|

Getting your Trinity Audio player ready...

|

– Andrew Macken & Chris Demasi

The December quarter rounded out an extraordinary year characterized by stock returns that were okay for the many (the median stock in the S&P 500 returned 12.7% in 2023), and extraordinary for the few (one stock in eight from the S&P 500 returned 50% or more). Montaka was fortunate to own many of the extraordinary performers in 2023.

This extreme skew in stock performance – particularly as it favored many megacap stocks – was not anticipated by the conventional wisdom one year ago. It’s yet another example of how conventional wisdom can hinder, rather than assist, investors in their navigational decisions.

We continue to stick to our first-principles-based approach to investment analysis and monitor for high-probability long-term winners within large, attractive transformations. And we try to be ready to act at a moment’s notice should stock prices move to levels that reflect significant undervaluation.

This happened in October when global luxury powerhouse, LVMH, experienced a stock price decline of nearly 30% from its peak several months prior. We have studied this business in detail over the years and were patiently waiting for a stock price attractive enough for investment. We took the opportunity to sell The Carlyle Group to fund this new investment. We have not been happy with Carlyle’s management team and governance, and we believe Montaka’s large continuing investments in Blackstone and KKR provide adequate exposure to the benefits we foresee in the alternative asset management space.

Beyond this, Montaka’s portfolio did not change much during the quarter. Annualized portfolio turnover remains very low by industry standards, at just 26%.

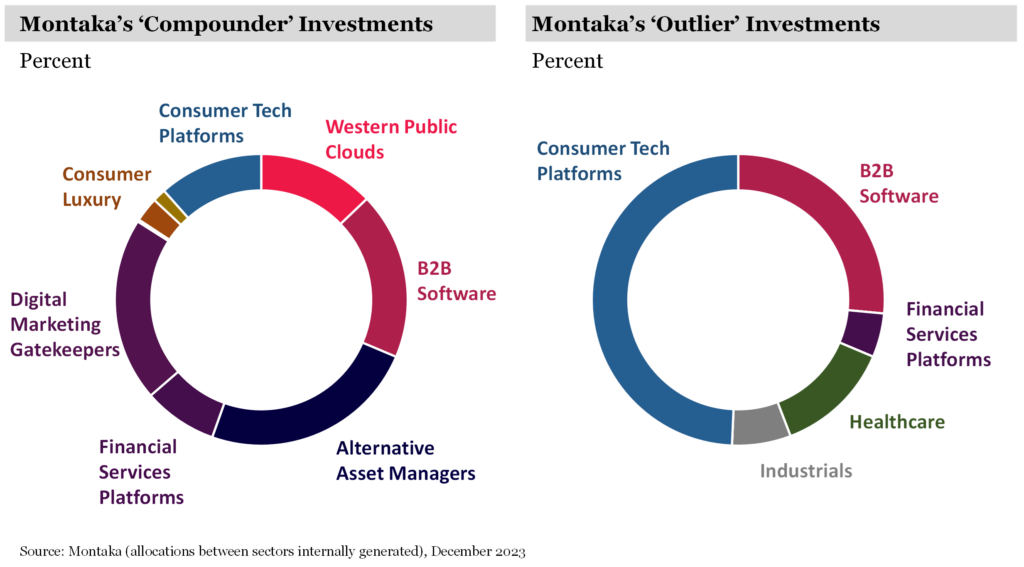

We continue to invest overwhelmingly towards ‘compounder’ businesses, which account for approximately 85% of Montaka’s portfolio; and retain a modest allocation of around 12% to ‘outlier’ opportunities.

We show sector exposures of Montaka’s compounders and outliers below.

This quarter, in place of a stock case study, we walk you through Montaka’s portfolio and examine five key areas of investment opportunity. Most of Montaka’s ‘compounder’ investments belong to at least one of these key areas.

In each case, as you will see, it is insufficient to simply identify areas of growth or business quality. Of course, it is underappreciated growth or profitability that creates the conditions for investment opportunity today.

A common thread running through each of these investments is ‘time horizon arbitrage’. That is, while most investors in the market are myopically focused on the next quarter’s earnings ‘beat’ or ‘miss’, Montaka instead focused on more substantial variations between likely earnings power, relative to expectations, several years into the future.

