of Japanese GDP.

GDP of Major Economic Blocs (2016, US$ Billions)

Source: Bloomberg

From the analysis above, we believe we can rule out China as a major beneficiary of a widening US current account deficit. Essentially, we believe a strengthening Chinese consumer will keep a lid on the Chinese savings rate from rising sharply.

So who will import Trump’s demand?

Most likely the Eurozone and Japan, in our estimation. Both economies have experienced accelerated economic growth in recent years, buoyed by extraordinarily accommodative monetary policies. And we see no reason for additional fiscal stimulus at this point which could reduce their national savings rates.

Indeed, quite the opposite. Should monetary policies normalise in these economies, this would arguably reduce domestic consumption, increase domestic savings and increase current account surpluses. All of the above would result in upward pressure on these currencies.

Eurozone & Japan: Domestic Currency vs Current Account (% of GDP)

Source: Bloomberg

![]() Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.

Andrew Macken is Chief Investment Officer with Montaka Global Investments. To learn more about Montaka, please call +612 7202 0100.