Winners in alternative assets (‘alts’)

One of the less obvious ‘fly wheels’ Montaka identified several years ago was in the business models of the world’s leading alternative asset managers – particularly Blackstone and KKR. We observed that, in the asset management industry, growth disproportionately favors the largest, biggest, most trusted brand names, with the longest track records. This greater scale drives advantages in talent attraction/retention, access to deal flow, geographic and product diversification, and client attraction/retention – which further drives scale, and so the flywheel continues to gather steam.

The alternative asset management space is undergoing a large structural transformation that we believe will result in supernormal asset growth over the coming decade – and will disproportionately favor the leading managers. Th industry, at approximately US$10 trillion aggregate AUM today, has significant room to grow in the context of global stocks and bonds of more than US$200 trillion, and real estate an additional US$100 trillion. Growth will continue to be driven by (i) Insurance partnerships – which represent a US$30 trillion pool of assets; (ii) Retail / private wealth channels – which represent more than US$80 trillion in assets; and (iii) Asian allocations to alts – which are currently running at a penetration that is one-quarter that of North America.

While this structural transformation of the alts space remains in an early innings, it is coming – and we think it is underappreciated by the market. Over time, we believe it will continue to benefit the shareholders of Blackstone and KKR immensely, of which Montaka is one, on your behalf.

Winners in AI

It will come as little surprise to regular readers that Montaka’s portfolio is meaningfully exposed to those select businesses we assess as high-probability long-term winners from the AI revolution – which remains in its infancy.

We see AI winners across three basic dimensions:

- Those that can ‘distribute’ the benefits of AI to customers. Winners along this dimension will likely be dominated by those businesses with existing large privileged datasets, and large embedded customer bases. These include the likes of Microsoft, ServiceNow, Salesforce, and Spotify.

- Those that can employ AI successfully in their own operations to increase productivity. Early winners along this dimension include Meta and Alphabet – though longer-term winners will span lots of non-tech industries as well.

- Those that sell the compute, and related services, required to run the AI-infused software applications. Along this dimension, the three hyperscalers – Amazon, Microsoft and Alphabet – are the clear winners in the western world. (Alibaba and Tencent continue to appear to be the highest probability winners in the second largest economy in the world, China).

After some strong stock price performances in 2023, the temptation is there for some investors to perhaps wonder if the ‘AI thesis’ has already largely played out. We strongly caution against such a view. Indeed, our research shows that, for most large enterprise clients, early experimentation is underway, however, large-scale roll-outs of AI-infused applications have not yet even begun.

Mission-critical financial services platforms

There are several financial services platforms out there today that are so mission-critical, one does not need to lose sleep over whether or not the businesses will exist over the longer term. Identifying these businesses is relatively straight forward. It is far more challenging to identify a subset of these businesses that are mispriced by the market today and materially undervalued. We believe we have currently identified two.

S&P Global owns some of the world’s largest and most valuable financial datasets and has built several important businesses on top of these advantages. One of its most valuable is its Ratings business which provides credit ratings for the world’s fixed income securities. Of course, this business won big from the significant bond issuance that happened when interest rates were very low during the pandemic – and demand was pulled forward. But when rates started to rise, S&P Global experienced an ‘air pocket’ and demand temporarily evaporated.

But while Ratings earnings are currently depressed, the market is not adequately reflecting the large earnings uptick that will materialize over the coming years. Substantially all of the bonds issued over the last three years need to be refinanced. The demand for S&P’s ratings is simply pent-up. It is coming. Indeed, between now and 2026, S&P Global expects that US$8 trillion in refinancings that will need ratings.

Visa is the world’s largest global payments network and probably needs little introduction. What is underappreciated about Visa is the long-term compounding effect of its relatively newer, smaller, but higher-growth businesses in Visa Direct and B2B/Commercial payments – and the various services that will be attached to these over time.

Today, most of the market is myopically focused on Visa’s large core consumer payments business, which is slowing now after a booming period fueled by fiscal stimuli and high inflation. But the longer-term contribution from Visa’s newer businesses will likely be more than the market currently expects due to the compounding effect of their relatively higher growth rates and very large addressable markets.

Digital marketing gatekeepers

The world’s digital marketing gatekeepers – think Meta, Alphabet, Amazon and Tencent in China – continue to grow in importance for the revenue-generation of businesses, large and small, and from substantially all industries. As businesses become more sophisticated in harnessing their customer data, and the digital marketing platforms grow in sophistication with data-based targeting and measurement, buyers and sellers are increasingly connected for transactions that would otherwise have not been made. As a result, the willingness to pay for these services by advertisers continues to grow structurally.

This dynamic is best illustrated with a simple example from 2023. L’Oreal, the world’s largest cosmetics company, has consistently grown its revenues at around 15% per annum of late, in a global cosmetics market that typically grows only around 6 or 7% per annum. The reason for this extraordinary outperformance is increasingly larger allocations to sophisticated digital marketing spend.

L’Oreal spends approximately €14 billion per annum on advertising and promotions (A&P) – of which, 75% is allocated to digital media. In 2024, it will grow this spend by another 16% over and above 2023 levels. “We are developing our own AI-powered A&P allocation tool,” L’Oreal’s CEO, Nicolas Hieronimus, said last year, “which gives spectacular results in terms of increasing ROI both short-term and long-term.”

Through this lens, the world’s digital marketing gatekeepers hold the key to unlocking new sales for businesses across a wide range of industries that otherwise would not be made. This makes them, in effect, quasi-shareholders in nearly every other business on planet earth. And we believe this continues to be underappreciated by the market.

A consumer luxury winner

LVMH owns several of the world’s most prestigious and well-nurtured luxury brands, including Christian Dior and the 170 year-old Louis Vuitton.

In a world in which the wealthy continue to grow wealthier, LVMH’s best customers have an extraordinary ability to pay almost any price for the world’s most luxurious goods. Price increases – even substantial ones – are not questioned, or even noticed, by these customers. And indeed, higher prices only serve to increase the cachet and exclusivity of these brands. As a result, long-term revenue growth will likely continue to be driven by price increases to an unusually large degree.

Such a strong contribution to growth from pricing has important profit margin implications for LVMH. It means that long-term profit margins will probably end up at levels far greater than those being expected by the market today. And this is one of the important reasons we believe this extraordinary business is undervalued today.

Macroeconomic musings for 2024 and beyond

We provide a brief summary of our macroeconomic assessments below. Please note, however, that most macroeconomic eventualities, while relevant for corporate earnings in the aggregate, will be of less relevance for the select few businesses owned in Montaka’s highly-concentrated portfolio. Just 10 investee companies account for 74% of Montaka’s portfolio exposure. And the growth in earnings power that we see in the coming years for these businesses is overwhelmingly structural, idiosyncratic, and relatively untethered from aggregate GDP growth rates.

Last year started with many believing inflation would be difficult to control and ended with many now believing it’s largely in control. Montaka’s internal analysis of the constituent drivers of inflation suggest that inflation should continue to decelerate, all else equal.

But this is the problem with macroeconomic forecasts – and a core reason why we won’t make them: all else is never equal!

It remains to be seen for how long the Fed keeps interest rates at current relatively high levels – and the impact this will have on many consumers who are already very stretched. If the Fed holds rates high for too long, the Fed itself could push the world’s largest economy into recession.

At the same time, it remains to be seen how China stimulates its very weak economy and the impact this will have on global inflation. Any new wars in 2024 could add to inflationary surprises; while any wars resolved could increase disinflationary surprises.

US politics will also contribute to the calculus. The Republican-controlled House will continue to limit fiscal spending in 2024, which is disinflationary. And with the Republicans likely to take back control of the US Senate in 2025, a win for President Biden in this November’s general election probably means limited fiscal spending in the US for the foreseeable future; while a return of President Trump – which is remarkably possible – would no doubt bring even larger tax cuts, which are typically net inflationary.

New year reflections on the sport of investing

Charlie Munger, rest in peace, said in one his final interviews a few weeks ago: “All investment is intrinsically damn difficult!”

Hear, hear! We continually remind ourselves that investing is not simply the pursuit of forecasting the future and putting money behind these assessments. It’s about taking a different view to that which is priced-in by the market – and, of course, the view needs to be right. This is hard because the market is approximately right most of the time.

And if that weren’t challenging enough, it is generally true that one’s ‘pay day’ from such an investment is the result of others in the marketplace coming around to one’s differentiated view. Of course, the timing of this dynamic is unknowable. It could happen over several weeks, or it could take several years. And it may also be the case that the market’s incorrect view happens to get more wrong before it gets right. (And along every step of the way, how does one know for sure they are right, and the market is wrong?)

To summarize the above, a great investor needs to: (i) develop views that are generally closer to truth than others’, (ii) hold views that others disagree with, (iii) look stupid a lot of the time, and (iv) give up substantially all notions of control over any short-term outcomes. Damn difficult!

The good news is that there are great rewards for those who can understand and work within these dynamics. We assess that one of the greatest advantages an investor can arm themselves with (but most do not) is a genuine long-term perspective.

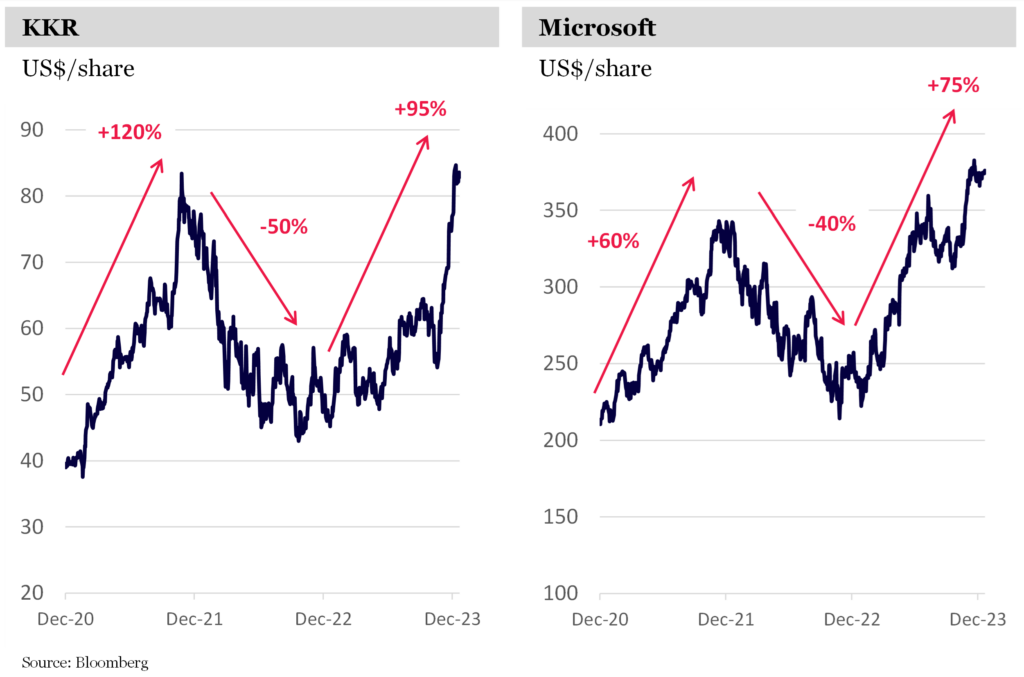

History clearly demonstrates that equities do well over long periods of time – while turning positive or negative with the probability of a coin flip over short periods of time. History also clearly demonstrates that the ‘price of admission’ for owning the world’s highest-returning businesses is frequent and large draw-downs over the holding period.

Just take a look at the experience of KKR and Microsoft – two of the world’s greatest businesses – over the last three years. Great returns, but a frightening ride along the way!

Montaka focuses on the world’s most advantaged businesses that are well-positioned within large structural transformations. And we seek to own the ones for which our assessment of future earnings power is materially higher than that which is priced-in by today’s stock prices.

And by freeing ourselves from the worry of uncontrollable stock price journeys over the short term, we can hang on to these great investment opportunities – with great long-term reward.

Of course, this is only possible because of the extraordinary patience of Montaka’s investors, team members, and stakeholders. And for this, we are extremely grateful.

Podcast: Join the Montaka Global Investments team on Spotify as they chat about the market dynamics that shape their investing decisions in Spotlight Series Podcast. Follow along as we share real-time examples and investing tips that govern our stockpicks. Click below to listen. Alternatively, click on this link: https://podcasters.spotify.com/pod/show/montaka

To request a copy of our latest paper which explores the empirical research around the 3 pillars of active management outperformance, please share your details with us:

Note: Montaka is invested in Spotify, Meta, Microsoft, Salesforce & ServiceNow.